Can Applied Materials AI Systems justify the hype after a sharp pullback, or is the market finally questioning the AI capex trade?

What triggered AMAT’s 13% intraday surge?

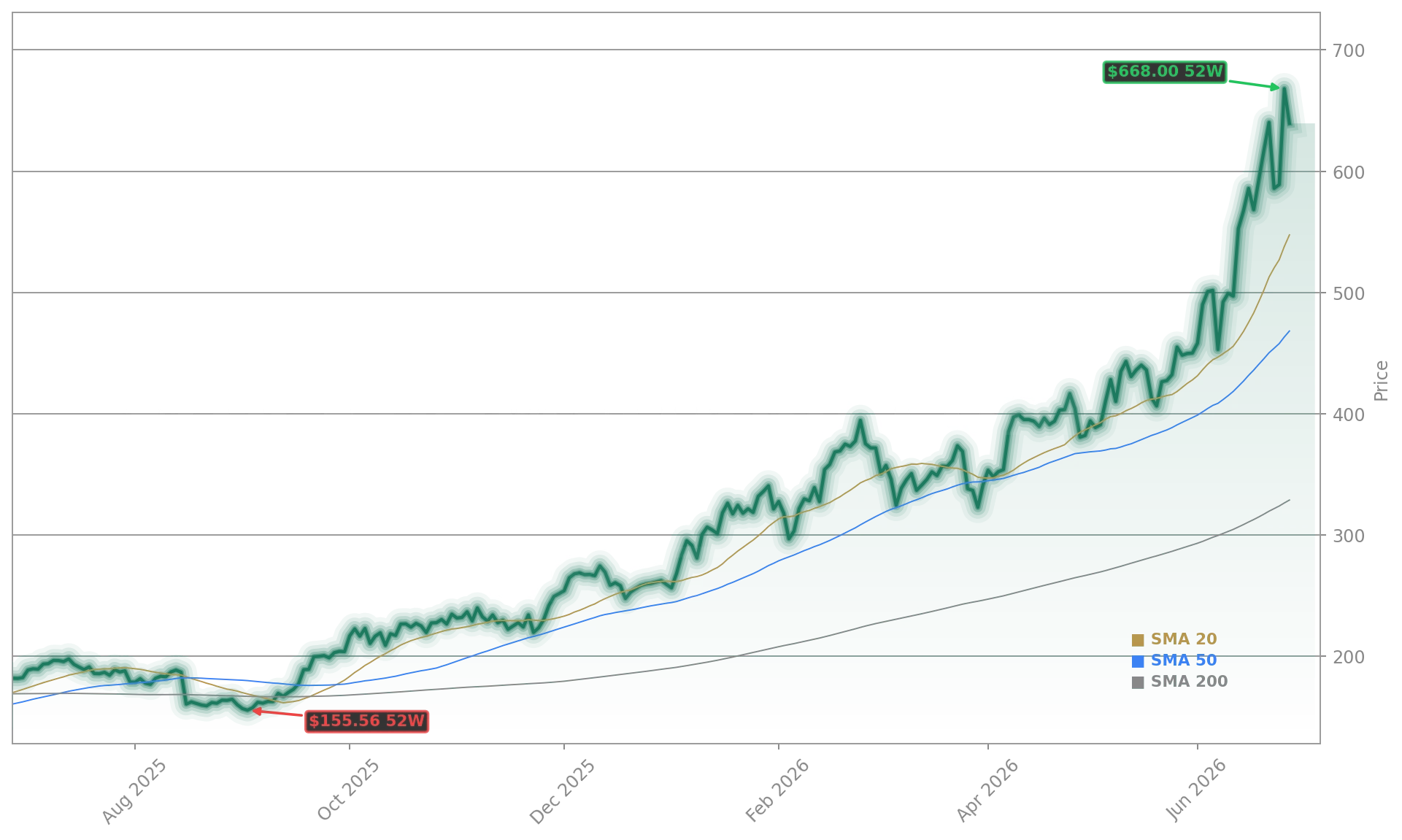

Applied Materials, Inc. spiked to $668.00 on Thursday — its highest close in history — after triggering a TradePulse ‘Power Inflow’ signal at $612.34 at 10:00 AM ET. This proprietary order flow indicator flagged a sharp, coordinated shift toward buying activity from both institutional and retail traders, propelling shares up 9.3% intraday. The momentum extended into Friday, with AMAT trading at $645.45 as of 2:22 PM CET — still up sharply on the week and outperforming the S&P 500 and NASDAQ, which posted modest losses. The move wasn’t isolated: memory and storage stocks rallied broadly after Micron’s strong earnings, reinforcing investor conviction in the AI-driven semiconductor capex cycle.

How do Applied Materials AI Systems solve the ‘memory wall’?

Applied Materials, Inc. unveiled a suite of new chipmaking systems designed explicitly to accelerate AI infrastructure deployment. These Applied Materials AI Systems include advanced epitaxy tools for DRAM transistor engineering, next-gen chemical mechanical planarization (CMP) and deposition systems for 3D stacking, and high-precision e-beam metrology for defect control in advanced packaging fabs. The goal is to boost memory bandwidth, improve power efficiency, and enable reliable hybrid bonding — directly addressing bottlenecks holding back generative AI model training and inference. Competitors like KLA and NVIDIA rely on these tools to scale their own AI hardware roadmaps, making Applied Materials, Inc. a critical, non-discretionary supplier in the AI supply chain.

Why are analysts raising targets — and by how much?

Wells Fargo upgraded its price target on Applied Materials, Inc. to $740 from $715, maintaining an Overweight rating and citing ‘increased confidence in the technology roadmap’ following recent investor events. Jefferies raised its target even more dramatically — to $770 from $510 — and reiterated its Buy rating, highlighting Applied Materials, Inc.’s ‘outperformer status’ and ‘strong exposure to leading-edge foundry and DRAM.’ Citigroup also boosted its target to $710, citing a ‘widening DRAM supply gap’ and AMAT’s expanding role in advanced packaging. Collectively, these upgrades reflect a consensus that Applied Materials AI Systems are not just incremental but foundational to next-generation AI chip economics.

How does AMAT compare to peers in the AI hardware race?

While Tesla and Apple build AI chips for internal use, and NVIDIA designs the most powerful accelerators, Applied Materials, Inc. builds the machines that make those chips possible. Its broad portfolio — spanning etch, deposition, metrology, and packaging — gives it wider exposure than narrower peers like KLA Corporation (KLAC), which focuses primarily on process control. A recent Globe and Mail analysis concluded Applied Materials, Inc. offers a more compelling risk-reward profile than KLAC, citing higher projected sales and EPS growth, stronger estimate trends, and a more attractive valuation multiple. That differentiation matters as AI capex shifts from logic-only to memory- and packaging-intensive workloads.

What’s the risk — and is the valuation sustainable?

Despite the bullish momentum, valuation concerns persist. GuruFocus estimates AMAT trades at 169.7% above its intrinsic value, with a forward P/E well above historical averages. Insider sales totaling $114.1 million have also raised eyebrows. Yet, unlike many AI-themed stocks, Applied Materials, Inc. delivered record financials in Q2 2026, with revenue and EPS far exceeding consensus — validating the strength of its execution. The company’s ability to scale supply and navigate China-related headwinds remains a watchpoint, per Yahoo Finance UK. Still, Trefis notes that while AMAT trades at a premium, its profitability and growth trajectory remain tightly linked to AI’s structural demand curve — not speculative sentiment.

Related Coverage: A recent analysis titled Applied Materials Forecast -9%: Plunge Despite $720 Targets questions whether the stock can sustain its rally after a sharp pullback, even as Wall Street targets climb. Meanwhile, onsemi Acquisition -19%: Synaptics Deal Sparks Selloff highlights how investor sentiment is shifting toward execution discipline — a contrast that underscores Applied Materials, Inc.’s credibility as a capital-efficient AI infrastructure partner.

Applied Materials, Inc. is delivering on its AI hardware promise with tangible, high-impact systems. For U.S. investors, this isn’t just a semiconductor equipment play — it’s a leveraged bet on the physical layer of AI’s next decade. The next quarterly earnings will confirm whether demand remains robust across foundry, DRAM, and advanced packaging segments. For long-term portfolios exposed to AI infrastructure, Applied Materials AI Systems represent a core, non-correlated growth pillar.