Is MicroStrategy Debt Reduction a smart balance-sheet reset, or an early warning that the Bitcoin buying machine is slowing down?

Why does MicroStrategy Debt Reduction matter now?

MicroStrategy Incorporated, now operating as Strategy, completed a repurchase of its 0% convertible senior notes due 2029, retiring $1.5 billion of debt for about $1.38 billion in cash. The discount matters: the company cut liabilities while avoiding a fresh equity raise in a weak tape. Just as important, it did not buy Bitcoin last week, a notable break from the pattern many investors have come to expect from executive chairman Michael Saylor and CEO Phong Le.

That decision has immediate market relevance because Strategy is often treated as a leveraged Bitcoin proxy rather than a software business. When the company pauses purchases, traders tend to question whether Bitcoin demand support is fading. Bernstein previously described the firm as a kind of Bitcoin buyer of last resort, so a pivot toward debt management naturally changes the debate around valuation, liquidity, and upside torque.

Can Strategy protect liquidity and valuation?

The headline benefit is clear. Total convertible debt outstanding fell from roughly $8.2 billion to $6.7 billion, and management framed the transaction as proactive capital management. Strategy still holds a massive Bitcoin treasury, with reported figures across recent disclosures ranging above 700,000 BTC and newer market chatter placing holdings even higher. Either way, it remains the world’s largest corporate Bitcoin holder by a wide margin.

The tradeoff is cash. The company’s dollar reserve reportedly dropped from $2.25 billion to $871 million. That leaves less flexibility against roughly $1.2 billion of annual dividend and debt-service obligations tied to STRC and other preferred instruments. For equity holders, MicroStrategy Debt Reduction helps near-term leverage optics, but it also increases pressure to raise new capital if Bitcoin stalls or financing markets tighten.

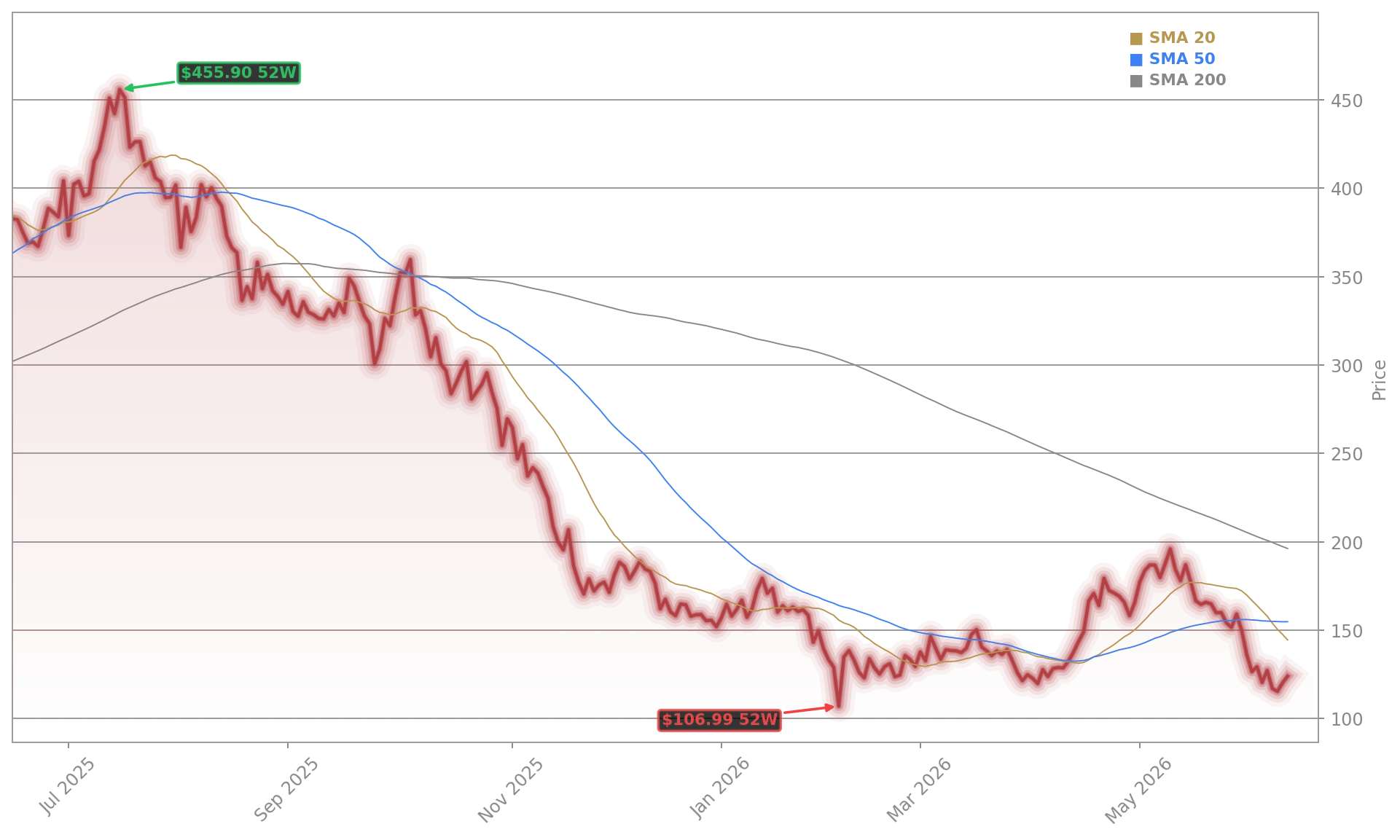

That tension helps explain the stock reaction. MSTR is well below its 52-week high of $457.22 and remains above its 52-week low of $104.17, so this is neither a breakout nor a capitulation signal. It is a reset in expectations.

How are Wall Street and traders reading Strategy?

Analyst sentiment still leans constructive. Market tallies show 14 Buy or Strong Buy ratings against 1 Hold, reflecting confidence that Bitcoin stabilization could re-expand the premium investors assign to Strategy’s treasury model. TradingKey recently highlighted a median analyst target near $347.50, while 24/7 Wall St. published a much more aggressive upside scenario above $425. Those targets are highly path-dependent on Bitcoin, which means Strategy continues to trade more like a structured crypto vehicle than a conventional software stock.

Institutional positioning also remains active. TradingView highlighted combined additions by major holders including BlackRock and Vanguard. At the same time, hedge fund manager Paul Tudor Jones exited his direct equity stake while keeping puts and calls, effectively turning Strategy into a volatility trade. That is a useful signal for investors comparing MSTR with high-beta market favorites like Tesla or NVIDIA: volatility itself is part of the thesis.

Elsewhere, insider selling filings tied to Jarrod M. Patten added another layer of scrutiny, even if the sales were modest relative to Strategy’s market value.

What should investors watch beyond Bitcoin?

The underfollowed part of the story is the operating business. Strategy reported Q4 2025 revenue of $123 million, with subscription growth of 62.1% on its STRC platform, even as EPS was hit by a $17.44 billion unrealized Bitcoin loss. That split matters because a stronger software and capital-markets engine could eventually reduce dependence on constant treasury expansion.

Related Coverage: Investors following balance-sheet risk should also read our look at MicroStrategy Bitcoin Sales and the recent -5.1% plunge, which explored how quickly sentiment can shift when the market questions the company’s Bitcoin playbook. The same report is also relevant from a sector angle because it shows how Strategy’s moves can ripple across crypto-linked equities and influence trading in adjacent risk assets such as Apple suppliers and other momentum names.

We remain focused on expanding STRC to generate amplification and drive growth in Bitcoin Per Share for MSTR common stock investors.— Phong Le

MicroStrategy Debt Reduction gives Strategy breathing room and shows management is willing to defend the balance sheet, not just chase more Bitcoin. For investors, the next catalyst is whether the company can rebuild liquidity without diluting shareholders too aggressively. If Bitcoin stays firm and financing windows stay open, MicroStrategy Debt Reduction could mark a smarter, more durable phase in the bull case for MSTR.