Did Nike Earnings really mark a turnaround, or did one-time gains simply hide deeper problems investors can no longer ignore?

Why Did Nike Earnings Beat Yet Spook Investors?

Nike Earnings for the quarter ended May 31, 2026, topped consensus estimates—$10.97 billion in revenue versus $10.86 billion expected, and $0.72 EPS versus $0.14 a year ago—but the victory was pyrrhic. A $0.52 per-share benefit from U.S. import tariff refunds (stemming from the invalidation of Trump-era orders) accounted for over 70% of the EPS gain. Excluding that, underlying profitability remains strained. Gross margin jumped to 49.2%, yet wholesale revenue rose 4% while direct-to-consumer (DTC) sales fell 7% globally—a troubling inversion for a brand that spent years prioritizing digital control. As Jefferies noted, the beat was ‘expected, but not transformative.’ The stock initially fell 3% after hours before surging 4.9% intraday—reflecting not confidence, but exhaustion of pessimism.

How Does Nike Compare to Adidas and Lululemon?

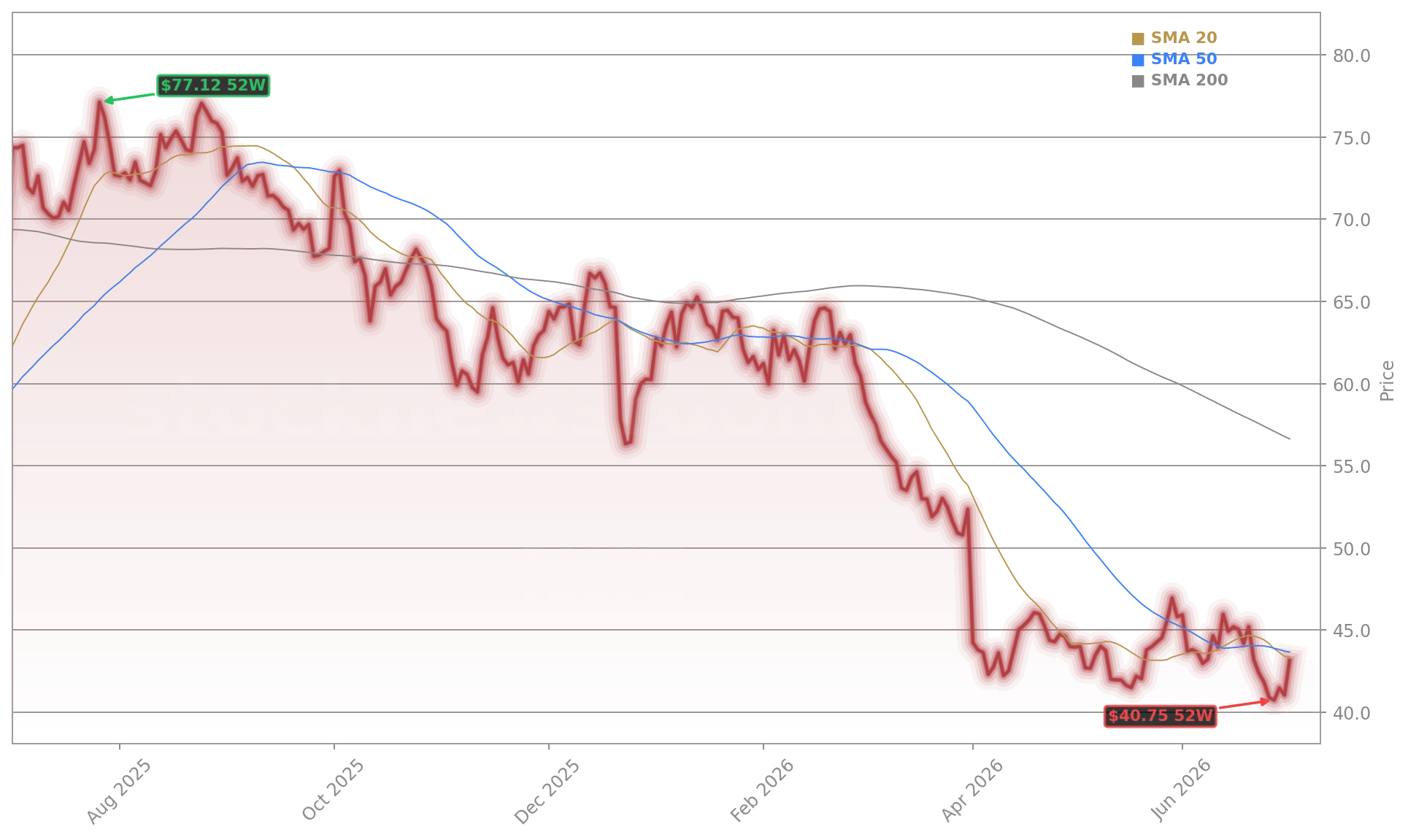

While Nike, Inc. wrestles with stagnation, Adidas and Lululemon Athletica are pulling ahead. Analyst Wendy Liu at RBC Capital Markets highlights a widening ‘execution gap’: Adidas and On Holding now anchor the ‘Constant-Deliver Camp,’ with solid growth and improving full-price sell-through, while Nike remains mired in the ‘Neustart & Wiederaufbau Camp’—a label increasingly associated with delayed execution. Lululemon’s recent earnings disappointment didn’t dent its premium valuation; Nike trades near 11-year lows despite comparable scale. With U.S. wholesale revenue up double digits for the full year—and China sales plunging 17%—Nike’s geographic imbalance deepens. Meanwhile, Adidas gains U.S. shelf space as Nike retreats, and Lululemon expands into footwear with growing traction. The competitive dynamic isn’t just about market share—it’s about investor patience. Citigroup lowered its Nike price target to $45.00, citing ‘slower-than-expected turnaround,’ while maintaining a ‘neutral’ rating.

What’s Driving the Weak Outlook for Nike Earnings?

Nike’s fiscal 2027 guidance—revenue down low-to-mid single digits—reflects three converging pressures: macro anxiety, category decay, and execution lag. CFO Matthew Friend stated bluntly: ‘Our customers are under pressure globally.’ That includes consumers hit by energy inflation, geopolitical uncertainty—including spillover from the Iran conflict—and tighter discretionary budgets. Sportswear and Jordan Streetwear, once growth engines, now drag the franchise. Running and Nike Mind delivered five straight quarters of double-digit growth, but those categories represent less than 25% of sales. Management admitted ‘we’re not living up to our full potential’ in core apparel—raising questions about brand heat and product velocity. Inventory tightening is underway, but with DTC traffic down across all regions and wholesale now carrying disproportionate growth weight, the model remains misaligned. As one Wall Street strategist put it: ‘You can’t turn around a ship when half the hull is underwater.’

Is This Nike Earnings Report a Buying Opportunity?

We know we’re not living up to our full potential, particularly in Nike sportswear and Jordan streetwear, where sell-through remains challenged.— Elliott Hill, CEO of Nike, Inc.

At $44.20, Nike trades at levels last seen in 2014—and below its 52-week high of $58.70. Jefferies retains a ‘buy’ rating despite cutting its target from $90 to $75, citing ‘long-term brand equity’ and ‘World Cup tailwinds’ (U.S. national team merch sales up 2.5x vs. 2022). Yet insiders’ confidence appears selective: CEO Elliott Hill and Director Timothy D. Cook bought shares in April, but Wesbanco Bank slashed its stake by 59% in Q1. The $3 EPS target projected by CFRA for 2028 hinges on sportswear recovery—a scenario with no visible catalyst. With the S&P 500 trading at 22x forward earnings and Nike at 27x, its valuation premium looks increasingly unjustified. For U.S. portfolios, Nike Earnings may signal opportunity—but only for investors willing to wait out a multi-year reset. As Meta and NVIDIA dominate AI-driven market leadership, Nike remains a value play in search of a narrative.