Can Moderna’s pipeline story outweigh a brutal valuation reset, or is the latest sell-off warning investors not to chase the rally?

Why Did Moderna Forecast Diverge So Sharply?

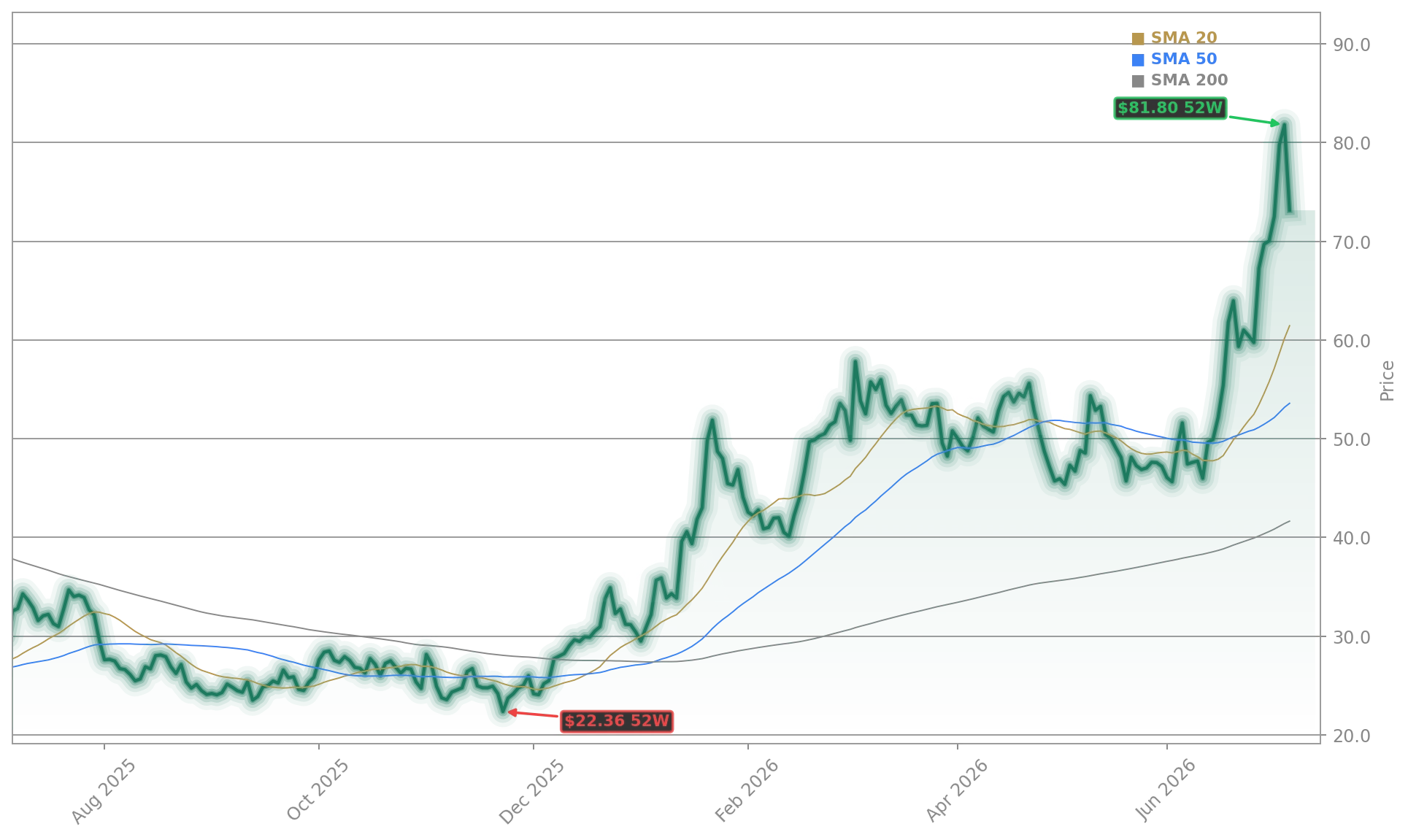

Moderna, Inc. plunged 8.2% to $73.23 after a 48% rally in June — its strongest monthly gain since 2023 — fizzled amid broad rotation into tech and information-technology names like Broadcom and Arista Networks. The selloff occurred despite no material negative news, suggesting technical exhaustion and profit-taking. Barron’s noted Moderna was the S&P 500’s biggest loser early in the session, trailing only Synchrony Financial. The stock’s retreat from its $81.80 Monday close — its highest since August 2024 — signals growing skepticism about whether recent gains reflect durable value or short-term speculation.

What Does Morgan Stanley’s $39 Target Mean for Investors?

Morgan Stanley analyst Matthew Harrison maintained an Equal-Weight rating on Moderna, Inc. while lifting the price target from $33 to $39 — a 48% downside from current levels. The move reflects cautious optimism on pipeline progress but persistent concerns about revenue diversification and near-term profitability. Notably, Harrison’s upgrade was not accompanied by a rating change, underscoring institutional hesitation. Meanwhile, Bank of America Securities analyst Alex Stranahan kept a Sell rating with a $38 target, warning that shares have ‘overshot implied value’ from upcoming data readouts — particularly for intismeran, the personalized melanoma vaccine expected to report preliminary efficacy in late 2026.

How Does Moderna Forecast Compare to Biotech Peers?

Unlike peers such as Regeneron or Vertex, Moderna, Inc. lacks near-term commercial revenue beyond its flu and RSV vaccines — both still scaling. Its $37.87 consensus price target (per MarketBeat) implies 49% average downside, far steeper than the 12% average for S&P 500 healthcare stocks. While Tesla and NVIDIA are driving tech-led momentum on Wall Street, biotech valuations remain fragile: the iShares Biotechnology ETF (IBB) is up just 2.1% YTD versus the NASDAQ’s 18.3% gain. Institutional selling reinforces caution — HSBC Holdings PLC reduced its stake by 14.4% and Meitav Investment House cut its position by 37.2% in Q1, citing valuation risk.

Is the Pipeline Pivot Enough to Shift the Moderna Forecast?

Moderna, Inc. is executing a strategic pivot toward in vivo CAR-T and multi-antigen vaccines — a shift highlighted at its June investor day. Chief Scientific Officer Lin Guey emphasized scalability of its ‘off-the-shelf’ mRNA-engineered T-cell therapy, slated for clinical development in 2027. The company also appointed former Biogen CFO Michael McDonnell to its Board and Audit Committee, strengthening financial governance ahead of potential late-stage launches. Yet, analysts remain divided: while Ad Hoc News calls the strategy ‘bullish’, Trefis rates MRNA ‘Very Unattractive’ due to weak operating performance and high valuation. The Moderna Forecast hinges less on past success and more on whether intismeran, flu, and RSV data can trigger commercial inflection in 2027 — not 2026.

What’s Next for Moderna Forecast and Q2 Earnings?

Q2 2026 results — expected in late July — will test the Moderna Forecast under renewed pressure. Revenue guidance remains muted, and the GAAP net loss widened to $1.34 billion in Q1, per The Globe and Mail. With insider selling accelerating — over 125,000 shares sold by executives in 90 days — investor patience is thin. Still, the company’s $5.2 billion cash position and 75.33% institutional ownership (led by Vanguard) provide runway. The next catalyst? FDA advisory committee feedback on the flu vaccine — a topic covered in depth in Moderna Flu Vaccine -3.4% After FDA Panel Backs Shot. That 9–0 VRBPAC vote offers tangible validation — but not immediate revenue.

Because it is off-the-shelf, you’re doing this in a person’s body, it is scalable.— Lin Guey, Chief Scientific Officer of Therapeutics Research, Moderna, Inc.

Moderna, Inc. remains at a pivotal inflection point between pandemic legacy and platform potential. For US investors, the Moderna Forecast is no longer about speed of execution — it’s about sustainability of monetization. The next quarterly earnings will determine whether the narrative shifts from hope to hard metrics. For long-term portfolios exposed to biotech volatility, disciplined position sizing and clear catalyst timelines are essential.