Can IonQ Commercialization justify premium valuations as quantum rivals fall behind and cash burn keeps climbing?

Why Is IonQ Commercialization Driving Divergence?

Over the past six months, IonQ, Inc. has delivered positive returns while D-Wave Quantum, Rigetti Computing, and Quantum Computing Inc. all declined — despite similar headlines about R&D milestones. This isn’t random volatility; it’s a structural shift. Investors are no longer treating quantum computing as a monolithic theme. Instead, they’re applying classic Wall Street filters: revenue growth, customer contracts, and balance sheet discipline. IonQ Commercialization — anchored by the University of Cambridge deployment and federal defense contracts — has become the benchmark against which peers are now measured. That’s why IonQ shares rose 30% year to date even as the broader quantum ETF (QTUM) gained only 54% with far lower concentration risk.

How Does IonQ Compare to Tech Giants?

Unlike NVIDIA, which builds quantum-classical hybrid infrastructure via CUDA-Q, or Microsoft and IBM, which embed quantum access into cloud platforms, IonQ, Inc. offers a vertically integrated trapped-ion hardware stack — a high-risk, high-differentiation bet. Its Q1 2026 revenue of $64.67 million reflects not software subscriptions but multimillion-dollar system sales and government contracts. That contrasts sharply with peers burning cash without revenue: Rigetti reported $1.2 million in Q1 revenue, D-Wave $4.8 million. IonQ Commercialization is also drawing strategic validation — Citigroup recently upgraded IonQ, Inc. to ‘Neutral’ with a $62 price target, citing ‘de-risked execution’ and ‘clear path to $265M full-year revenue.’ Meanwhile, RBC Capital Markets maintains an ‘Underperform’ rating on Rigetti, citing ‘lack of commercial inflection.’

What’s Behind the $151M Cash Burn?

IonQ, Inc. reported $151.02 million in operating cash burn in Q1 — a figure that underscores the capital intensity of scaling quantum hardware. Yet that burn is now tied directly to revenue-generating activities: manufacturing, system deployment, and engineering support for the Cambridge and Space Development Agency contracts. The $128.52 million in stock-based compensation reflects aggressive talent acquisition in a tight quantum engineering labor market — not speculative overhead. This contrasts with Quantum Computing Inc., which reported $8.3 million in cash burn on just $2.1 million in revenue. IonQ Commercialization isn’t hiding behind R&D opacity; it’s transparently funding go-to-market scale. As one Wall Street analyst noted, ‘This isn’t burn for burn’s sake — it’s burn with invoices.’

Is the Market Ready for Quantum Revenue?

Yes — but selectively. The January 2025 comments by NVIDIA CEO Jensen Huang catalyzed a sector-wide selloff, yet they also clarified the market’s new threshold: practical applications, not theoretical timelines. IonQ Commercialization delivers exactly that — quantum advantage in materials simulation for defense logistics and molecular modeling for pharma. Bloomberg reports that IonQ’s systems are now live in three U.S. national labs and two Fortune 50 R&D centers. That’s not ‘future potential’ — it’s current utilization. Meanwhile, the Defiance Quantum ETF (QTUM), which owns IonQ, Inc. as its second-largest holding, emphasizes diversification precisely because single-stock quantum exposure remains venture-grade. IonQ Commercialization is real, but it’s also high-stakes: its trapped-ion architecture has no margin for error against superconducting or photonic alternatives backed by Alphabet and Honeywell.

What’s Next for IonQ Commercialization?

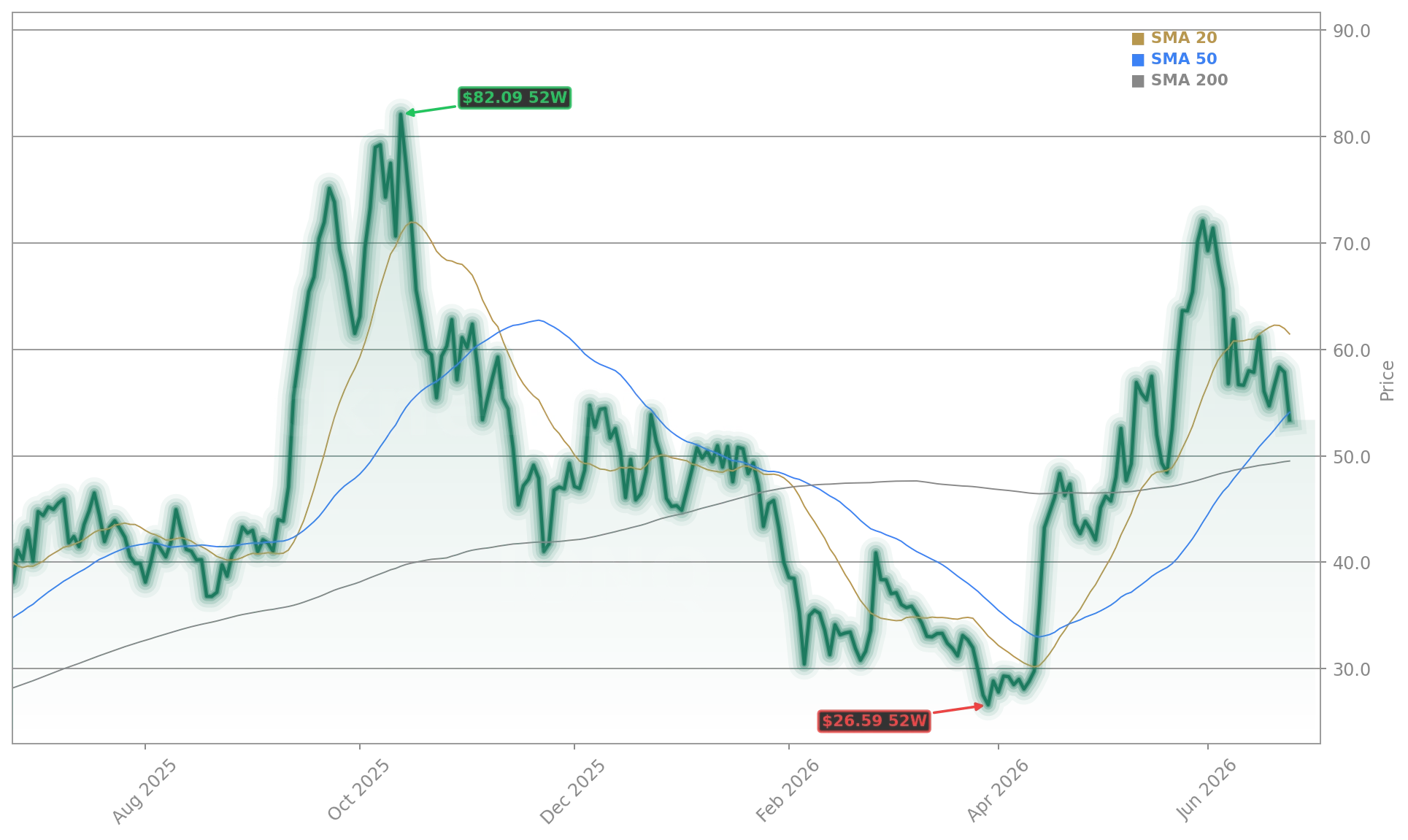

IonQ, Inc. has raised full-year 2026 revenue guidance to $260–$270 million — a target that implies $200M+ in second-half revenue. That hinges on closing at least two additional 256-qubit system contracts before Q3 earnings. The company also plans to begin shipping its next-gen 1,024-qubit ‘Forte’ platform in Q4, with pre-orders already placed by a major European aerospace consortium. Morgan Stanley analysts recently affirmed their ‘Overweight’ rating, stating, ‘IonQ Commercialization is the only quantum hardware story with a visible, contract-backed revenue ramp — and it’s accelerating.’ With the stock trading at $53.22 — near its 52-week support zone — technical buyers are watching for a sustained break above $57.50 to confirm institutional accumulation.

IonQ Commercialization is the only quantum hardware story with a visible, contract-backed revenue ramp — and it’s accelerating.— Morgan Stanley analyst

Related coverage shows how sharply IonQ Commercialization reshapes valuation debates: IonQ Acquisitions: Stock Drops 9.9% After Record Revenue explores whether M&A can deepen its hardware moat, while Qualcomm Acquisition $3.9B Sends Stock Lower Before AI Push highlights how semiconductor leaders are pivoting to quantum-adjacent AI infrastructure — a trend that both competes with and validates IonQ’s roadmap. For investors, the message is clear: IonQ Commercialization has moved beyond theory into contractually backed execution. IonQ Commercialization is no longer a question of ‘if’ — it’s a question of scale and sustainability. IonQ Commercialization defines the new quantum investment paradigm on Wall Street. For portfolios seeking exposure to the next wave of computing infrastructure, IonQ, Inc. is the first pure-play quantum company to pass the commercial viability test.