If Dell AI Servers are printing record revenue, why is the stock suddenly trading like the market has stopped believing?

Why Are Dell AI Servers Driving Revenue — Not Stock Gains?

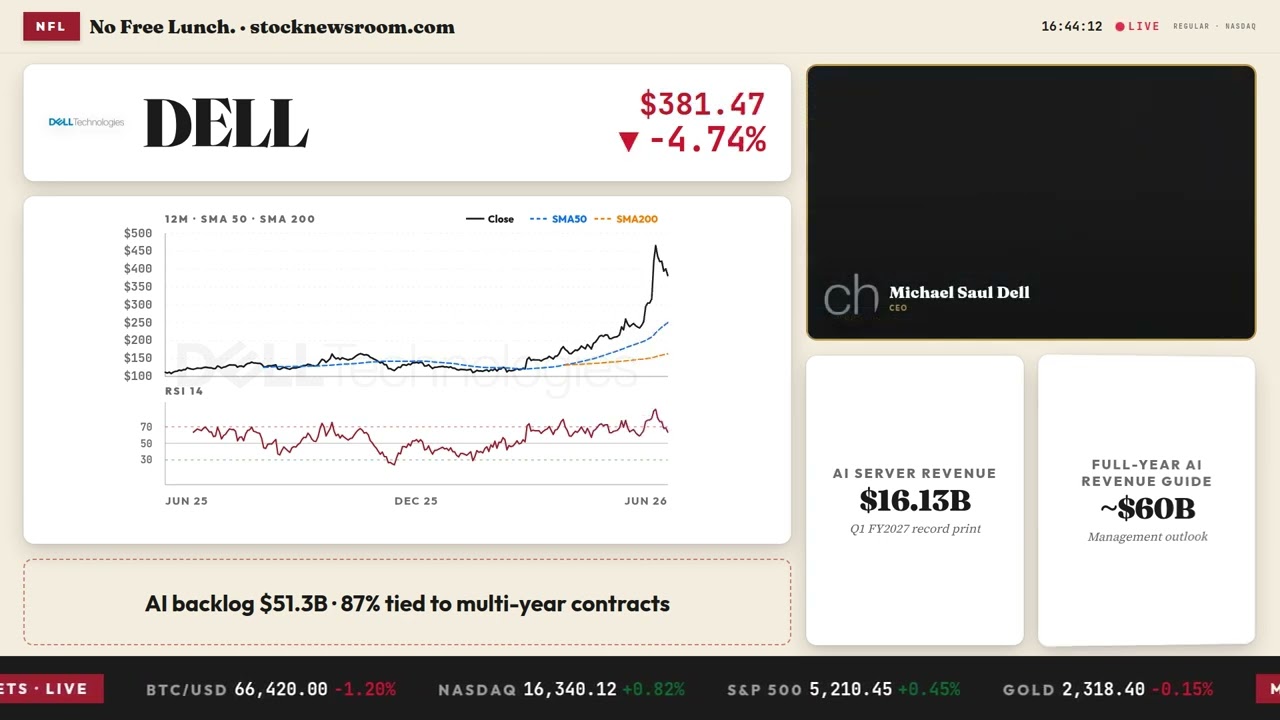

Dell Technologies Inc. reported $16.13 billion in AI-optimized server revenue for Q1 FY2027 — a staggering 757% increase year over year — yet its shares dropped 4.74% to $381.78 after hours. The disconnect underscores a broader market shift: while fundamentals remain robust, positioning and flows now dominate price action. Dell Technologies Inc. has become a poster child for the ‘Parabolic Seven’ — high-momentum AI infrastructure names now facing mechanical deleveraging. Its 31.4x trailing P/E remains more moderate than peers like Super Micro Computer, yet volatility is king in today’s environment. Traders are prioritizing risk reduction over earnings beats — especially ahead of Wednesday’s CPI report and escalating tensions in the Strait of Hormuz.

Is This a Rotation — or a Reckoning?

Yes — and it’s sector-wide. Hewlett Packard Enterprise (HPE), Cisco, and other AI infrastructure players are all under pressure, confirming this isn’t Dell-specific. The coordinated 9% intraday slide in Dell Technologies Inc. and 11% drop in Super Micro Computer signals a macro-driven rotation out of high-beta tech. Analysts at RBC Capital Markets note that ‘de-risking in AI hardware is structural, not cyclical — it reflects portfolio rebalancing amid rising rate uncertainty.’ Meanwhile, Citigroup maintains its ‘Buy’ rating on Dell Technologies Inc., citing ‘unmatched execution in AI server delivery and a $51.3 billion backlog that remains underappreciated.’ Still, the firm lowered its near-term price target from $492 to $483.83, acknowledging short-term headwinds.

What Do the Technicals Say?

Despite the pullback, Dell Technologies Inc. remains in a powerful uptrend: up 226% over 12 months and trading 17% above its 20-day simple moving average ($318.59). Its MACD remains above the signal line, signaling improving momentum — not capitulation. Yet the stock is stretched: trading 129% above its 200-day SMA ($162.86) makes it highly sensitive to volatility spikes. Support at $318.59 is the first line in the sand; a break below could trigger deeper mean reversion. Resistance looms at $469.47 — the June 52-week high. Benzinga Edge scores reinforce the duality: Momentum (98.82), Value (20.57), Growth (52.5). For investors, this means the trend remains bullish — but risk management is non-negotiable.

How Does Dell Compare to AI Infrastructure Peers?

Dell Technologies Inc. stands apart from Super Micro Computer on valuation and execution discipline. While SMCI trades at 13x forward earnings, Dell Technologies Inc. trades at 21x — a premium justified by its scale, diversified channel, and enterprise trust. Unlike SMCI, Dell Technologies Inc. doesn’t rely on a single OEM model; its AI servers are co-engineered with NVIDIA and deployed across hyperscalers like Meta and cloud providers. That said, competition is intensifying: Cisco’s AI server push, HPE’s Apollo line, and even Apple’s in-house silicon ambitions are pressuring margins. Morgan Stanley recently upgraded Hewlett Packard Enterprise to ‘Overweight,’ citing ‘stronger AI server visibility,’ a subtle signal that Dell’s dominance isn’t guaranteed. Still, Goldman Sachs reaffirmed its $485 price target, stating, ‘Dell AI Servers are the most scalable, enterprise-ready platform in the market.’

What’s Next for Dell Technologies Inc.?

With full-year AI server revenue guidance now at ~$60 billion, Dell Technologies Inc. is on pace to capture over 25% of the global AI infrastructure market in FY2027. The next catalyst is the June 17 AI Infrastructure Summit, where Dell is expected to announce new liquid-cooled server platforms targeting LLM training workloads. Analysts at JPMorgan warn that ‘any delay in new platform ramp could trigger follow-through selling,’ but most expect Dell to maintain its leadership in AI server volume — not just revenue. The $51.3 billion AI backlog remains a powerful buffer, and with 87% of that tied to multi-year contracts, visibility is unusually high. For long-term investors, this dip may be a strategic entry point — especially if the S&P 500 stabilizes post-CPI.

Related Coverage: Dell’s $51.3 billion AI backlog isn’t just a headline number — it’s a strategic moat backed by multi-year commitments from global cloud leaders. To understand whether Wall Street has already priced in flawless execution — or if there’s still upside — read Dell AI Forecast: $51B Backlog, Raised Outlook, Warning.

Dell AI Servers are the most scalable, enterprise-ready platform in the market.— Goldman Sachs

Dell AI Servers remain the core growth engine for Dell Technologies Inc. — delivering record revenue, raising guidance, and reinforcing its role as a critical enabler of the AI infrastructure buildout. For investors, the selloff reflects short-term positioning pressure, not deteriorating fundamentals. The next quarterly earnings will test whether momentum rebounds alongside broader Nasdaq stability. For disciplined investors, Dell AI Servers represent both a near-term volatility hedge and a long-term compounder in the AI era.