Can Qualcomm Data Center really become the company’s next growth engine as handset weakness collides with a new AI infrastructure push?

What’s Driving Qualcomm’s Data Center Breakthrough?

Qualcomm Incorporated’s entry into the data center is no longer aspirational—it’s contractual. CEO Cristiano Amon confirmed on the Q2 FY26 earnings call that a leading hyperscaler has signed on for custom AI silicon, with initial shipments slated for late 2026. This isn’t a reference design or sampling phase; it’s volume ramp timing. The chip leverages Alphawave Semi’s high-speed interconnect IP and integrates RISC-V-based AI accelerators—technology Qualcomm is now actively evaluating via advanced acquisition talks with Tenstorrent. Citigroup analysts upgraded QCOM to ‘Buy’ with a $265 price target, citing ‘a credible, capital-light path to $3B+ data center revenue by FY2029.’ That would represent nearly 7% of total FY2025 revenue ($44.3B), but more importantly, it diversifies away from handset volatility—especially as Chinese OEM demand softens.

How Does Qualcomm Data Center Compare to Intel and Nvidia?

While Intel struggles to monetize its foundry ambitions and NVIDIA dominates training with massive GPU clusters, Qualcomm Incorporated is targeting inference, AI agents, and real-time edge-to-cloud orchestration—markets growing at 34% CAGR through 2029 (per Morgan Stanley). Unlike Intel’s 114.2x forward P/E, Qualcomm trades at just 21.8x—below the XLK sector benchmark of 28.7x. Its 5.1x P/S ratio also sits well under Intel’s 12.5x and even Broadcom’s 8.2x. RBC Capital Markets notes that ‘Qualcomm’s data center margin profile, anchored by royalty-like IP licensing and fabless execution, could sustain 60%+ gross margins—well above traditional CPU vendors.’ That structural advantage is why QCOM’s free cash flow yield holds at 5.68%, even as it invests $1.2B in AI silicon R&D this fiscal year.

Why Are AR and Wearables Now Core to the Data Center Strategy?

Qualcomm’s Snapdragon Reality Elite platform—unveiled at the Augmented World Expo—delivers 48 TOPS of on-device AI compute with industry-leading thermal efficiency. It’s not a standalone play: it’s the client-side counterpart to the Qualcomm Data Center stack. When AI agents run inference in the cloud (via the new hyperscaler chip), they need low-latency, secure endpoints—exactly what AR glasses and AI wearables deliver. The Snapdragon START developer program bundles hardware modules, AI frameworks, and cloud orchestration tools, effectively creating a vertically integrated AI stack. This mirrors Apple’s strategy but with broader OEM access—and positions Qualcomm as infrastructure for Meta’s next-gen AR roadmap and Microsoft’s Copilot+ devices.

Is the Valuation Still Justified Amid Handset Weakness?

Yes—but with caveats. Q2 FY26 handset revenue fell 13% YoY to $6.02B, reflecting Chinese OEM softness and memory constraints. Yet Automotive revenue hit a record $1.33B (+38% YoY) and IoT reached $1.73B (+9%). Combined, Automotive + IoT grew 20% YoY—outpacing total company growth. With $12.8B in FY2025 free cash flow, a 0.8x debt-to-equity ratio, and a newly authorized $20B buyback (of which $5.4B has already been deployed), Qualcomm Incorporated is funding its transformation without leverage risk. Goldman Sachs highlights that ‘non-Apple QCT revenue grew 18% YoY in FY2025—proof that diversification is operational, not just rhetorical.’

What Catalysts Are Next for Qualcomm Data Center?

The rise of AI agents is reshaping our roadmap across every platform we develop—and our entry into the data center, where a leading hyperscaler custom silicon engagement is on track for initial shipments later this calendar year.— Cristiano Amon, CEO of Qualcomm Incorporated

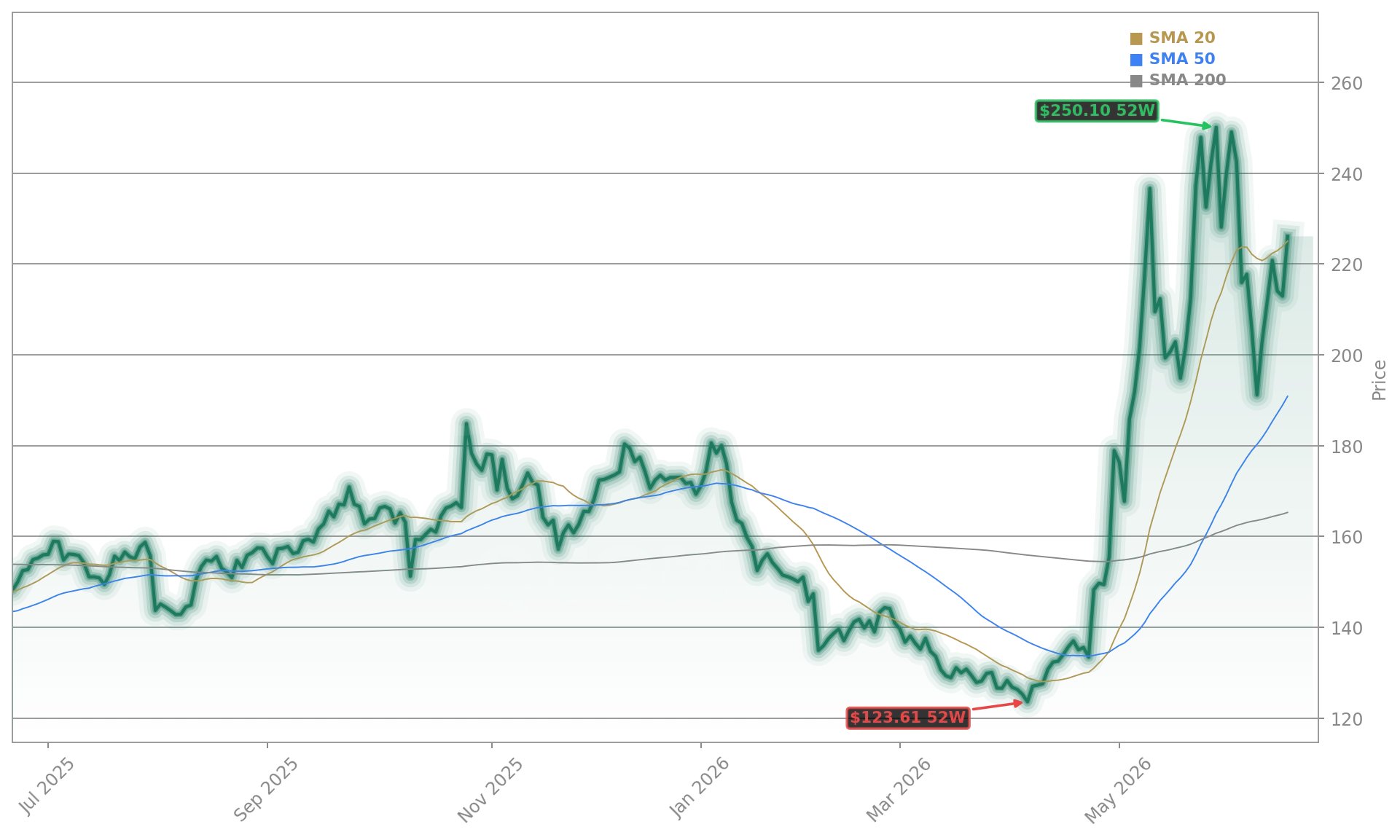

The June 24, 2026 Investor Day is the critical near-term catalyst. Qualcomm Incorporated will detail its Physical AI roadmap—including full specifications for its first data center SoC, power efficiency benchmarks versus AMD MI300X, and commercial timelines for Tenstorrent integration. Bloomberg reports the chip is already undergoing validation at two Tier-1 cloud providers. With 30-day volatility spiking above 90%, the market is pricing for binary outcomes. But for long-term investors, the convergence of data center silicon, AR endpoints, and AI wearables creates a defensible moat—one that neither Tesla nor traditional chipmakers currently replicate.