Can Intuit AI Strategy turn deep market skepticism into a comeback, or are institutional buyers stepping in too early?

Why Are Big Investors Buying Intuit Now?

Despite a brutal 2026 for Intuit Inc., major institutions are doubling down. Focus Partners Wealth increased its stake by 10.9% in Q4 2026, holding $109.18 million in shares. The Healthcare of Ontario Pension Plan Trust Fund expanded its position by 18.5%, acquiring 17,016 shares to reach 109,240 shares valued at $72.4 million. State Street Corp bought another 180,069 shares, bringing its total stake to over 13 million shares—worth $8.65 billion. These moves contrast sharply with insider selling and recent price target cuts, suggesting a divergence between short-term sentiment and long-term conviction in Intuit AI Strategy.

What’s Driving the Sell-Off?

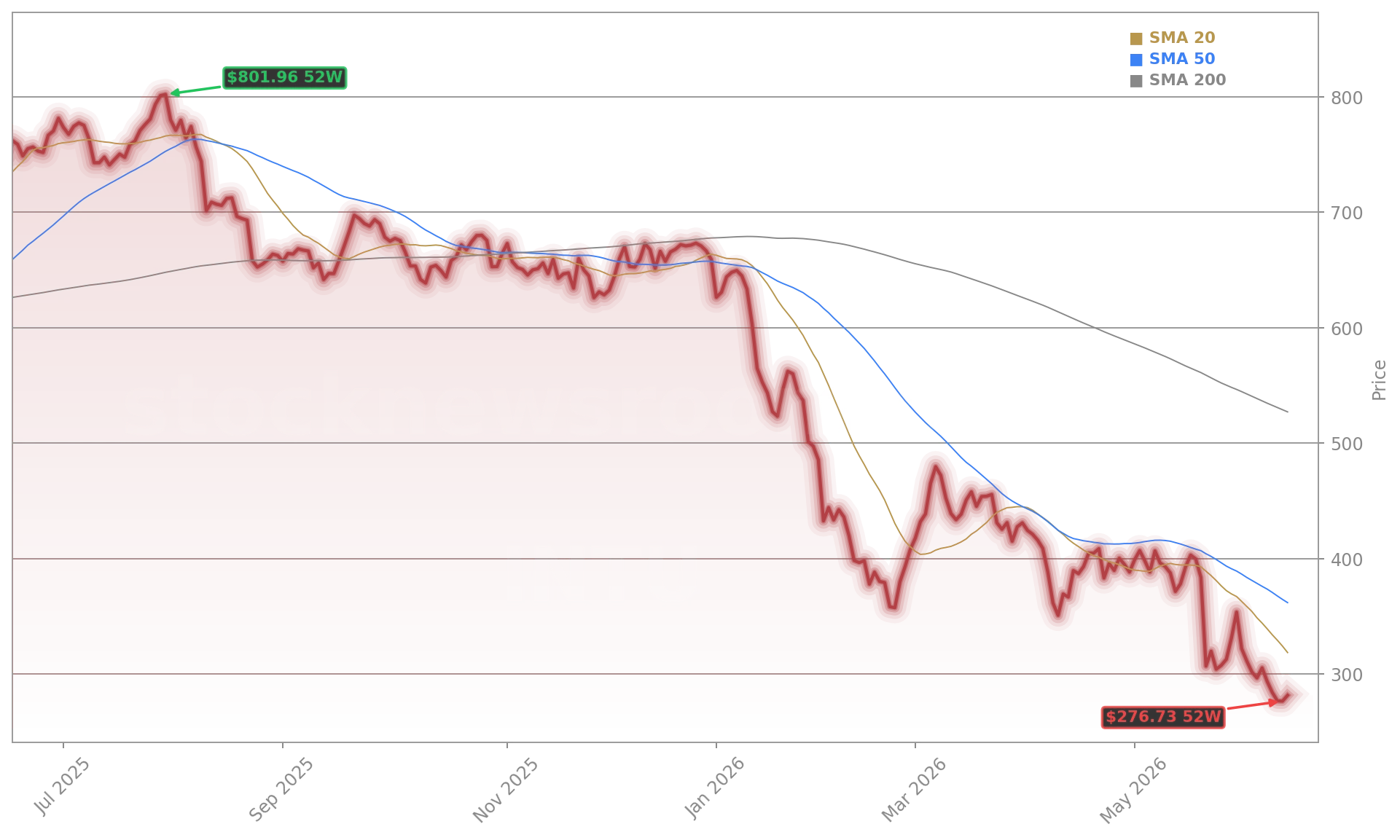

Intuit Inc. has lost more than half its market value since January—down 54.95%—as Wall Street questions its ability to defend its core tax and small-business software franchises. Competitors like Apple-backed tax startups, Chime Tax, and Perplexity Tax are gaining traction with AI-native, low-cost alternatives. TurboTax’s Q3 2026 performance disappointed, prompting Mizuho to lower its price target—though it maintained an Outperform rating. Meanwhile, legal investigations into Intuit’s pricing practices and ongoing scrutiny from the FTC continue to weigh on sentiment. The RSI at 34.4 signals oversold conditions, but without catalysts, technical rebounds remain fragile.

How Does Intuit AI Strategy Compare to Peers?

Intuit AI Strategy stands apart from peers like Adobe and NVIDIA in execution focus—not infrastructure, but embedded financial intelligence. While Adobe leans on generative AI for creative workflows and NVIDIA powers the underlying chips, Intuit is deploying AI directly into tax filing, bookkeeping, and cash-flow forecasting. Its recent partnership with Mother New York—the agency behind its humanized AI branding—signals a deliberate shift from ‘algorithmic accuracy’ to ‘user trust’. That’s critical in a sector where transparency and compliance outweigh raw speed. By contrast, Zscaler and Workday face similar ‘SaaSpocalypse’ fears but lack Intuit’s regulatory moat and recurring revenue stability—85% of Intuit’s revenue is subscription-based.

Can AI Offset the 3,000-Job Cut?

Intuit’s 17% workforce reduction—approximately 3,000 jobs—is explicitly tied to funding its Intuit AI Strategy. The company plans to reinvest savings into AI product development, cloud infrastructure, and customer-facing automation. Analysts at Citigroup and RBC Capital Markets note that while cost discipline is welcome, the real test is monetization: Can AI features in QuickBooks and Mailchimp drive upsells, reduce churn, and lift average revenue per user? With Q3 2026 EPS at $12.80 and revenue at $8.56 billion—both beating consensus—Intuit demonstrated operational resilience. Yet Goldman Sachs’ recent downgrade to Sell and the 8.6% single-day drop it triggered show how thin the margin for error has become.

What Do Analysts Say About the Outlook?

The consensus remains cautiously constructive: 14 of 20 analysts rate Intuit Inc. a ‘Moderate Buy’, with an average price target of $514.58—nearly 80% above current levels. Morgan Stanley reaffirmed its Overweight rating, citing ‘AI-enabled cross-selling potential’ in small business segments. However, Vontobel Holding Ltd. trimmed its stake by 15.2%, selling 115,608 shares—underscoring that even large holders are hedging. With Intuit raising $1.75 billion in senior notes and maintaining a $1.20 quarterly dividend, balance sheet strength is unquestioned. The question isn’t solvency—it’s scalability of the Intuit AI Strategy in a rapidly commoditizing landscape.

Related Coverage: Intuit’s valuation pressure intensified after Goldman Sachs downgraded the stock to Sell—triggering an 8.6% plunge—and investors are now watching for signs of stabilization in the wake of that warning. Meanwhile, broader AI infrastructure demand is gaining traction across defense tech, as seen in Dell’s $1.44 billion Air Force AI contract, which highlights how sovereign AI initiatives may indirectly benefit software firms with government-certified platforms like Intuit’s.

Intuit’s AI isn’t about replacing humans—it’s about making every small business owner feel like they have a CFO, tax attorney, and growth strategist on speed dial.— Brad Smith, CEO of Intuit Inc.

Intuit AI Strategy is no longer just a product roadmap—it’s the linchpin of investor confidence in the company’s next decade. For U.S. portfolios, this is a high-conviction, high-risk bet on AI monetization in regulated verticals. The next quarterly earnings will show whether early AI adoption is translating into measurable revenue lift—not just cost savings. For long-term investors, the institutional buying spree suggests the bottom may be in sight.