Can Dollar Tree Earnings keep this rally alive, or did the market just price in the easy upside all at once?

Why are Dollar Tree Earnings moving shares?

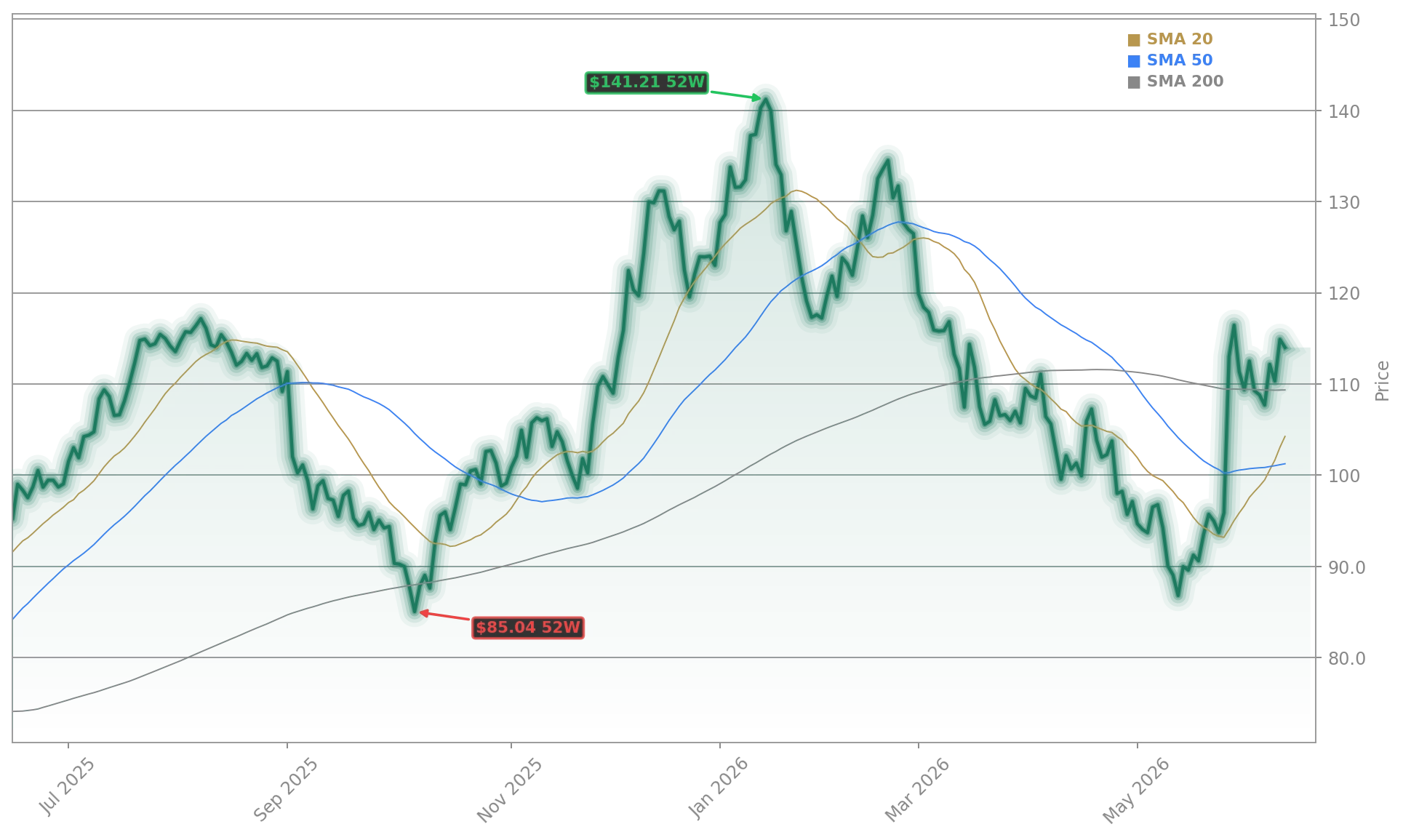

Dollar Tree, Inc. posted first-quarter adjusted earnings per share of $1.74, above the $1.53 consensus, while revenue reached about $4.99 billion, ahead of expectations near $4.96 billion. The company also raised its fiscal 2026 adjusted EPS outlook to $6.70 to $7.10, up by $0.20 from its prior range. That combination of an earnings beat and a higher forecast helps explain why Dollar Tree Earnings triggered one of the strongest moves in the discount retail group on Thursday.

The market reaction matters because DLTR had come into the report with muted expectations after earlier weakness in the stock. Investors were looking for proof that value retail can still hold traffic and profitability even as lower-income consumers remain pressured by inflation and fuel costs. Instead, the quarter showed a business that is gaining from shoppers trading down, while also managing freight, shrink, and merchandising more effectively.

How is Dollar Tree handling consumer pressure?

Reuters reported that strong demand for affordable essentials helped support the improved outlook, even with tariff-related cost pressures still in the background. Management’s multi-price strategy, store improvements, and tighter execution appear to be supporting both basket size and margins. Several reports noted that store visits softened, but average spending per trip increased, suggesting customers are consolidating purchases and staying price conscious.

That dynamic is important for investors comparing discount chains. Dollar Tree’s response to consumer strain looks more disciplined than many feared, particularly after the company’s separation from Family Dollar sharpened its operating focus. Stock Titan highlighted 7.2% net sales growth, a 3.5% comparable-store sales gain, and 113 new store openings in the quarter. Reuters also pointed to better margins despite higher import costs, reinforcing the idea that execution, not just pricing, drove the upside.

Elsewhere in retail, investors are watching peers such as DoorDash, Best Buy, and Dollar General for signs of whether budget pressure is broadening across categories. Dollar Tree’s new nationwide partnership with DoorDash adds an extra convenience angle, giving customers on-demand access to more than 9,000 stores.

What are analysts saying about Dollar Tree?

Analyst sentiment remains mixed but constructive. TradingView noted that Barclays kept an Overweight rating while trimming its price target to $131 from $149, signaling continued confidence in the long-term setup even after moderating near-term valuation assumptions. A day earlier, Moomoo reported that Deutsche Bank downgraded DLTR to Hold from Buy, though it still raised its price target to $99 from $92.

Those calls show the debate around Dollar Tree Earnings is shifting from whether the company can stabilize to how much upside is already reflected after the stock’s sharp rebound. Thursday’s move pushed DLTR well above Deutsche Bank’s updated target and closer to Barclays’ revised view, which may lead some investors to look for confirmation in second-quarter guidance and ongoing traffic trends.

For now, the better takeaway is that earnings quality improved. The beat was not driven by a single line item, and the guidance increase suggests management sees enough demand durability to offset external pressures. That is typically the kind of setup that gets growth and value investors interested at the same time.

What should investors watch next at Dollar Tree?

The next test is whether Dollar Tree can maintain comparable sales growth while protecting margins if consumer budgets tighten further during the summer. Investors will also be watching how the DoorDash rollout influences basket mix, whether new stores ramp efficiently, and how tariff exposure evolves. In a market also tracking leaders like NVIDIA and Apple, DLTR stands out as a consumer name tied less to AI enthusiasm and more to everyday spending behavior.

Related Coverage: Earlier coverage on StockNewsRoom explored whether a prior beat and the company’s expanding multi-price strategy could justify a sharp stock reaction despite cautious guidance. That analysis remains useful for investors comparing how sentiment around value retail has evolved into the latest quarter. Read more in Dollar Tree Earnings +7.1% Surge After Record Quarterly Beat.

Dollar Tree Earnings delivered exactly what bullish investors needed: a clear beat, a raised outlook, and evidence that value demand remains healthy. After DLTR’s 17.55% intraday jump, the focus now shifts to whether margin gains and higher baskets can continue through the rest of fiscal 2026. If management keeps executing, Dollar Tree Earnings could remain a key catalyst for the stock.