Are Robinhood Earnings still a growth story or is the crypto slump exposing just how fragile this fintech rally really is?

How are Robinhood Earnings moving the stock?

Robinhood Markets, Inc. (HOOD) last reported quarterly results with net revenue of about $1.07 billion, up 15% year over year, and adjusted earnings per share of $0.38. Net income rose roughly 3% to $346 million, marking another profitable quarter. However, consensus on Wall Street had been closer to $1.14 billion in revenue and $0.39 EPS, so the miss on both the top and bottom line immediately weighed on sentiment.

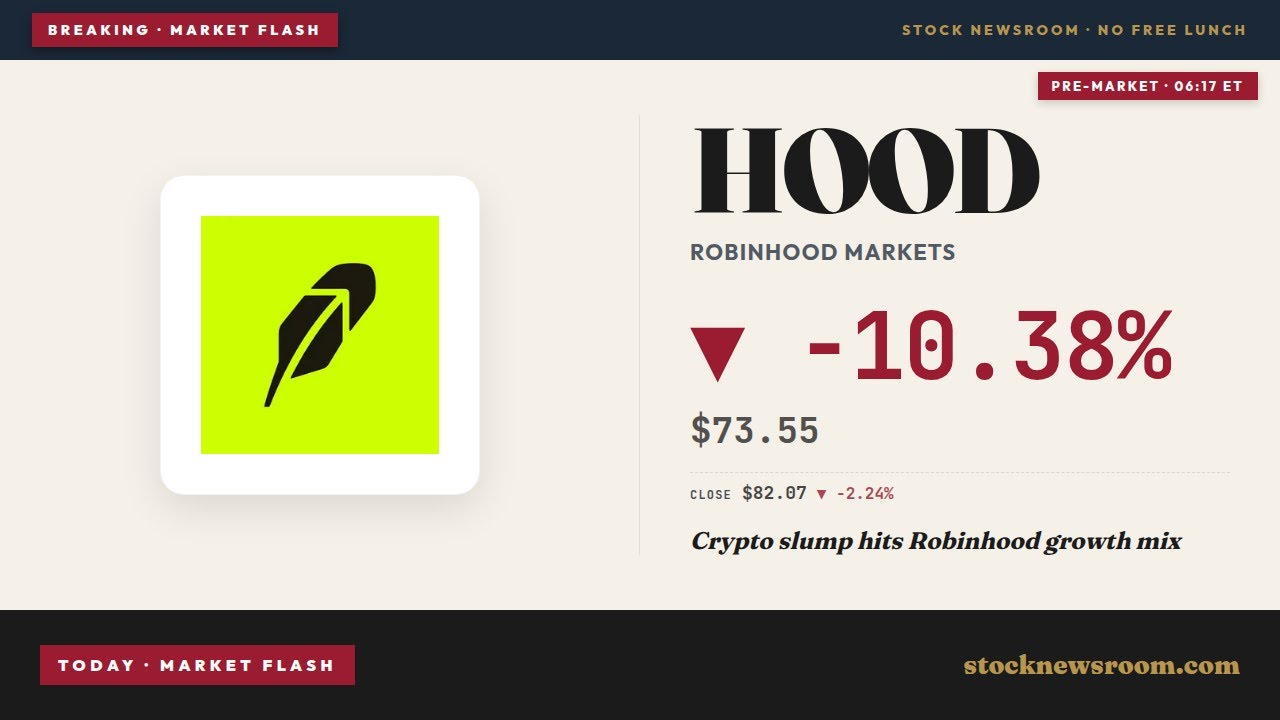

HOOD closed the prior day at $74.41 and recently traded around $82.07 before the earnings reaction. In early U.S. pre‑market action today, the stock is indicated at $73.60, down about 10.3%, erasing a chunk of its recent rally and reflecting disappointment with Robinhood Earnings and the underlying trading mix. While the stock is still well off its 52‑week lows, the setback reminds investors how quickly growth expectations can reset when a high‑beta fintech misses the mark.

On a year‑to‑date basis, HOOD shares had already faced volatility amid changing risk appetite in the NASDAQ and increasing regulatory scrutiny of event contracts and crypto products. The latest quarter adds fundamental pressure to that backdrop, even as some analysts continue to frame the pullback as a potential opportunity for long‑term buyers.

What hurt Robinhood Earnings under the hood?

The primary issue in the latest Robinhood Earnings update was a steep downturn in cryptocurrency activity. Crypto trading revenue dropped about 47% year over year to roughly $134 million, as months of weaker Bitcoin and alt‑coin prices cooled retail speculation. That shortfall more than offset modest strength in equities and options and directly contributed to the revenue miss versus Wall Street expectations.

Transaction‑based revenues overall were up about 6% from a year ago but declined roughly 20% versus the previous quarter, underscoring how sensitive the business remains to short‑term trading intensity. Critics such as wealth manager Ross Gerber argue the company still behaves too much like a “gambling app,” heavily reliant on customers trading speculative options, crypto and prediction contracts rather than building long‑term portfolios.

Management, led by CEO Vlad Tenev, is trying to shift that narrative. Tenev emphasized that crypto’s long‑term value lies in infrastructure and tokenization rather than price spikes, signaling continued investment into blockchain rails even through the current downturn. Still, in the near term, a weaker crypto cycle has clearly exposed the leverage in Robinhood’s earnings profile.

Are Gold, banking and prediction markets offsetting the pain?

Despite the headline miss, several business lines are quietly transforming the company. Paid subscription product Robinhood Gold reached a record 4.3 million subscribers, up 36% year over year, with subscription revenue climbing about 32% to $50 million. Attach rates are rising as well: around 16% of the overall customer base and roughly 40% of new customers now take Gold, giving the company a high‑margin, recurring revenue pillar that is far less cyclical than trading.

Robinhood’s new banking offering has also scaled quickly. Management reported more than $2 billion in net deposits and about 125,000 funded customers, with an impressive 40% of those customers using the product for direct deposit. That suggests users are starting to treat Robinhood as a primary banking relationship rather than just a speculative trading app, which could support deeper wallet share over time.

The breakout star of the quarter was the company’s “other” trading category, largely driven by event contracts and prediction markets. Revenue in this bucket surged roughly 320% year over year to about $147 million, with prediction market volumes on track for approximately $3 billion in April, which would mark the second‑highest month since launch. These products are controversial from a regulatory standpoint, but they demonstrate Robinhood’s ability to monetize retail interest around sports, politics and macro events in a way traditional brokers like Charles Schwab or Fidelity currently do not.

Beyond the U.S., the company is making measured progress in international expansion, including nearly 1 million funded customers abroad, crypto plans for Canada and in‑principle approval in Singapore. That positions Robinhood competitively against diversified platforms like NVIDIA’s favored trading partners in AI‑themed baskets and full‑service brokers courting global flow.

What does higher spending and Trump Accounts mean?

Another key piece of the Robinhood Earnings story is spending. Adjusted operating expenses plus stock‑based compensation came in at about $607 million and included roughly $14 million of incremental costs tied to the new Trump Accounts program and the Rothera prediction‑market exchange. Management raised full‑year adjusted OpEx and SBC guidance to a range of $2.7 billion to $2.825 billion, reflecting an additional $100 million investment this year, about half of it expected in Q2.

Trump Accounts represent a potentially transformative contract: more than 5.5 million U.S. children are already enrolled, with over 60 million eligible, and Robinhood is positioned as sole broker and trustee under the direction of the U.S. Treasury, alongside BNY Mellon as financial agent. The structure is cost‑plus, meaning revenues are designed to exceed expenses over time, but investors will need to watch execution risk and near‑term margin pressure.

Even with heavier spending, Robinhood continues to prioritize capital returns. The board refreshed a $1.5 billion buyback authorization, and the company has already repurchased over $300 million of stock this year, or around 4 million shares. That contrasts with earlier years when dilution from equity compensation was a persistent concern and brings HOOD more in line with capital frameworks at mature fintech peers.

On the Street, opinions remain divided. Piper Sandler and Truist Financial both maintain Buy ratings with ambitious medium‑term price targets, while Louis Navellier recently downgraded Robinhood from Strong to Neutral in his Stock Grader framework. TradingKey notes some analysts see potential long‑run targets up to $425 by 2030 if Robinhood fully globalizes and successfully monetizes AI‑driven products, though such scenarios require flawless execution.

Related Coverage

Investors looking to connect the latest Robinhood Earnings with the company’s broader AI ambitions may want to review the recent analysis “Robinhood OpenAI Investment $75M Surge Shocks HOOD.” That piece explores whether Robinhood’s $75 million allocation to OpenAI via its ventures arm could turn its AI narrative into a tangible growth catalyst. You can read it here: Robinhood OpenAI Investment $75M Surge Shocks HOOD, which provides additional context on how AI tools such as Cortex and agentic AI initiatives might reshape the platform’s competitive edge against giants like Apple and Tesla in AI‑themed retail investing.

Price moves up and down, but what I can tell you is crypto as technology infrastructure is going to be big, and we’re investing.— Vlad Tenev, CEO of Robinhood Markets, Inc.

In sum, the latest Robinhood Earnings underline a company in transition: crypto weakness and higher expenses are clashing with rapid growth in Gold, banking and prediction markets. For U.S. investors, HOOD now hinges less on meme‑stock frenzies and more on whether these newer, stickier revenue streams can stabilize margins and smooth out trading cycles. The next earnings report will show whether Trump Accounts, international expansion and AI‑powered products can turn this volatile fintech into a more durable fixture of NASDAQ portfolios.