Can Lucid Financing finally ease liquidity fears enough to turn a sharp stock bounce into a more durable recovery?

What Does the $800M Draw Mean for Lucid Financing?

Lucid Group, Inc. activated $800 million under its Delayed Draw Term Loan agreement with Ayar Third Investment Company — an affiliate of Saudi Arabia’s Public Investment Fund. The draw, executed on July 6, 2026, was formally reported in a Form 8-K filed with the U.S. Securities and Exchange Commission — a mandatory disclosure for material financial obligations. Unlike equity dilution, this Lucid Financing action preserves shareholder ownership while adding near-term operating flexibility. It also signals continued institutional confidence in Lucid’s long-term roadmap, especially as the company prepares for its Q3 2026 production ramp and potential expansion of its Arizona manufacturing footprint. With cash and equivalents expected to rise significantly post-draw, Lucid Group, Inc. now holds greater capacity to fund engineering milestones, battery supply agreements, and U.S. service network buildout — all critical for competing with Tesla and NVIDIA-powered EV software ecosystems.

How Is Lucid Group, Inc. Positioned Against EV Peers?

While Lucid Group, Inc. remains smaller in scale than Tesla, its financial positioning is evolving rapidly. Tesla (TSLA) reported $25.7 billion in cash at end-Q1 2026, while Rivian (RIVN) held $12.3 billion — both benefiting from earlier capital raises and higher production volumes. Lucid Group, Inc., by contrast, is leveraging targeted, non-dilutive financing — a strategy analysts at RBC Capital Markets recently highlighted as ‘prudent for capital-constrained EV startups navigating the 2026 margin squeeze.’ Meanwhile, NVIDIA’s Blackwell architecture is accelerating AI-driven vehicle development across the sector, raising the bar for software-defined EV competitiveness. Lucid’s upcoming Q3 delivery report — expected by mid-August — will be closely watched not just for volume but for gross margin trajectory, which remains below industry averages. Citigroup maintains a ‘Neutral’ rating on Lucid Group, Inc. with a $7.25 price target, citing ‘execution risk but improving balance sheet discipline.’

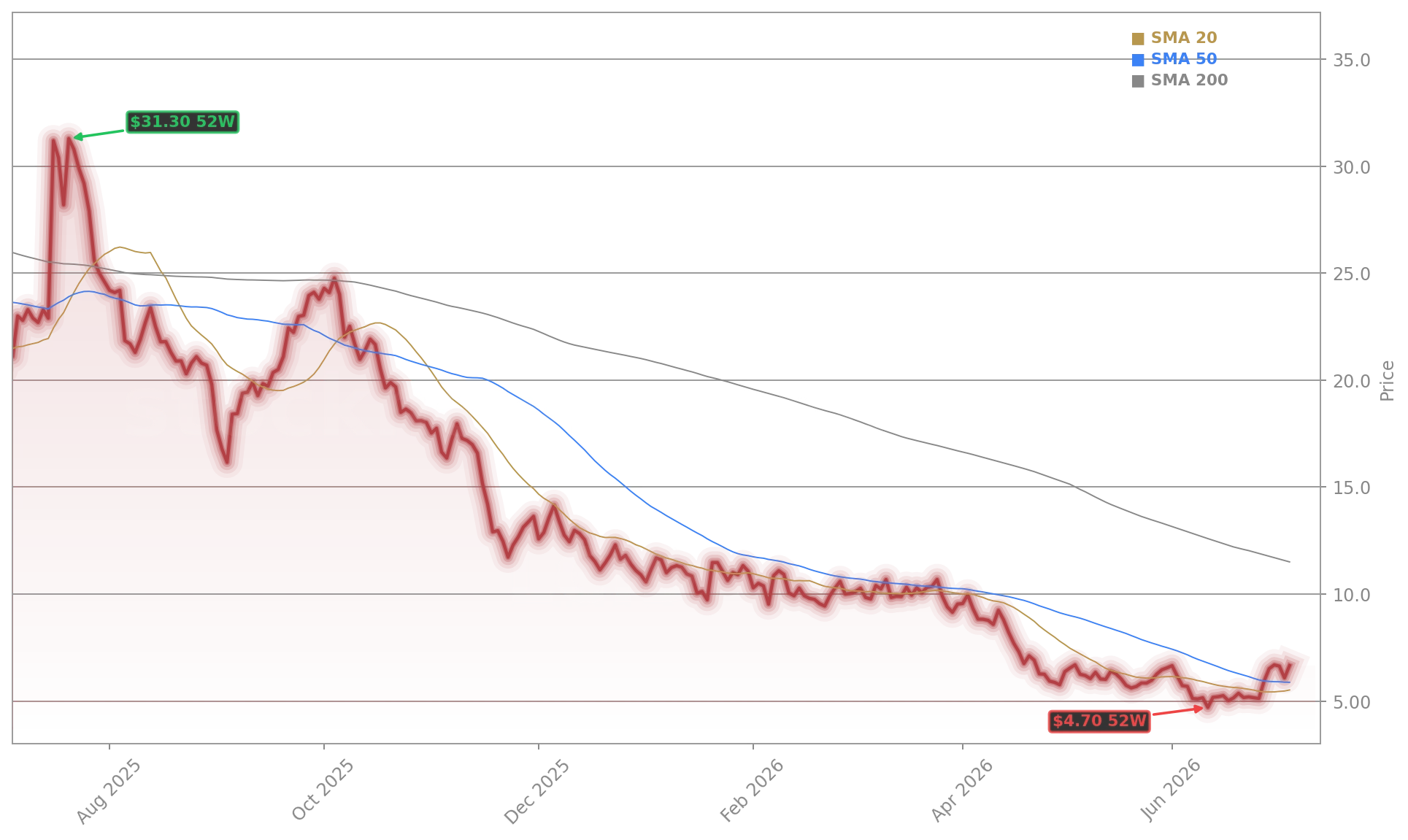

Why Did Lucid Financing Trigger a 9.2% Pre-Market Jump?

The $800 million Lucid Financing event coincided with reinforcing macro signals for EV demand. According to Reuters, battery electric vehicles captured 29.8% of new car registrations in the UK in June — the strongest non-seasonal monthly share on record. That data point matters: it validates broadening mainstream adoption, a tailwind for premium EV makers like Lucid Group, Inc. Technical indicators also shifted favorably: LCID reclaimed both its 20-day ($5.52) and 50-day ($5.87) moving averages — a rare positive crossover after months of underperformance. Though still below its 100-day ($7.71) and 200-day ($11.50) averages, the MACD histogram turned positive, suggesting short-term momentum has gained traction. With resistance near $7.00, a sustained break above that level could trigger algorithmic buying and options flow — making Lucid Financing not just a balance sheet event, but a catalyst for renewed Wall Street attention.

What’s Next for Lucid Group, Inc. and Its Investors?

Investors now pivot to Q3 2026 delivery guidance — expected in mid-August — and the company’s ability to convert liquidity into tangible output. Lucid Group, Inc. aims to produce over 22,000 vehicles in 2026, up from 12,100 in 2025. That growth hinges on battery cell supply stability and service center deployment pace. Morgan Stanley analysts note that ‘Lucid Financing reduces near-term liquidity risk, but margin expansion remains the true inflection point for valuation re-rating.’ Meanwhile, broader NASDAQ exposure to EVs remains elevated, with the index up 4.3% year-to-date — outperforming the S&P 500’s 2.1% gain. For U.S. investors holding tech- or auto-linked ETFs, Lucid Group, Inc.’s progress matters as a barometer of capital efficiency in the next-generation EV race.

This draw reflects our disciplined capital strategy — prioritizing non-dilutive funding while maintaining optionality for growth investments.— Peter Rawlinson, CEO of Lucid Group, Inc.

Related Coverage: Lucid’s recent CFO appointment follows a 7.8% stock decline after a Q2 delivery miss, raising questions about leadership continuity amid accelerating production timelines. The same article highlights investor concerns over litigation risk and supply chain execution, underscoring why the $800 million Lucid Financing move is being viewed as both defensive and strategic.