Can the Moderna Flu Vaccine turn an FDA panel win into a real growth story before Wall Street loses patience?

What Does the FDA Vote Mean for Moderna, Inc.?

The FDA’s Vaccines and Related Biological Products Advisory Committee (VRBPAC) delivered a decisive 9–0 recommendation in favor of Moderna’s seasonal flu vaccine for adults aged 50 and older — a pivotal validation of its mRNA platform beyond pandemic applications. While the FDA retains full discretion, historical precedent shows it follows VRBPAC recommendations approximately 85% of the time. A final decision is expected by August 6, 2026 — placing the Moderna Flu Vaccine squarely in the crosshairs of Q3 2026 positioning for institutional investors. Notably, this isn’t a rebrand of an existing product: it’s a novel mRNA-based flu vaccine with demonstrated 52.9% relative efficacy versus standard quadrivalent flu shots in Phase 3 trials — a statistically significant advantage that could reshape seasonal immunization economics across the U.S. healthcare system.

How Does Moderna, Inc. Compare to Biotech Peers?

Unlike legacy vaccine players such as Merck or Sanofi, Moderna, Inc. brings platform scalability, rapid manufacturing iteration, and digital supply chain integration — traits increasingly valued in post-pandemic biotech investing. Its pipeline now includes three commercial-stage assets, a flu/COVID-19 combination vaccine in Phase 3, a norovirus candidate entering Phase 2b, and a personalized cancer vaccine co-developed with Merck showing 49% recurrence-free survival improvement in advanced melanoma (data expected Q4 2026). This diversification contrasts sharply with peers like NVIDIA, whose AI-driven growth is hardware-constrained, or Tesla, where regulatory approvals are product-cycle dependent rather than platform-based. Moderna’s mRNA technology, meanwhile, shares infrastructure across indications — a structural advantage for capital efficiency that Wall Street is now pricing in.

Is the Moderna Flu Vaccine Enough to Offset Valuation Risk?

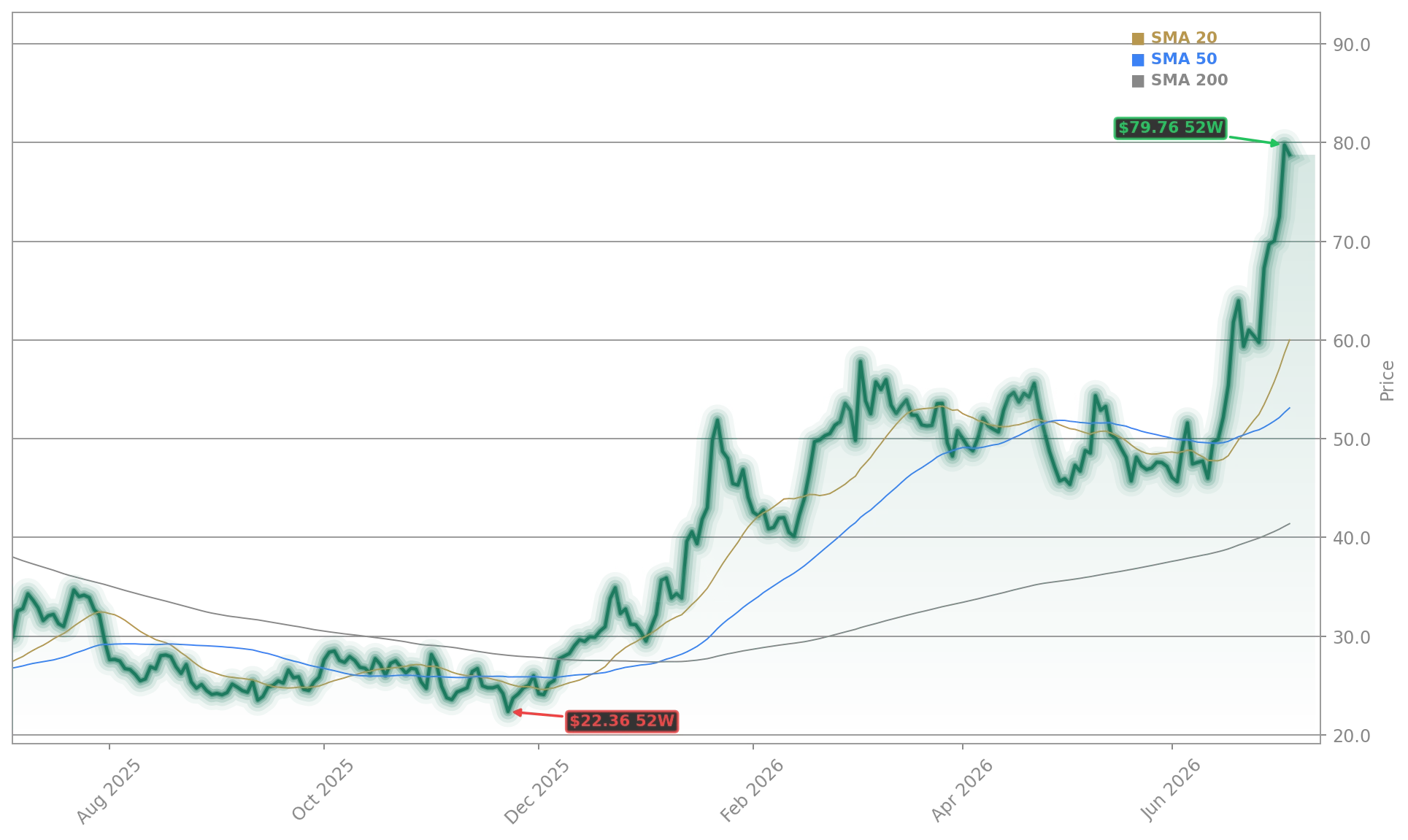

Despite a 112% year-to-date gain, Moderna, Inc. trades at a forward P/S ratio of 12.3x — above the biotech sector median of 5.8x — reflecting aggressive expectations for the Moderna Flu Vaccine and upcoming launches. Revenue jumped to $389 million in Q1 2026 from $108 million a year earlier, yet net losses persist. Crucially, Moderna, Inc. ended Q1 with $7.5 billion in cash and short-term investments, giving it runway well into 2028 — the year management targets cash breakeven. Still, B of A Securities maintains an Underperform rating on Moderna, Inc. and raised its price target to $38, citing near-term revenue concentration risk and limited visibility beyond 2027. That contrasts with RBC Capital Markets, which upgraded its rating to Sector Perform and lifted its price target to $45, emphasizing the Moderna Flu Vaccine’s $2.1 billion peak U.S. sales potential and platform leverage into oncology.

What’s Next for Moderna, Inc. Beyond the Flu Shot?

The Moderna Flu Vaccine is just the opening act. A flu/COVID-19 combination vaccine enters U.S. Phase 3 trials this month, with potential 2027 launch timing. Separately, Moderna, Inc. and Merck are advancing mRNA-based personalized cancer vaccines — a program that could redefine adjuvant therapy for melanoma, non-small cell lung cancer, and renal cell carcinoma. Early data from the KEYNOTE-942 trial suggests a 44% reduction in recurrence versus pembrolizumab alone. Meanwhile, in vivo CAR-T programs — highlighted in recent coverage as a potential multi-billion-dollar platform — are now entering IND-enabling studies. That work could position Moderna, Inc. not just against traditional pharma, but as a structural challenger to Apple-backed AI-driven drug discovery platforms and Tesla-adjacent biomanufacturing automation plays. The company’s 2026 revenue target of 10% growth — modest by biotech standards — reflects disciplined capital allocation amid pipeline de-risking.

Related Coverage

The 9–0 VRBPAC vote isn’t just about flu — it’s the first FDA endorsement of mRNA for a seasonal, non-emergency indication. That changes the entire regulatory playbook.— Luca Issi, RBC Capital Markets

For deeper analysis of Moderna’s platform expansion beyond vaccines, see Moderna Strategy +13%: In Vivo CAR-T Surge Lifts MRNA, which details how its next-generation cell therapy pipeline could unlock $8–12 billion in annual revenue by 2030. The article underscores how the Moderna Flu Vaccine serves as both a near-term catalyst and a proof point for broader mRNA delivery validation — a critical bridge to high-margin oncology and rare disease markets.