Has Kevin Warsh just turned the Federal Reserve Rate Path from a cut story into a fresh tightening risk?

What Does Warsh’s Tone Mean for the Federal Reserve Rate Path?

Kevin Warsh didn’t raise rates — but he redefined the Federal Reserve Rate Path. At his inaugural press conference, Warsh declared the Fed had “failed for five years on price stability” and pledged an unambiguous return to its 2% inflation mandate. He declined to submit his own dot plot projection, signaling skepticism toward the tool’s credibility. Nine of 18 FOMC participants now project at least one rate hike in 2026 — up from just four in March — and the median year-end funds rate forecast jumped from 3.4% to 3.8%. The market responded: CME futures now assign a 70% probability to a September hike, with 1.5–2 total hikes priced in by December. That’s a stark reversal from the 2025 cycle, when the Fed cut rates three times.

How Are Treasury Yields and the Dollar Reacting?

The front end of the yield curve tightened sharply: the 2-year Treasury yield spiked to 4.22% post-meeting before settling at 4.17%, while the 10-year yield dipped to 4.49% — reflecting a flattening curve and diminished inflation risk premium. The US Dollar Index surged past 100, pushing EUR/USD below $1.15. Gold slid toward $4,000/oz, prompting Goldman Sachs to slash its 2026 price target from $5,400 to $4,900. Bitcoin fell to $64,000 as spot ETFs bled $111 million in one day — underscoring how tightly crypto now trades with Fed liquidity expectations. Meanwhile, insurance stocks rose on higher yields, and real estate and utilities underperformed as rate-sensitive sectors absorbed the hawkish repricing.

Why Did Warsh Launch Five Task Forces?

Warsh didn’t just tweak messaging — he launched institutional reform. Five new task forces were announced: on communications, balance sheet analysis, data sources, inflation framework, and labor market metrics. The balance sheet group is especially critical: Warsh views quantitative tightening as a core tightening tool, not just a complement to rate hikes. As he noted, “If rates and the balance sheet aren’t in tandem, you’re pressing the gas and brake simultaneously.” The communications group signals a deliberate retreat from Powell-era forward guidance — echoing Alan Greenspan’s “mystery and ambiguity” doctrine. This isn’t delay; it’s strategic recalibration. As Citigroup analysts observed, “Warsh isn’t buying time — he’s buying rigor. His Federal Reserve Rate Path depends on better data, not better forecasts.”

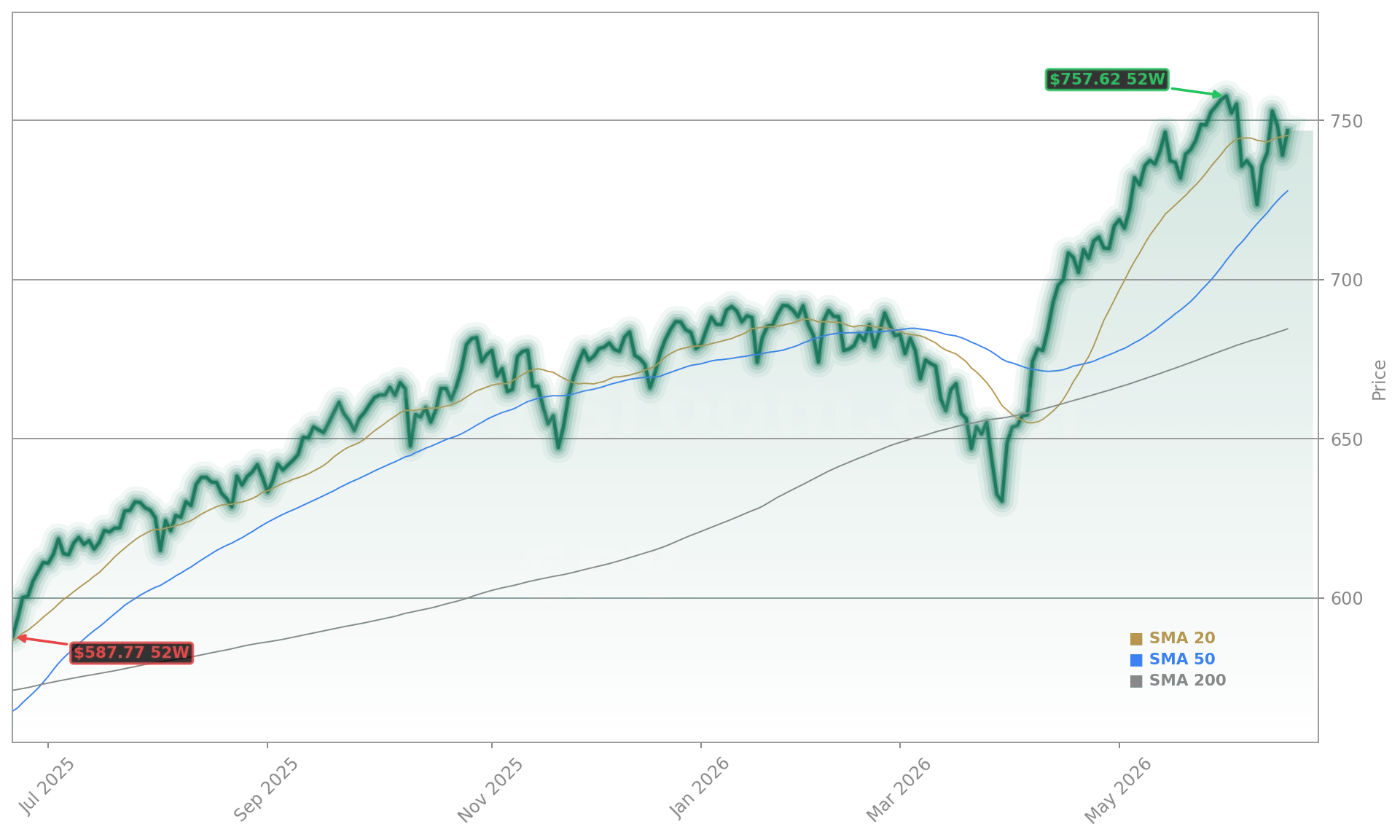

What’s the Outlook for S&P 500 and Mega-Cap Tech?

Markets absorbed the shock: the S&P 500 closed up 1.1% at 7,562, and the NASDAQ jumped 2.5% to 30,406 — led by NVIDIA, Tesla, and Apple. That resilience reflects a key reality: strong earnings (25–26% YoY growth in Q1 2026) and robust capital investment are offsetting rate concerns. Yet breadth is widening — the Russell 2000 hit a new high, and financials outperformed. Still, the Federal Reserve Rate Path poses a headwind for growth stocks. RBC Capital Markets downgraded the semiconductor sector to “Underperform,” citing “tighter financial conditions and delayed AI capex.” Morgan Stanley maintains its “Overweight” on financials, citing “higher-for-longer net interest margins.” With core CPI holding at 2.9% and PPI pressures mounting, the Fed’s path remains data-dependent — but the bar for cuts has risen meaningfully.

What’s Next for Investors?

The next FOMC meeting is in late July — and Warsh’s approach will be tested. If June’s CPI print holds above 3.5%, a September hike becomes near-certain. The Fed’s new inflation framework — which distinguishes supply shocks (e.g., oil) from persistent core pressures — means energy-driven spikes won’t automatically trigger easing. For portfolios, this reinforces the need for disciplined allocation: quality dividend growers, financials, and inflation-resilient consumer staples. As Bloomberg noted in its post-meeting analysis, “Warsh isn’t fighting inflation — he’s rebuilding the Fed’s credibility to fight it. That makes the Federal Reserve Rate Path more credible, not less predictable.”

I’ve said for years that inflation is a choice. You bet it is.— Kevin Warsh

The Federal Reserve Rate Path is now clearly upward in the near term — with credibility as its anchor. For investors, this means positioning for resilience, not reaction. The next quarterly earnings cycle will reveal whether corporate America can sustain margins amid persistent core inflation. For long-term investors, the message is unambiguous: stay invested, but stay selective.