Can Applied Materials Forecast momentum keep climbing after UBS raised its target and the stock broke to a fresh high?

Why Did UBS Raise Its Applied Materials Forecast?

UBS analyst Timothy Arcuri maintained a Buy rating on Applied Materials, Inc. and increased the price target from $515 to $570 on June 10 — a 10.7% upward adjustment. The move comes as AMAT’s Tampines, Singapore facility prepares for a $500 million expansion, aimed at scaling production of atomic layer deposition (ALD) and epitaxy systems critical for advanced logic and memory chips. Unlike cyclical equipment peers, AMAT’s exposure spans both logic (driven by NVIDIA’s Blackwell and Rubin architectures) and memory (supporting AI accelerators and HBM3 stacks), giving it structural leverage to the AI infrastructure wave. The upgrade signals growing conviction that AMAT’s 2026 revenue growth — now expected to exceed 22% year-over-year — is underpinned by multi-year capacity commitments from foundry and memory leaders, not just quarterly volatility.

How Does AMAT Compare to Semiconductor Peers?

While NVIDIA dominates AI chip headlines, Applied Materials, Inc. occupies the indispensable infrastructure layer — and its performance diverges meaningfully from peers. KLA Corporation, for instance, saw shares decline 3.2% last week amid softening inspection tool orders, while AMAT surged. Similarly, Broadcom’s recent earnings — though showing $22.2B in AI-related revenue — triggered a sharp 7% selloff due to margin pressure and guidance concerns. In contrast, AMAT’s Q2 2026 guidance implies gross margin expansion to 47.5%, supported by higher-margin advanced packaging and AI-optimized tool shipments. This resilience positions AMAT as a more predictable lever to AI capex than chip designers or legacy IDMs — especially as the S&P 500’s tech sector faces increasing scrutiny on valuation sustainability.

What Does the Singapore Expansion Mean for Wall Street?

The $500 million Singapore investment isn’t just about square footage — it’s a strategic bet on geopolitical diversification and AI supply chain localization. With U.S. export controls tightening on advanced chip tools and China’s domestic equipment push accelerating, AMAT’s Tampines hub now serves as a key node for ASE, UMC, and Samsung’s AI-adjacent logic and memory ramp. Analysts at Stifel and Wells Fargo have echoed UBS’s view: AMAT’s ability to deliver tools with sub-2nm readiness — combined with its Singapore-based service and calibration infrastructure — makes it irreplaceable for customers navigating export rule complexity. That operational moat directly supports the Applied Materials Forecast for 18–24-month order visibility, now running at 1.8x annualized revenue — well above the 1.3x average for semiconductor equipment peers.

Is AMAT’s Technical Strength Sustainable?

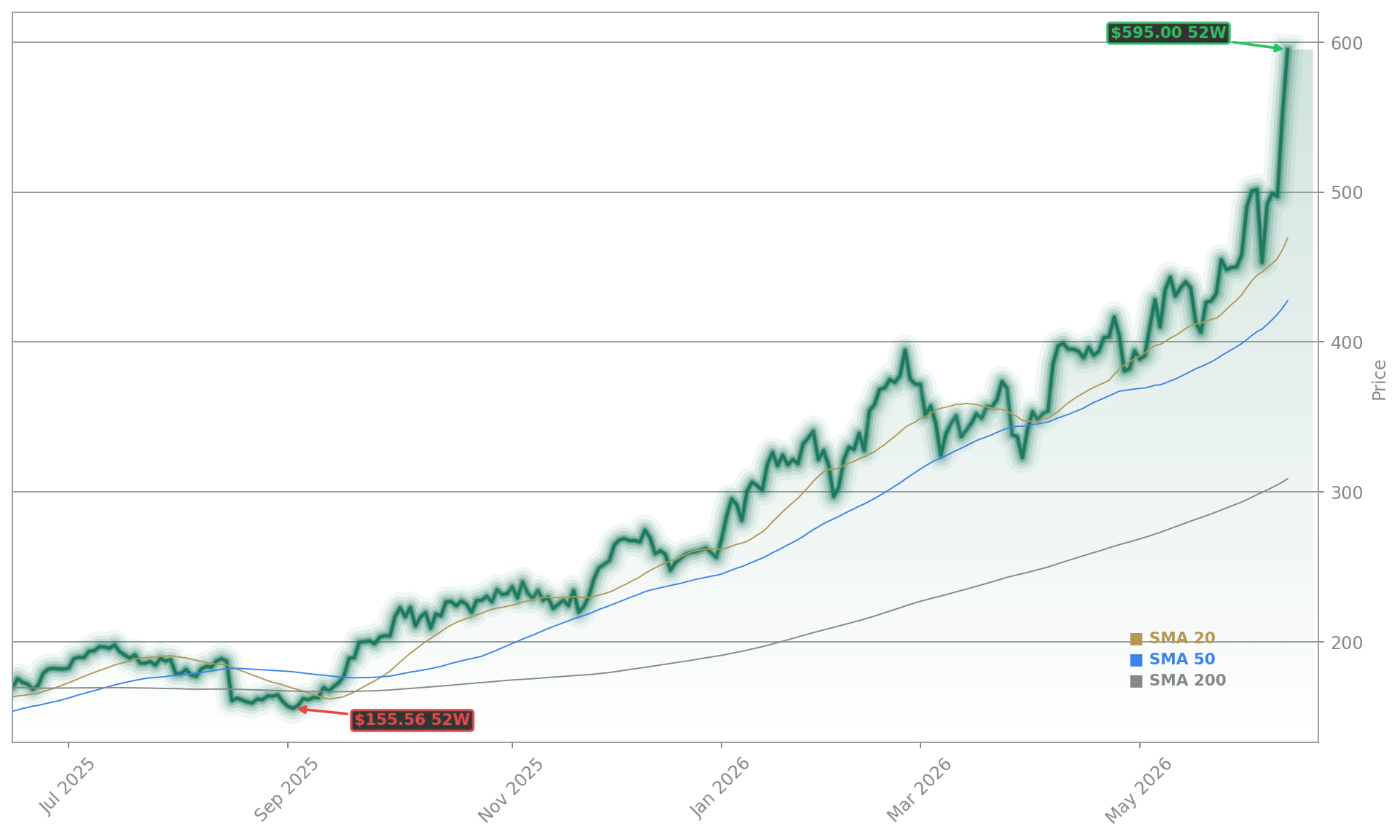

Technically, Applied Materials, Inc. is firing on all cylinders: up 4.89% to $595.00 on Monday, with after-hours trading holding near $571.00. The stock cleared its 52-week high of $589.25 earlier in the session — a level it hadn’t breached since April 2025 — and now trades 27% above its 200-day moving average. RSI remains in bullish territory at 62.1, and MACD shows accelerating positive momentum. Support now sits at $558 (near-term) and $467 (long-term), levels that align with institutional accumulation patterns identified in recent options flow. Unlike many tech names trading near stretched valuations, AMAT’s forward P/E of 28.4 remains below the NASDAQ-100 average of 31.2 — suggesting room for further multiple expansion if the Applied Materials Forecast for AI-driven tool demand holds.

What’s Next for Applied Materials Forecast and Investors?

With Q2 2026 earnings due July 16, the market’s focus shifts to order intake for 3nm and GAA transistor tools — particularly for mobile AI SoCs and AI inference chips. UBS expects AMAT to report $7.12 in EPS and $7.2B in revenue, both above consensus. Meanwhile, Wedbush’s Matt Bryson — who recently initiated coverage on Cerebras Systems with an Outperform rating — noted in a June 12 internal note that ‘AMAT’s Singapore capacity is becoming the de facto bottleneck for AI chip ramp timelines.’ That commentary underscores how tightly AMAT’s execution now links to broader AI infrastructure delivery. The Applied Materials Forecast is no longer just about equipment cycles — it’s about AI’s physical infrastructure velocity.

Applied Materials’ Singapore expansion is becoming the de facto bottleneck for AI chip ramp timelines.— Matt Bryson, Wedbush

Related Coverage: For deeper insight into how AMAT’s Singapore expansion is reshaping its competitive positioning, see Applied Materials Singapore Expansion Drives AMAT +4.7%. Investors also need context on how AI revenue growth doesn’t always translate to stock gains — as demonstrated by Broadcom Earnings at $22.2B: Record AI Revenue, Stock Tanks.