Are Netflix Earnings really as strong as the headline numbers suggest, or is weak guidance quietly rewriting the bull case?

Why did Netflix Earnings spark a selloff?

The latest Netflix Earnings report for Q1 2026 looked impressive at first glance. Revenue climbed 16% year over year to $12.25 billion, modestly ahead of Wall Street’s roughly $12.18 billion consensus. Earnings per share surged to $1.23 versus expectations near $0.76, helped by a one‑time $2.8 billion breakup fee tied to the failed Warner Bros. Discovery deal. Excluding that fee, underlying EPS would have been closer to $0.58, still profitable but far less spectacular.

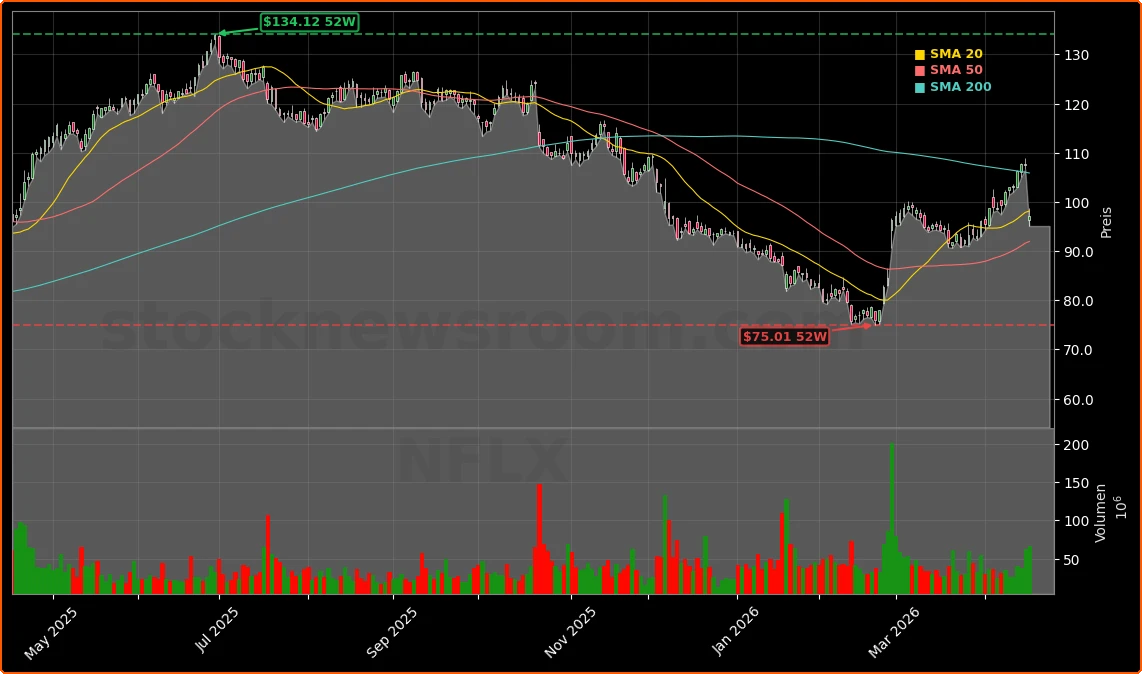

Despite the beat, the stock is down about 9.87% on the day, trading near $97 versus Thursday’s $97.35 close and well below its 52‑week high around $134. The pressure stems from Netflix’s outlook: management guided Q2 revenue to about $12.57 billion and EPS to $0.78, both below consensus estimates of roughly $12.63–12.64 billion and $0.84 respectively. The company also kept its full‑year 2026 revenue range intact with a midpoint near $51.2 billion, rather than raising it after the Q1 upside and March price hikes.

That lack of a classic “beat and raise” quarter has been a key trigger for profit‑taking, especially after the stock had rallied roughly 40% off its February lows into the print. With Netflix Earnings now seen as “good but not great,” traders are rapidly resetting expectations.

How important is Reed Hastings stepping down?

The other big headline from the Netflix Earnings release is the end of an era: co‑founder and chairman Reed Hastings will not stand for re‑election at the June shareholder meeting, fully stepping away from formal leadership after nearly three decades. Hastings had already ceded the CEO role to co‑CEOs Ted Sarandos and Greg Peters in 2023, but his presence on the board was viewed by many as a strategic anchor.

Hastings framed the move as a chance to focus on philanthropy and other pursuits, praising Netflix’s culture and its leadership bench. On the call, Sarandos described him as “a true history maker,” while Peters emphasized how Hastings’ focus on “member joy” and innovation shaped every stage of the company’s evolution from DVD‑by‑mail to global streaming leader.

Several analysts, including Rosenblatt’s Barton Crockett, argue Hastings’ exit is not a fundamental thesis-breaker but acknowledge it adds to investor unease in a week when guidance already disappointed. Market history suggests founder departures at tech giants—from Bill Gates at Microsoft to Hasso Plattner at SAP—do not automatically derail returns, but short‑term sentiment often wobbles.

What are analysts saying about Netflix Earnings?

Reaction across Wall Street to the Netflix Earnings print has been mixed but not outright bearish. Seaport Research Partners’ David Joyce kept a Buy rating and even raised his price target from $115 to $119, arguing that clarity after abandoning the Warner Bros. Discovery bid should ultimately help sentiment. He sees upside toward $138 if the ad business and live/gaming initiatives outperform.

On the cautious side, Barclays analyst Kannan Venkateshwar cut his target from $115 to $110 while maintaining an Equal Weight stance, warning that the negative reaction to guidance could linger given elevated expectations after recent price hikes. Bernstein’s Laurent Yoon also trimmed his target from $115 to $110 but kept an Outperform rating, noting that fundamentals look intact even as a step‑up in content spending raises questions about longer‑term margin expansion.

Banks remain broadly constructive: JPMorgan reiterated an Overweight with a slightly reduced $118 target and explicitly recommended buying the post‑earnings weakness. Morgan Stanley likewise argued the valuation now looks compelling, seeing the Q2 miss as partly timing‑related to U.S. price increases and content amortization. Needham’s Laura Martin highlighted Netflix’s push into mobile‑first engagement like vertical video, kids’ games and video podcasts as a way to defend screen time against YouTube and TikTok and ultimately monetize via both subscriptions and advertising.

Can Netflix still grow without an AI “hype” story?

A recurring theme in commentary around the latest Netflix Earnings is the company’s position in a market obsessed with AI‑linked growth. While mega‑caps like NVIDIA, Apple and other AI beneficiaries command premium multiples, Netflix is increasingly viewed as a pure entertainment platform, targeting low‑teens revenue growth and high single‑digit to roughly 20% EPS growth rather than explosive AI‑driven expansion.

Management is leaning into pricing power, engagement and advertising instead. Co‑CEO Greg Peters defended recent U.S. price hikes, arguing that Netflix still offers one of the lowest “cost per hour watched” among major streaming services and that retention actually strengthened across regions in Q1. The ad‑supported tier at $8.99 per month continues to scale: in markets where it is available, around one‑third of the base uses it, and Netflix is targeting about $3 billion in 2026 ad revenue, roughly double last year.

At the same time, content investment is set to climb toward roughly $20 billion this year, above historical growth rates, as Netflix bets heavily on live events and sports. The World Baseball Classic delivered record viewership in Japan, and the company is in discussions to deepen its relationship with the NFL, while maintaining its focused, event‑driven approach rather than buying full‑season rights. These initiatives, combined with targeted M&A such as the acquisition of Ben Affleck–backed AI tools firm Interpositive, show management is not ignoring technology but prioritizing monetizable engagement over pure AI narrative.

Related coverage on Netflix Earnings

For a deeper dive into how guidance, content spending and leadership risks converged to turn a headline beat into a double‑digit drop, readers can explore detailed analysis of the Netflix Earnings shock and outlook reset. That piece also examines how the Reed Hastings transition could reshape the company’s strategic risk profile and what the current valuation implies versus other U.S. tech and media names.

In addition, sector‑focused investors may find it useful to read the broader streaming and media takeaways in this companion look at Netflix Earnings and the shifting competitive landscape, which contrasts Netflix’s guidance stumble with the more AI‑centric growth stories at other NASDAQ heavyweights and outlines how ad‑tier economics could evolve across the industry.

Maybe this is just a wobble that everyone should ignore.— Barton Crockett, Rosenblatt Securities

Ultimately, the latest Netflix Earnings underline a clear message for U.S. portfolios: this is no longer a hyper‑growth story, but a cash‑generating media platform balancing price hikes, heavier content spend and ad‑tier expansion. The stock’s sharp pullback brings valuation back toward a more reasonable range, and the next few quarters—especially evidence of sustained ad growth and engagement—will determine whether this earnings wobble proves to be a buying opportunity or an early warning of slower days ahead.