Why would a company beat estimates, raise guidance, and still see investors erase nearly 20% in a single session?

Why are Intuit Earnings hitting the stock?

Intuit Inc. delivered fiscal third-quarter revenue of $8.56 billion, up 10.4% from a year earlier, while adjusted earnings reached $12.80 per share, both ahead of consensus. The company also lifted its full-year outlook, projecting revenue growth of 13% to 14%. Under normal conditions, that would have supported the stock. Instead, investors punished the shares as management paired the report with plans to cut about 3,000 jobs, or roughly 17% of the workforce, and warned of softer long-term trends in TurboTax.

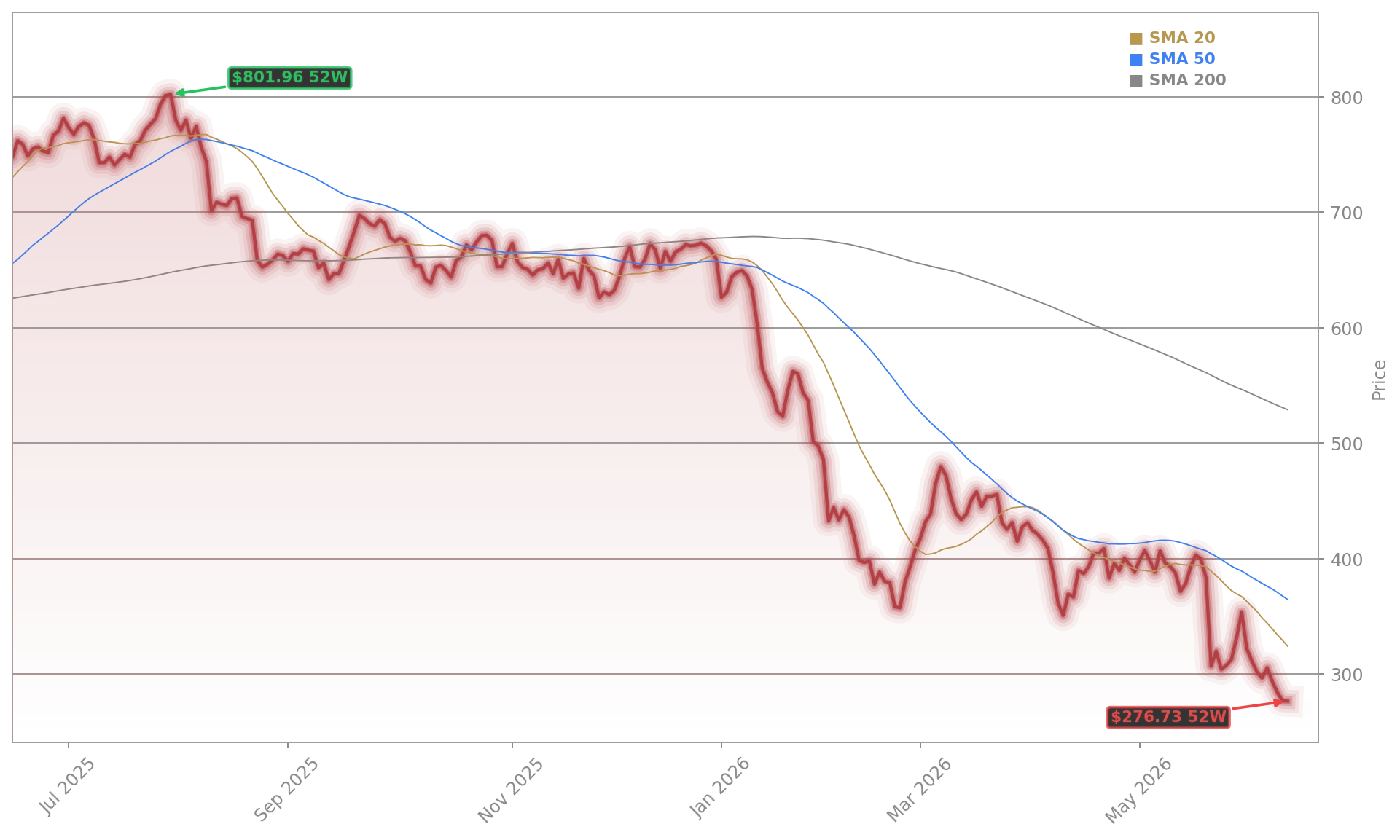

The stock’s drop to $307.33 marks a collapse from the prior close of $332.48 and reflects a far harsher read-through than the headline beat suggested. The key issue was not the quarter itself but what Intuit Earnings implied about future growth quality. Investors appeared worried that margin gains and pricing may be masking weaker unit growth in tax preparation, particularly in lower-income customer segments that are more price sensitive and more willing to experiment with AI tools.

Can Intuit defend TurboTax from AI?

TurboTax remains the center of the debate. Consumer revenue rose 8% to $5.3 billion, and TurboTax revenue increased 7% to $4.4 billion. TurboTax Live was a bright spot, with management expecting full-year revenue growth of 36% to $2.8 billion and customer growth of 38%. But the company also forecast a roughly 2% decline in total TurboTax Online units and expects its share of e-file tax returns to slip by about one percentage point.

That outlook fed a broader market narrative that AI assistants are starting to absorb workflows once handled by dedicated software platforms. Investors have raised similar questions around enterprise software leaders including Adobe, Salesforce, and ServiceNow. In Intuit’s case, concern is more immediate because tax filing is a structured workflow that generative AI may help simplify over time. Management pushed back on the idea that the layoffs were caused by AI, saying the restructuring is aimed at reducing complexity, flattening management layers, and reallocating resources to growth priorities.

Is the restructuring a warning sign?

The workforce cut is large enough that investors are treating it as more than a routine efficiency move. Intuit expects restructuring charges of $300 million to $340 million, mostly in the fourth fiscal quarter. Management framed the changes as a way to improve agility and accelerate product delivery, but the timing made the move look defensive to the market.

There were still areas of strength. Global Business Solutions revenue climbed 15% to $3.3 billion, while Online Ecosystem revenue rose 19% to $2.5 billion. Excluding Mailchimp, growth was even stronger. Credit Karma revenue increased 15% to $631 million, while ProTax was flat at $278 million. Those figures suggest the broader platform is holding up better than the stock action implies. Still, when a company tied closely to tax season cuts thousands of jobs right after reporting, Wall Street tends to assume tougher demand or a more disruptive competitive backdrop is emerging.

Analyst reaction has started to reflect that caution. Barclays cut its price target to $443 from $540 after the report, even while some market observers argued the quarter itself was solid. For comparison, other megacap tech names such as NVIDIA and Apple have recently been rewarded for earnings beats, showing how differently investors now treat software names facing AI substitution risk.

What should investors watch next?

The next key metric is whether Intuit can keep shifting customers toward assisted and higher-value offerings fast enough to offset pressure in do-it-yourself filing. Paying units are expected to grow about 2%, helped by higher average revenue per user, while pay-nothing customers are projected to fall to around 7 million from 8 million a year ago. That mix shift can support revenue, but only if customer acquisition remains healthy.

Related Coverage: We recently looked at the first market reaction in Intuit Earnings Drop 15% After Hours Despite Raised Outlook. That piece breaks down why stronger guidance failed to calm the market and how AI worries around TurboTax changed the tone almost immediately after the release.

Intuit Earnings show a company still growing, but one that now has to prove its tax franchise can hold up as AI changes consumer behavior. For investors, the raised outlook matters less than whether TurboTax units stabilize and the restructuring produces real operating leverage. The next quarter should show whether this sell-off was an overreaction or the start of a deeper reset for Intuit Inc..