Is Applied Materials still buyable after a 7.4% jump, or is Citigroup’s $710 target only the start of a bigger AI-driven move?

Why Did Citigroup Raise AMAT’s Target?

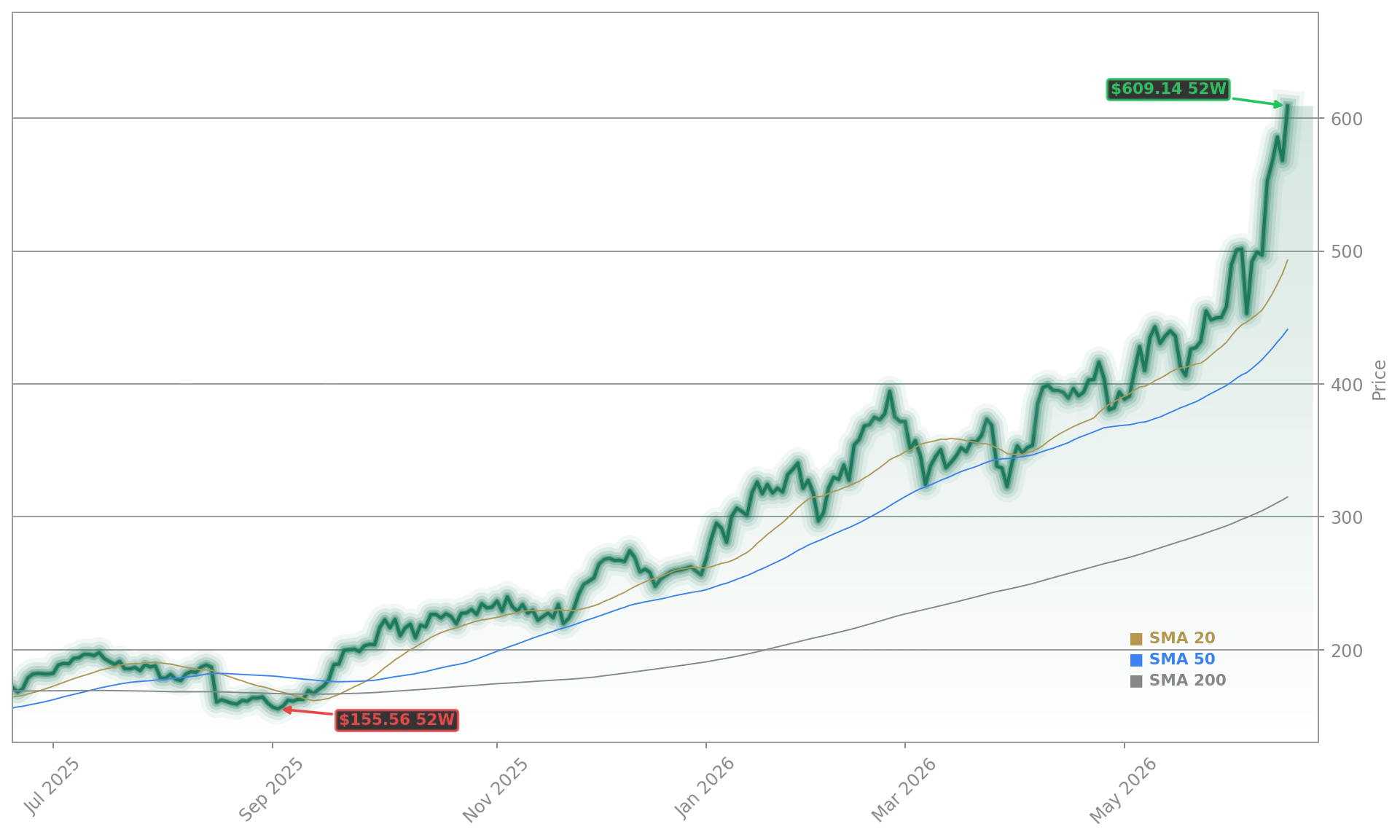

Citigroup analyst Atif Malik boosted Applied Materials, Inc.’s price target from $550 to $710—maintaining a Buy rating—and cited accelerating wafer fabrication equipment (WFE) demand as the core catalyst. Malik’s revised bull-case WFE sales forecast now stands at $145 billion for 2026, $200 billion for 2027, and $250 billion for 2028—up sharply from prior estimates. His note emphasized persistent capacity constraints, progress at Intel and Samsung foundries, and AI-driven logic and memory chip production ramping faster than expected. The upgrade coincided with AMAT’s intraday record high of $623.35—well above its 52-week high of $620.22—and reflects a broader Wall Street consensus: semiconductor equipment makers are no longer cyclical laggards but structural beneficiaries of the AI infrastructure buildout.

How Does AMAT Compare to Peers?

While Applied Materials, Inc. surged 7.4% to $610.34, peers followed closely: Lam Research jumped 4.2% to $385.88, hitting an all-time high of $397.54, and KLA rose 1.3% to $240.95—still below its $267.17 peak. ASML soared 6.1% to $1,921.94, eclipsing $1,938.49 earlier in the session. This synchronized strength underscores that the Applied Materials Forecast isn’t isolated—it’s part of a sector-wide re-rating. Notably, AMAT outperformed the NASDAQ Composite (up 1.8% today) and the Philadelphia Semiconductor Index (SOX), which gained 3.4%. Its 45.1% one-month return dwarfs NVIDIA’s 22.7% and Apple’s 9.3% over the same period—highlighting investor preference for semiconductor infrastructure over end-device players amid supply-chain tightness.

What’s Driving the Applied Materials Forecast?

The Applied Materials Forecast is being reshaped by three converging forces: AI chipset demand, CHIPS Act-funded domestic fab expansion, and long-term partnerships with innovators like Meta. A recent joint development with Luxottica tied to Ray-Ban Meta smart glasses underscores AMAT’s role beyond traditional logic and memory—extending into advanced packaging and heterogeneous integration. Q2 2026 revenue hit $7.91 billion, up 13% sequentially and 11% year-over-year—the highest quarterly figure in company history. Renaissance Investment Management’s Q1 Large Cap Growth Strategy identified AMAT as a top contributor, citing ‘broad-based growth across all segments’ and ‘favorable backdrop from federal stimulus and AI demand.’ With 138 hedge funds now holding AMAT—up from 111 in Q4—ownership breadth signals institutional conviction beyond momentum trading.

Is AMAT Overextended?

At $610.34, AMAT trades nearly 25% above its 20-day simple moving average—a technical signal some analysts flag as overextended. Yet fundamentals argue otherwise: gross margin expanded to 47.1%, operating margin hit 31.6%, and backlog rose to $14.2 billion—up 8% sequentially. While short-term pullbacks are possible, the structural drivers remain intact. Unlike cyclical downturns of the past, today’s WFE demand is anchored in AI, automotive, and national security priorities—not just consumer electronics. As Citigroup’s Malik noted, ‘continued capacity constraints’ through 2028 provide a multi-year runway—making near-term technicals less relevant for long-term investors. That context helps explain why AMAT’s valuation—trading at 32x forward EPS—still lags Tesla’s 48x and NVIDIA’s 61x despite superior earnings visibility.

What’s Next for Applied Materials Forecast?

Investors now await AMAT’s Q3 2026 guidance—expected in mid-July—and watch for confirmation of WFE spending acceleration across TSMC’s Arizona fab, Intel’s Ohio expansion, and Samsung’s Taylor, Texas site. Citigroup’s $710 target implies 16% upside from current levels, while consensus estimates project 14% EPS growth in fiscal 2026 and 12% in 2027. With the CHIPS Act allocating $39 billion directly to semiconductor manufacturing—and AMAT named as a key equipment partner—the Applied Materials Forecast remains tightly coupled to U.S. industrial policy execution. A breakout above $630 would confirm institutional accumulation ahead of earnings season—and further widen the gap between AMAT and traditional tech benchmarks.

We are more constructive on 2028 WFE given continued capacity constraints and expansion at both TSMC and memory makers, as well as recent progress at Intel and Samsung foundries.— Atif Malik, Citigroup

Related coverage includes Applied Materials Forecast +4.9% as UBS Lifts Target, which details Singapore capacity expansion and near-term margin leverage, and Broadcom AI Earnings +3.3% as Q2 AI Revenue Soars, highlighting how chip design leaders are fueling upstream equipment demand. Both reinforce that AI infrastructure is a multi-layered investment thesis—and AMAT sits at its most critical node.