Is Home Depot’s big bet on professional contractors a smart long-term move, or a costly gamble in a frozen housing market?

Why Did Wolfe Research Issue a Home Depot Downgrade?

Wolfe Research analyst Spencer Hanus downgraded The Home Depot, Inc. from Outperform to Peer Perform on June 23, 2026, citing a ‘limbo’ state driven by two converging forces: the persistent mortgage rate lock-in effect and the company’s strategic pivot toward large professional contractors. With the 30-year fixed mortgage rate at 6.47%, homeowners are staying put — suppressing housing turnover and, by extension, large-scale renovation demand. Wolfe noted that while Home Depot’s $18.3 billion acquisition of SRS Distribution and $5.5 billion purchase of GMS strengthen its pro-channel dominance, these moves increase capital intensity and compress near-term margin visibility. The firm offered no revised price target — a notable departure from typical downgrades — signaling uncertainty rather than outright bearishness.

How Does This Compare to Other Analysts?

Wolfe’s move stands in contrast to UBS and Mizuho, both of which maintained bullish ratings despite lowering price targets. UBS cut its HD target to $430 from $450 but kept its Buy rating, emphasizing Home Depot’s unmatched scale and contractor loyalty. Mizuho trimmed its target to $385 from $415 while reiterating an Outperform rating, calling the company ‘the clear leader in a consolidating pro channel.’ Meanwhile, the broader analyst consensus remains a Moderate Buy, with an average target of $371.71 — implying 14% upside from current levels. That gap between Wolfe’s caution and the broader street’s resilience underscores a key tension: long-term competitive strength versus near-term macro vulnerability.

What’s Happening to Home Depot’s Core Metrics?

Q1 2026 delivered $41.8 billion in revenue (+4.8% YoY) and US same-store sales growth of just 0.4% — well below historical norms and flat globally ex-currency. CEO Ted Decker acknowledged on the earnings call that ‘homeowners are taking on smaller projects’ amid elevated inflation and affordability pressure. Gross margin held steady at 34.2%, but SG&A rose 60 basis points as the company absorbed integration costs from recent acquisitions. The dividend remains rock-solid — $2.33 per share quarterly, yielding 2.77%, nearly triple the S&P 500’s yield — and marks 157 consecutive quarters of payouts. Yet investors are pricing in caution: HD trades at a P/E of 24, down from 28 earlier this year, and well below the S&P 500’s 32.

How Are Competitors Like Lowe’s Positioned?

Lowe’s Companies (LOW), HD’s closest rival, posted $23.1 billion in Q1 revenue and is forecasting similar same-store growth — flat to 2% — but with less exposure to large-scale pro integration. The Globe and Mail’s comparative analysis notes that Lowe’s has posted more consistent estimate revisions in recent quarters, while Home Depot’s earnings power is being re-evaluated amid its ambitious pro-channel expansion. Wolfe explicitly stated it ‘prefers Lowe’s’ in the current environment, citing lower execution risk. Still, Home Depot’s $165 billion in annual sales dwarf Lowe’s, and its pro segment now contributes over 55% of total sales — a structural advantage that could pay off when commercial construction rebounds. That said, Wall Street is watching closely: Placer.ai data shows Home Depot’s foot traffic remains more volatile than Target or Costco’s, suggesting weaker organic demand momentum heading into Amazon Prime Day.

What Does the Fed’s ‘Higher for Longer’ Stance Mean?

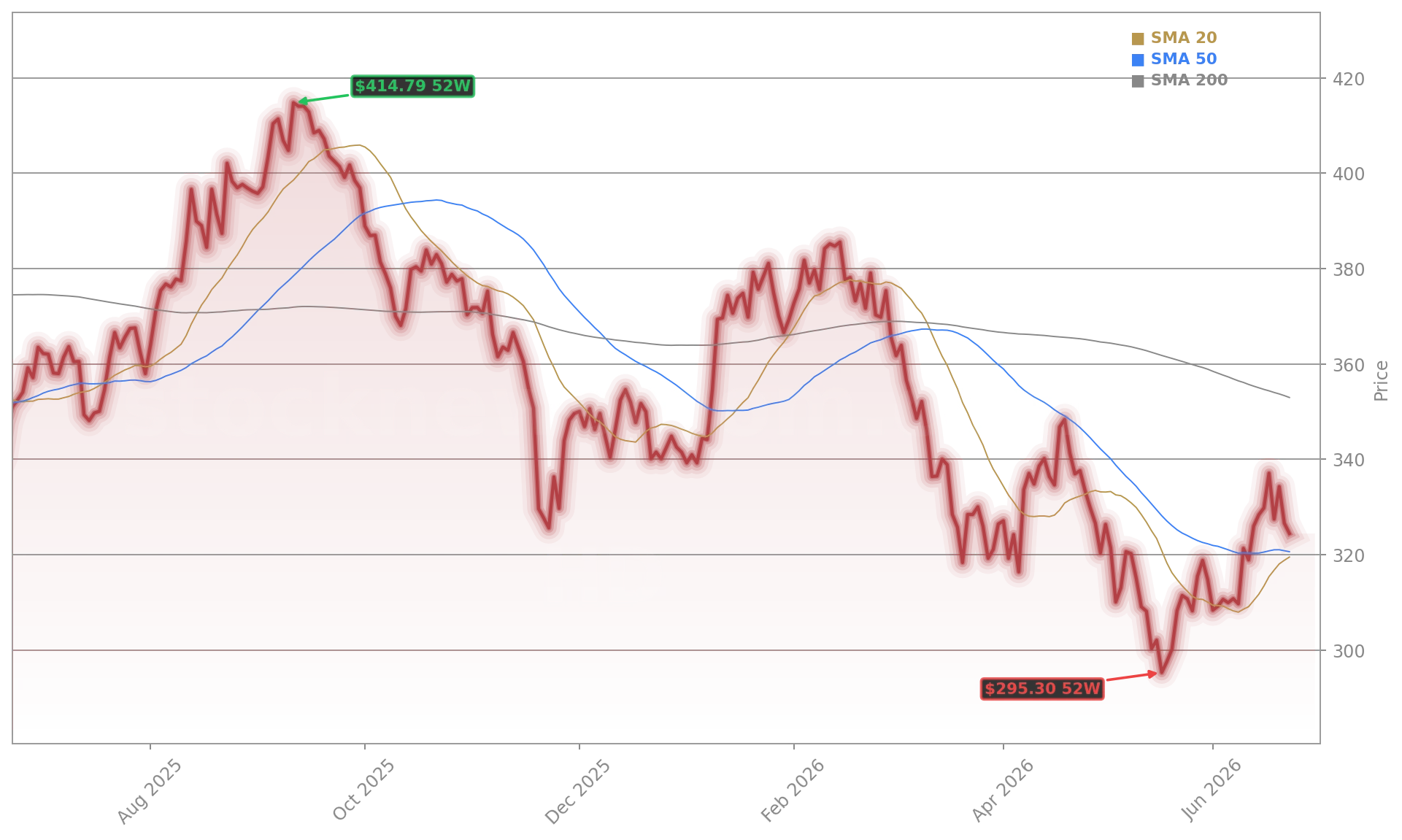

The Federal Reserve’s June 17 decision to hold rates steady — and the revelation that half of FOMC participants expect at least one hike in 2026 — delivered a sharp reminder: housing-sensitive stocks like The Home Depot, Inc. remain at the mercy of monetary policy. HD fell 2.9% through June 18, briefly touching its 52-week low of $289.10. While shares rebounded after the initial selloff, the Home Depot Downgrade crystallizes investor fatigue with the ‘wait-and-see’ narrative. Unlike NVIDIA or Apple, whose earnings are driven by tech cycles and global demand, Home Depot’s performance is tightly coupled to US consumer confidence, wage growth, and housing supply — all still lagging. That’s why institutional activity has been mixed: SG Americas slashed its stake by 51.5%, while Pullen Investment Management and Sentinel Dome Partners added new positions — a split reflecting divergent time horizons.

Related Coverage: Home Depot Earnings Beat on $41.77B Revenue, Outlook Held confirms the company’s operational strength despite soft comps, while GameStop Acquisition: Why the $56B eBay Bid Alarms Bulls offers a cautionary parallel on how aggressive M&A can shift investor focus from execution to balance sheet risk — a dynamic now playing out in Home Depot’s pro-channel strategy.

With the higher rates, housing turnovers remain low. Industry is not expecting a lot of growth in housing turnover this year, and new construction starts and sales are also trending down.— Ted Decker, CEO of The Home Depot, Inc.

The Home Depot Downgrade is not a verdict on the company’s quality — it’s a signal that patience is being tested. For income-focused portfolios, HD remains a core holding: its dividend yield, balance sheet strength, and market leadership are unmatched in the sector. But for Wall Street, the question is no longer whether Home Depot can survive the cycle — it’s whether its pro-channel bets will accelerate earnings before the housing recovery gains traction. With the next quarterly earnings report due in August, investors will watch for signs that smaller projects are scaling up — and whether the Fed’s next move unlocks broader spending. For long-term investors, the current valuation presents a strategic entry point — if they’re ready to wait for the residential recovery to accelerate.