Can Rivian’s billion-dollar capital raise strengthen its EV future, or will dilution fears keep crushing the stock?

What’s Driving the Rivian Stock Offering?

Rivian Automotive, Inc. launched its Rivian Stock Offering after market close on Monday, July 6, 2026, filing an 8-K with the SEC to disclose both the equity raise and preliminary Q2 financials. The offering targets up to 75 million newly issued shares — all sold by the company — with underwriters granted a 30-day option for an additional 11.25 million. While the offering price remains undisclosed, at current levels, the deal could raise over $1.2 billion before expenses. Proceeds will fund general corporate purposes, including equity contributions under its Amended and Restated Loan Arrangement with the U.S. Department of Energy — a critical lifeline for capital-intensive EV ramp-ups. This move comes as Rivian’s cash position climbs to an estimated $5.3 billion as of June 30, up from $4.8 billion at quarter-end March, suggesting strategic capital optimization rather than distress financing.

How Does Q2 Revenue Stack Up Against Peers?

Rivian Automotive, Inc. expects Q2 2026 revenue of $1.55 billion to $1.65 billion — a 19% to 27% year-over-year increase versus $1.30 billion in Q2 2025. That range beats the $1.46 billion FactSet consensus, underscoring accelerating execution. However, growth is tempered by a 12%–15% decline in average selling price, driven by a higher mix of commercial delivery vans — lower-margin but strategically vital for Amazon and other fleet partners. For comparison, Tesla reported Q2 2026 vehicle revenue of $14.2 billion with 442,000 deliveries, while NVIDIA’s data center revenue surged 215% year-over-year. Rivian’s software and electrical architecture services — now contributing meaningfully to revenue — align it more closely with tech-integrated auto peers than legacy OEMs. Morgan Stanley analysts recently upgraded the sector outlook, citing ‘software monetization inflection points’ across EV startups, though they maintained an ‘Underweight’ rating on Rivian pending margin clarity.

Why Did the Stock Drop Despite Revenue Upside?

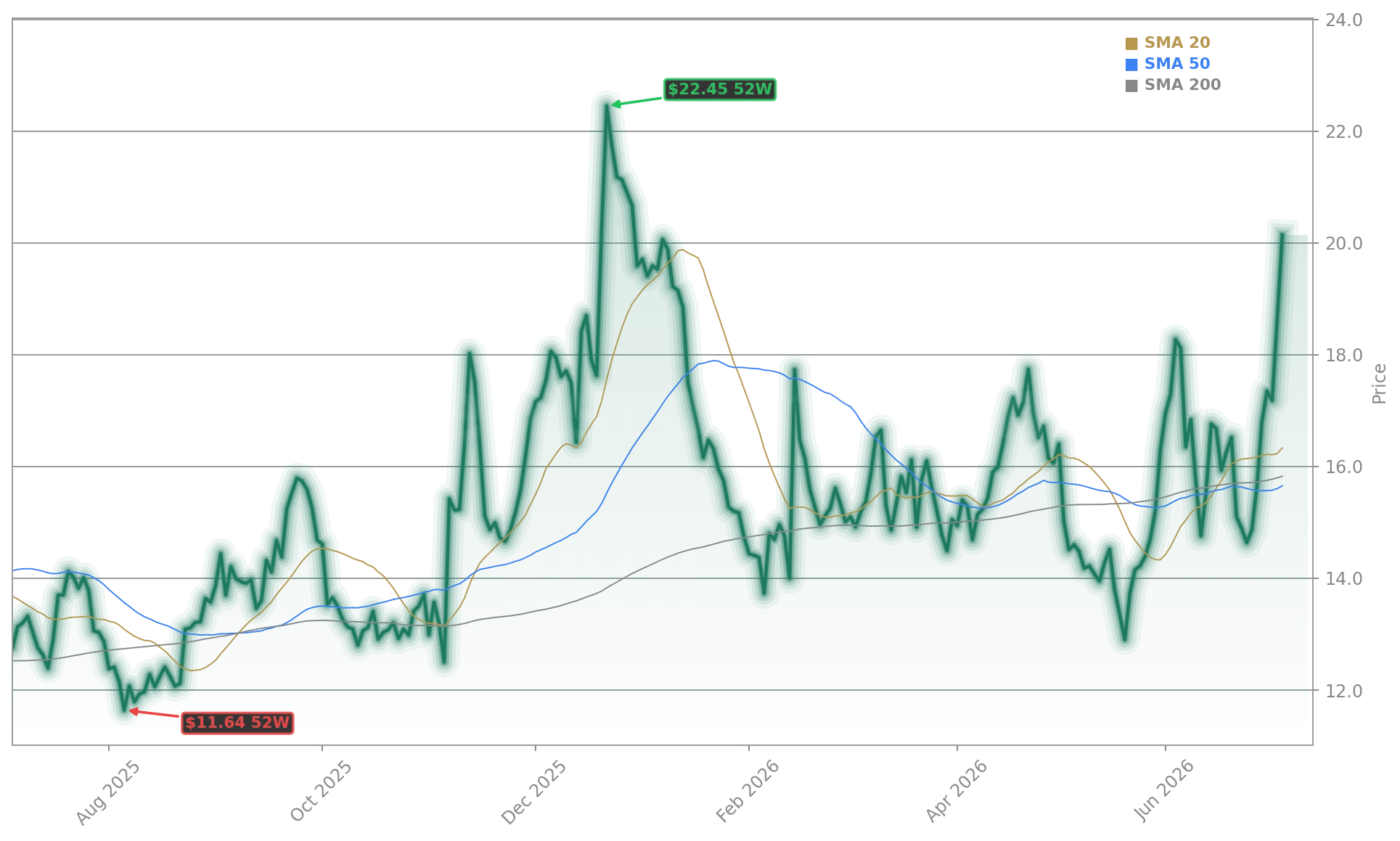

RIVN shares plunged 8.9% to $18.34 in after-hours trading — erasing 2026’s 2.2% year-to-date gain — as investors weighed dilution risk against operational progress. The Rivian Stock Offering represents ~11% potential share count expansion at the top end, a material dilution for a company still burning cash. Though Q2 deliveries rose 14% quarter-over-quarter — powered by R1 consumer SUVs, Amazon van deployments, and the early R2 crossover rollout — gross margins remain under pressure. Citigroup analysts noted in a July 5 report that ‘Rivian’s path to positive EBITDA hinges on R2 scale and software gross margin expansion beyond 65% — neither of which is fully priced in.’ The stock’s volatility reflects Wall Street’s broader skepticism toward pre-profitability EV names, especially as the S&P 500’s energy and auto sectors trade at 14x and 8x forward P/E, respectively.

What Does This Mean for the NASDAQ and EV Sector?

The Rivian Stock Offering arrives amid mounting sector scrutiny: Lucid Motors (LCID) sank 7.8% last week after missing delivery targets and replacing its CFO, while Apple’s long-rumored autonomous vehicle project remains in stealth — a reminder that hardware-software integration remains high-risk. Rivian’s $5.3 billion cash cushion provides runway into 2027, but its Q2 gross margin is expected to remain negative — unlike Tesla, which reported 18.3% vehicle gross margin in Q2. RBC Capital Markets downgraded Rivian to ‘Sector Perform’ on June 28, citing ‘unresolved capital intensity and competitive pressure from Ford’s E-Transit and GM’s BrightDrop.’ With the NASDAQ up 12% year-to-date but EV stocks lagging by 23%, Rivian’s offering may test investor appetite for growth-at-all-costs models in a rising-rate environment.

What’s Next for Rivian Automotive, Inc.?

Investors now await the official Q2 earnings release, expected July 30, 2026, which will confirm delivery volumes, gross margin, and R2 production ramp. The Rivian Stock Offering’s success will hinge on pricing discipline and investor confidence in the R2’s $45,000 price point — a key battleground against Tesla’s upcoming $25,000 model. With commercial van orders from Amazon locked through 2028 and new software contracts with Tier 1 suppliers, Rivian’s path forward balances scale, margin, and tech differentiation. The next catalyst is likely the Q3 production update — due August 20 — which will signal whether R2 volume can offset van mix headwinds and stabilize margins.

Related Coverage: Rivian’s delivery momentum is gaining real traction — Rivian Deliveries Jump 14% as R2 Launch Lifts Outlook. Meanwhile, sector-wide pressure is mounting: Lucid CFO Change -7.8% as Delivery Miss Hits the Stock highlights how quickly execution risks can derail EV valuations.

Rivian’s path to positive EBITDA hinges on R2 scale and software gross margin expansion beyond 65% — neither of which is fully priced in.— Citigroup analysts

Rivian Stock Offering signals both ambition and urgency as Rivian Automotive, Inc. scales toward profitability. For U.S. investors, it represents a high-conviction bet on EV software integration — but one requiring close monitoring of margin trajectory and R2 execution. The next quarterly earnings will determine whether this capital raise fuels acceleration or deepens skepticism. For long-term investors, disciplined entry points near $18–$20 could offer asymmetric upside if R2 production hits 10,000 units per quarter by Q4.