Is Berkshire’s multibillion-dollar Delta move a one-off trade, or the clearest sign yet that Buffett’s airline skepticism is over?

What Does Delta Air Lines Berkshire Stake Say About Buffett’s Legacy?

Greg Abel’s $2.65 billion Delta Air Lines Berkshire Stake — comprising nearly 40 million shares disclosed in Berkshire’s Q1 2026 13F filing — isn’t just a portfolio tweak. It’s a philosophical reset. While Warren Buffett famously declared airlines lacked durable competitive advantages “since the days of the Wright Brothers,” Abel acquired Delta at a trailing P/E of 12x and 25% return on equity — metrics more typical of branded consumer franchises than legacy carriers. The stake landed alongside full exits from Amazon (AMZN), UnitedHealth (UNH), and Domino’s (DPZ), making Delta the clearest signal of Omaha’s new valuation lens: cash-rich, asset-backed, and priced for exhaustion, not collapse.

How Is Delta Outperforming United and Southwest?

Delta Air Lines, Inc. stands apart from peers on three pillars: premium revenue, American Express annuity, and balance sheet discipline. Premium ticket sales surged 14% to $5.36 billion in Q1 2026, while Amex remuneration topped $2.0 billion — up 10% year-over-year and unmatched by United Airlines or Southwest Airlines. United generates higher EPS ($11.18) but pays no dividend; Southwest trades at a stretched 32x trailing P/E on $1.50 EPS amid fee-transformation uncertainty. Delta’s $54.6 billion market cap, 62% high-margin revenue mix, and $4.64 billion full-year 2025 free cash flow make it the only airline with a credible economic moat — a thesis echoed by Citigroup, which upgraded Delta to ‘Buy’ with a $102 price target last week.

Is Delta’s Dividend Hike a Sign of Financial Maturity?

Yes — and it’s accelerating. Delta Air Lines, Inc. announced a 15% quarterly dividend hike to $0.2150 per share, payable July 30, 2026, to shareholders of record on July 9. That follows record 2025 free cash flow and a $3.68 billion reduction in adjusted net debt — down to $14.30 billion. The dividend increase isn’t symbolic: it reflects real capital return capacity, backed by $1.1 billion in loyalty program cash flow alone. RBC Capital Markets recently affirmed its ‘Outperform’ rating, citing “the structural durability of Delta’s branded ecosystem” — a phrase that would make Warren Buffett nod, even if he didn’t sign off on the trade.

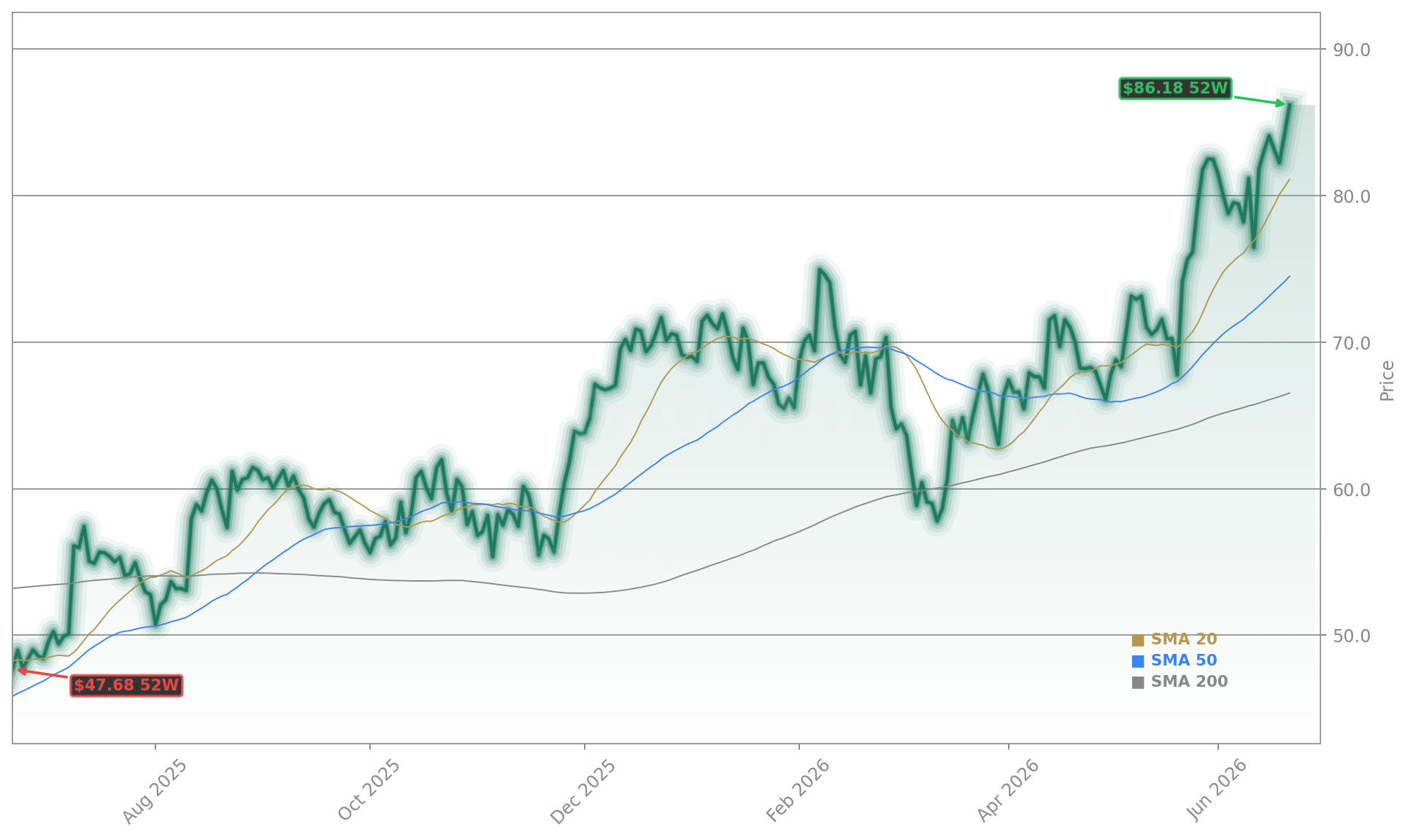

What’s Driving Delta’s 24% YTD Surge?

Beyond the Delta Air Lines Berkshire Stake, three catalysts converged: falling jet fuel prices (down 18% from Q4 2025 highs), robust premium demand (60% of revenue now comes from premium cabins, loyalty, and cargo), and disciplined capacity management. Q1 2026 adjusted EPS soared 44% to $0.64 on $14.20 billion revenue — up 9.4% year-over-year — while management reaffirmed full-year 2026 EPS guidance of $6.50–$7.50. That implies roughly 20% earnings growth, well ahead of the S&P 500’s 11% consensus. Notably, Delta’s 15x forward P/E remains below the NASDAQ’s 27x multiple — offering cyclical exposure with consumer-franchise discipline.

Related Coverage

Delta’s results underscore the power of our brand and the durability of our financial foundation.— Ed Bastian, CEO of Delta Air Lines, Inc.

Delta’s momentum extends beyond Berkshire’s stake: the recent DAL Award +1.7% Surge as $3.3B Deal Volume Expands highlights accelerating infrastructure-linked contract wins, while Caterpillar Data Center Boom as Power Revenue Jumps 48% underscores how industrial players like Caterpillar are capturing AI infrastructure tailwinds — a contrast to Delta’s consumer-anchored, non-AI growth story. For investors seeking exposure to resilient cash flow outside tech, Delta Air Lines Berkshire Stake offers a tangible, valuation-supported alternative.