Is onsemi buying growth at exactly the moment investors wanted focus, not a risky expansion into unfamiliar markets?

Why did ON Semiconductor’s stock drop 15%?

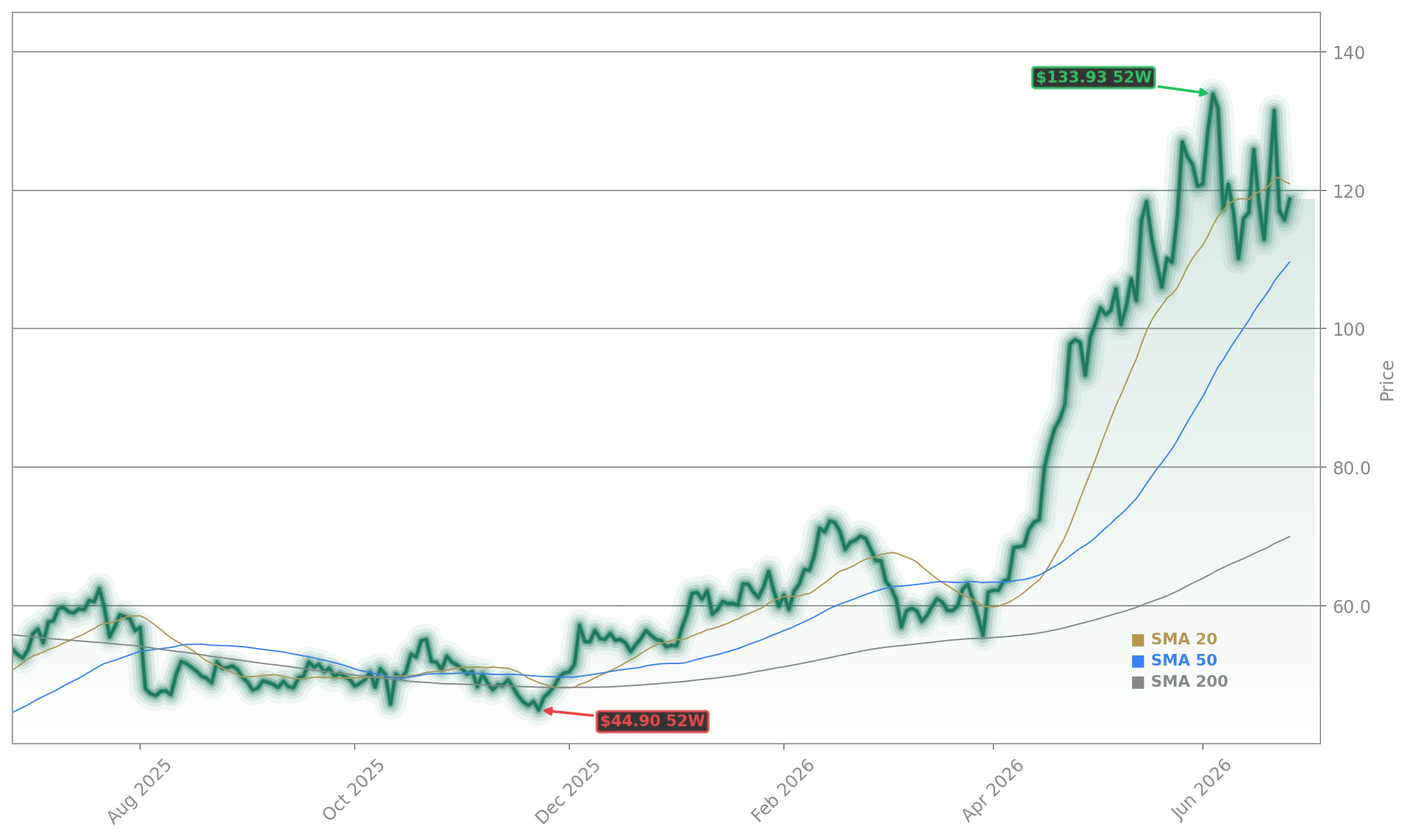

ON Semiconductor shares plunged 14.6% in pre-market trading on Friday, June 26, 2026 — the steepest single-day intraday drop since early 2025 — immediately following the announcement of its definitive agreement to acquire Synaptics. The $7 billion all-stock transaction, structured at a fixed exchange ratio of 1.350 ON shares per SYNA share, represents a 19% premium but has been met with investor skepticism. TD Cowen downgraded ON Semiconductor to ‘Hold’ from ‘Buy’, slashing its price target to $110 from $115, citing ‘increased complexity’ and ‘model dilution’ from the onsemi Acquisition. The move reflects broader concerns that ON Semiconductor is overextending beyond its automotive and industrial power-management strengths into fragmented, lower-margin edge-device markets.

What does the onsemi Acquisition mean for AI positioning?

The onsemi Acquisition is framed as a strategic leap into ‘physical AI’ — embedding intelligence directly into sensors, robotics, autonomous vehicles, and AR/VR hardware. Synaptics brings its Astra AI platform: integrated neural processing units (NPUs), microprocessors, and wireless connectivity IP. While SiliconANGLE notes the deal could expand ON Semiconductor’s total addressable market by $30 billion to $243 billion by 2030, Citigroup analysts stress that ‘more comprehensive details are needed’ on how Synaptics’ IP integrates with ON’s silicon carbide and imaging sensor roadmaps. Crucially, this pivot distances ON Semiconductor from the high-velocity, high-margin AI data center chip race dominated by NVIDIA and increasingly contested by Tesla and Apple — a narrative that had driven much of its recent valuation expansion.

How does Synaptics fit into ON Semiconductor’s portfolio?

Synaptics has long served the PC, smartphone, and smart-home markets — areas where ON Semiconductor has minimal presence. Its expertise lies in touch controllers, fingerprint sensors, and edge AI processors — valuable for smart devices but structurally less aligned with ON’s automotive and industrial customer base. The combined entity is expected to derive ~12% of revenue from consumer electronics post-close, up from near-zero today. That shift raises red flags for investors who have priced ON Semiconductor as a pure-play AI infrastructure enabler. Barron’s highlighted the disconnect: while S&P 500 futures dipped modestly in pre-market, ON Semiconductor was among the worst performers — signaling targeted investor concern rather than broad market weakness.

What are the financial risks of the onsemi Acquisition?

Though ON Semiconductor projects the deal will be accretive to non-GAAP EPS within 18 months and deliver $200 million in annual synergies, the all-stock structure introduces immediate dilution. Synaptics shareholders will own ~12% of the combined company — a significant equity issuance that increases share count by roughly 11%. With ON Semiconductor’s 2026 revenue forecast at $6.47 billion — up just 8% year-over-year after a 15% decline in 2025 — margin pressure from integration costs and lower-margin Synaptics revenue could delay EPS accretion. Moomoo and The Business Journals both note the mid-2027 closing timeline, meaning near-term execution risk looms large. As Benzinga reported, ON Semiconductor joined a list of major tech names falling in pre-market — a cohort increasingly defined by valuation recalibration amid rising interest rates and AI monetization uncertainty.

How are peers responding to the onsemi Acquisition?

The deal adds complexity to an already complicated model.— TD Cowen analyst

While ON Semiconductor retreats, peers like NVIDIA continue to rally on data center AI tailwinds — up 7% this week alone. Analog Devices (ADI) and Texas Instruments (TXN), both peers in power management and signal processing, remain flat — suggesting the market views ON’s move as idiosyncratic, not sector-wide. Synaptics’ stock rose 3.5% pre-market, reflecting shareholder approval of the 19% premium. Yet PR Newswire’s shareholder litigation alert underscores governance scrutiny: Ademi LLP is investigating whether Synaptics’ board adequately assessed alternatives. For U.S. portfolios, the onsemi Acquisition serves as a timely reminder that not all AI-related M&A creates equal value — especially when it blurs focus in a high-velocity sector.