Can Lucid Financing buy enough time for a real turnaround, or is Wall Street just cheering another expensive lifeline?

What Does the $800M Lucid Financing Mean for Wall Street?

Lucid Group, Inc. executed a $800 million draw from its Delayed Draw Term Loan (DDTL) facility with Ayar Third Investment Company — an affiliate of Saudi Arabia’s Public Investment Fund — on Sunday, July 6, 2026. The move, filed with the SEC on Form 8-K, marks the largest single capital infusion since the company’s 2021 SPAC listing. Unlike equity dilution, this Lucid Financing is debt-based and carries no immediate equity conversion triggers, preserving existing shareholder stakes. For U.S. investors, the timing is critical: the capital arrives just as Q3 2026 production planning begins and as competitors like Tesla report record deliveries and NVIDIA powers next-gen EV compute stacks. The facility’s terms — including a 7.25% interest rate and maturity in 2031 — are broadly in line with recent EV-sector debt offerings, according to Bloomberg analysis.

How Does This Compare to Rivals’ Capital Strategies?

While Lucid Group, Inc. relies on strategic sovereign financing, peers pursue divergent paths. Tesla maintains a fortress balance sheet with $29.3 billion in cash and zero long-term debt. Meanwhile, Rivian (RIVN) recently raised $2.5 billion in convertible notes, and Fisker (FSR) filed for Chapter 11 — underscoring how fragile capital structures remain across the EV startup cohort. Morgan Stanley analysts noted in a July 5 report that ‘Lucid’s access to non-dilutive, long-dated capital gives it a 12–18 month runway advantage over peers without sovereign backing.’ That buffer matters: LCID reported $1.2 billion in cash at end-Q1 2026, but burn averaged $380 million per quarter. This Lucid Financing extends liquidity into early 2028 — a window investors now see as essential for executing its new CEO’s turnaround plan.

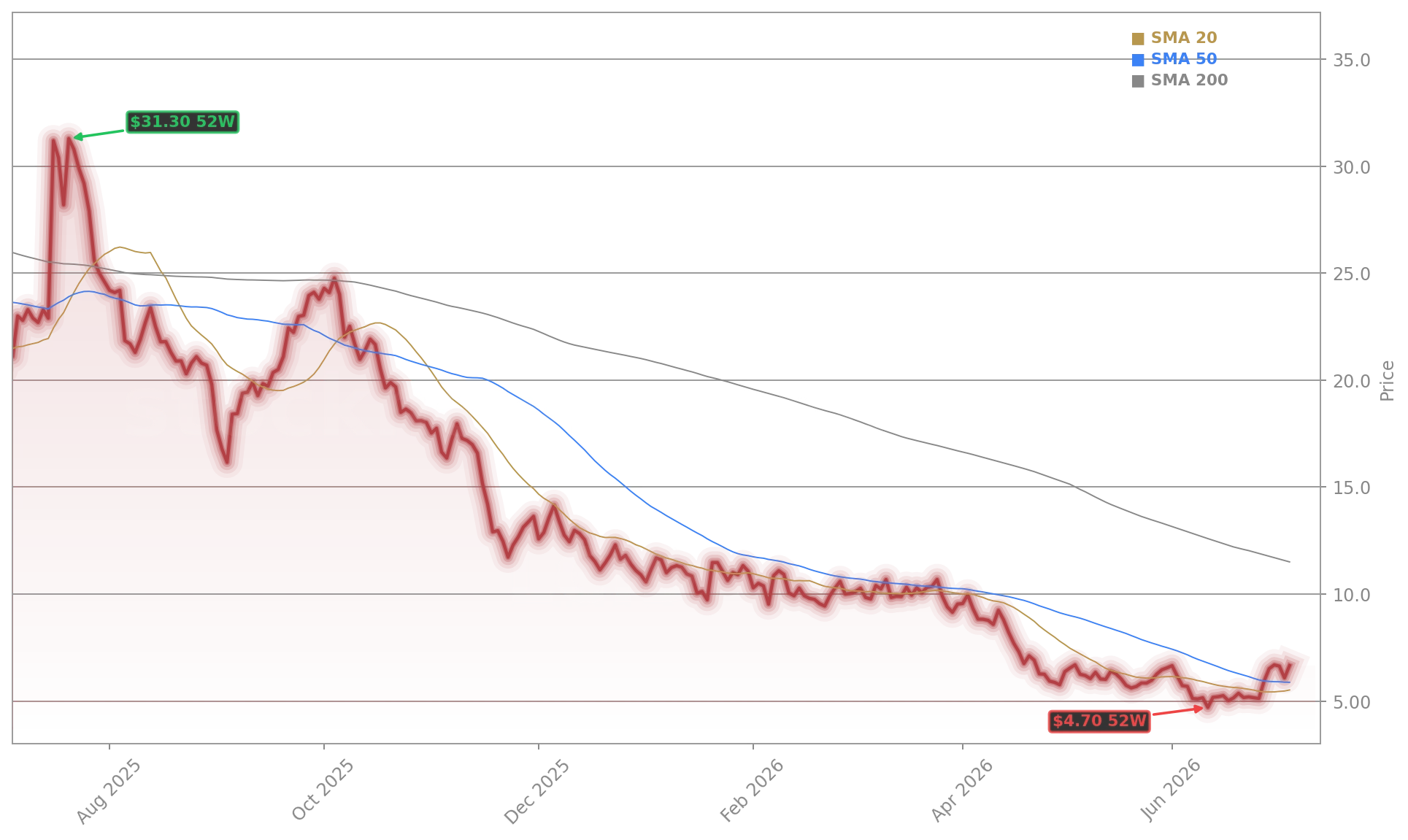

Is the Stock Rally Sustainable Beyond Technical Bounce?

LCID surged 9.21% to $6.64 on Tuesday pre-market, breaking above both its 20-day ($5.52) and 50-day ($5.87) moving averages — a rare positive technical signal since early 2025. Yet resistance looms at $7.00, just beneath its 100-day SMA ($7.71). RBC Capital Markets downgraded LCID to ‘Underperform’ in June, citing ‘persistent gross margin headwinds and unproven scalability beyond luxury segments.’ In contrast, Citigroup upgraded the stock to ‘Neutral’ on July 5, raising its 12-month price target to $8.50, citing ‘improved capital discipline and clearer path to Lucid Air S production.’ The divergence reflects Wall Street’s split view: one camp sees Lucid Financing as a lifeline, the other as a delay tactic in a market where scale — not specs — now defines valuation.

What’s Next for Lucid Group, Inc. in Q3 2026?

With fresh capital secured, Lucid Group, Inc. shifts focus to execution. The company recently suspended full-year 2026 production guidance but confirmed it will begin deliveries of the Lucid Air S — its volume-targeted model — in late Q3. Analysts at Goldman Sachs estimate Air S could double quarterly deliveries to ~7,000 units by year-end, assuming supply chain stability. Crucially, Lucid’s battery and powertrain IP remains highly sought after: the company is in advanced talks with three European OEMs for licensing agreements, per a Reuters report. If monetized, those deals could generate $150–$200 million in non-automotive revenue by Q4 — a potential catalyst beyond Lucid Financing alone.

Related Coverage

This draw reflects our disciplined capital strategy — prioritizing non-dilutive funding while maintaining strategic optionality for growth.— Peter Rawlinson, CEO of Lucid Group, Inc.

For deeper context on how this capital event fits into LCID’s broader recovery narrative, see Lucid Financing +9.2% as Lucid Draws $800M Credit Line, where Editor-in-Chief Maik Kemper analyzes whether this draw can convert a sharp stock bounce into durable momentum. The piece also explores how the new CEO’s capital discipline compares to prior leadership — a key factor for long-term investors assessing risk amid the broader S&P 500’s 12% YTD rally in tech and auto components.