Can Intuit still justify its premium valuation after Goldman Sachs turned bearish and the stock suddenly lost nearly 9%?

Why is the Intuit Downgrade moving shares?

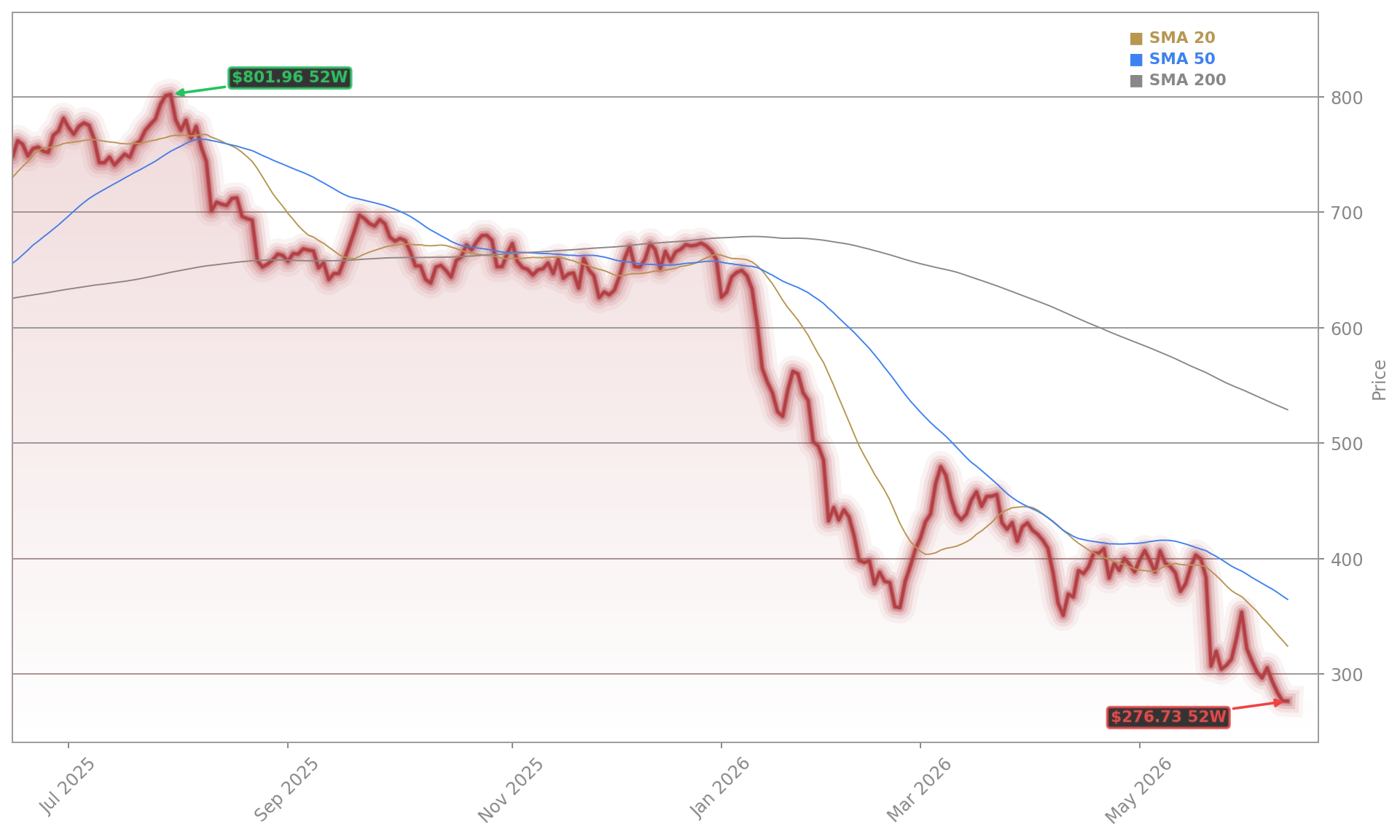

Intuit Inc. (INTU) fell to $323.39, down 8.58% from the prior close of $350.99, making it one of the weakest performers in both the S&P 500 and Nasdaq 100 on Tuesday. The move followed a new bearish call from Goldman Sachs, which downgraded the stock to Sell from Neutral. Analyst Gabriela Borges also lowered the price target to $276, a notable reset from prior expectations and now the most negative recommendation among the broad analyst group following the company.

The bank’s thesis is straightforward: conditions may get worse before they improve. Goldman Sachs sees a tougher environment for consumer tax software, particularly as more price-sensitive do-it-yourself filers compare options and as AI-driven tools begin to reshape user behavior. That backdrop matters because Intuit still derives a critical share of its value from tax preparation and small-business financial software, markets where pricing power and product differentiation are central.

Can Intuit defend its growth story?

The Intuit Downgrade lands only days after the company tried to stabilize sentiment following a bruising post-earnings selloff. Investors had already punished the stock after management acknowledged that TurboTax did not deliver the tax season it had expected and that pricing was a challenge with DIY filers. Several law firms have since announced investigations tied to the earlier 20% one-day plunge, adding another layer of headline risk around the name.

That pressure is colliding with a broader debate over whether software incumbents can defend their franchises as generative AI lowers switching costs. Brown Advisory’s Global Leaders Strategy said it exited its Intuit position in February, pointing to AI substitution concerns even while praising the company’s long-term execution. For investors, that matters because Intuit has long traded as a premium-quality software compounder, more comparable in market perception to platform leaders like Microsoft or Adobe than to slower-growth financial software peers.

Still, the story is not one-sided. In fiscal third quarter 2026, Intuit reported revenue of $8.6 billion, up 10% year over year. Consensus on Wall Street also remains far from uniformly bearish. TradingView data showed the average 12-month analyst target still implies meaningful upside from recent levels, and Rothschild & Co Redburn maintained a Buy rating even while cutting its target to $600 from $700.

How does Intuit compare with rivals?

The key question after this Intuit Downgrade is whether the stock is repricing toward a slower-growth future or simply reacting to a temporary loss of confidence. Intuit remains the dominant U.S. consumer tax software brand and a major player in accounting tools for small and midsize businesses. But dominance does not eliminate competitive risk, especially when rivals can use AI to simplify tax preparation, budgeting, or bookkeeping at lower cost.

That leaves Intuit in a different position from megacap software names such as Apple, NVIDIA, or Meta Platforms, where AI excitement has generally supported multiples rather than compressed them. For Intuit, AI is currently being discussed as both an opportunity and a threat. If the company proves it can use automation to deepen engagement across TurboTax, QuickBooks, and Credit Karma, the bear case may soften. If not, Goldman Sachs may not be the last firm to revisit estimates.

Related Coverage: Investors looking for the backdrop to today’s selloff should also read our earlier report on Intuit earnings, the 20% stock drop, and how AI and layoff fears shook sentiment. That piece explains why a company that beat estimates and raised guidance still lost investor support, and it helps connect the latest analyst action to the broader reset in expectations around the stock.

“Initially, the situation is likely to worsen,”— Gabriela Borges, Goldman Sachs

The Intuit Downgrade underscores how quickly sentiment can deteriorate when premium software valuations collide with pricing pressure, AI concerns, and weaker tax-season execution. For investors, the next test is whether management can restore confidence in TurboTax growth and defend margin resilience across the broader platform. If execution improves, the stock could eventually rebuild credibility, but for now Wall Street is signaling that patience will be required.