Can Rocket Lab Acquisition turn a launch company into a space infrastructure powerhouse faster than Wall Street can reprice it?

What Does the Rocket Lab Acquisition Mean for NASDAQ?

The $8 billion Rocket Lab Acquisition instantly elevates Rocket Lab USA, Inc. into the upper tier of space-sector market capitalization — and shifts investor focus from launch cadence to recurring service revenue. With Iridium’s $495 million OEBITDA and 57% margin in 2025, the combined entity gains a stable cash engine to fund Neutron development and next-gen direct-to-device (D2D) services. Unlike pure-play launchers such as Rocket Lab or SpaceX, the new Rocket Lab will generate revenue from spectrum licensing, IoT subscriptions, and government PNT contracts — a profile more aligned with telecom infrastructure than aerospace manufacturing. That’s why the stock surged 11.2% in pre-market trading — a reaction consistent with how Wall Street prices vertical integration in high-barrier sectors like semiconductors or cloud infrastructure.

How Does Iridium Compare to Competitors Like Starlink?

Iridium’s LEO network offers critical advantages over newer entrants: global L-band spectrum rights, 2.55 million active subscribers, and decades of safety-of-life certification across aviation, maritime, and defense. While Starlink focuses on broadband, Iridium delivers low-bandwidth, high-reliability, GPS-alternative positioning and messaging — capabilities the U.S. Department of Defense explicitly prioritizes in denied environments. That distinction matters: Morgan Stanley analysts recently upgraded Iridium to ‘Overweight’, citing its ‘irreplaceable spectrum moat’ and growing defense adoption of its NTN DirectSM service — a capability Rocket Lab now owns outright. For investors comparing Rocket Lab USA, Inc. to broader space ETFs or telecom infrastructure plays, this acquisition adds a rare blend of regulatory insulation and mission-critical demand.

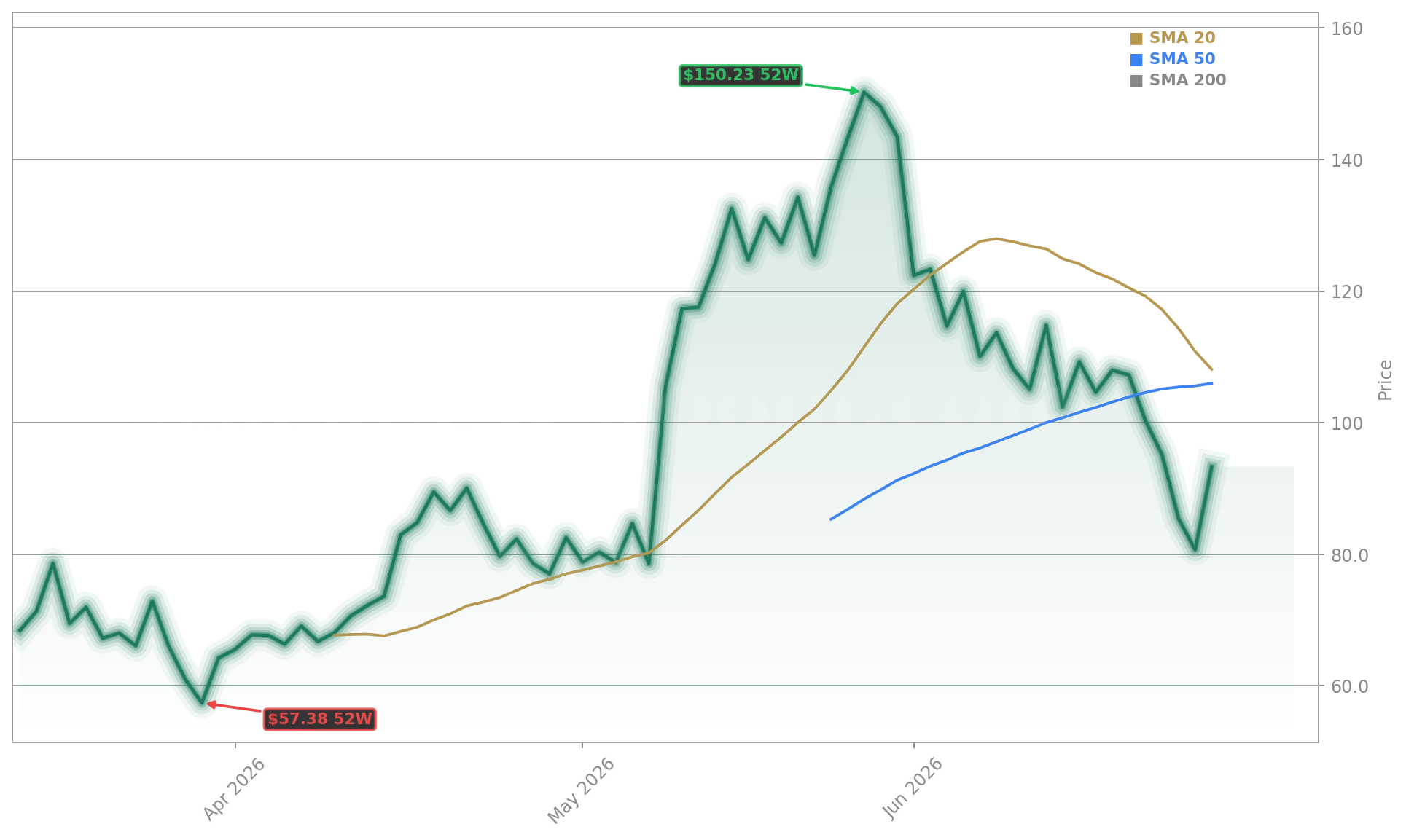

What’s the Financial Path to $150 Per Share?

With RKLB trading at $93.25 and analysts at 24/7 Wall St. projecting $150 by April 2027, the Rocket Lab Acquisition provides the catalyst — not just growth, but margin expansion. Rocket Lab eliminates third-party launch costs for Iridium constellation replenishment, capturing ~$250 million annually in internalized launch margin. Deutsche Bank and Wells Fargo have committed $3.6 billion in bridge financing, and the deal’s tax-free reorganization structure preserves capital efficiency. RBC Capital Markets notes the combined entity’s ‘path to $1.2 billion in annual recurring revenue by 2028’ — a figure that would place RKLB among the top 5% of NASDAQ-100 companies by recurring revenue concentration. Crucially, the $8 billion enterprise value implies just 9.2x 2025 EBITDA — a steep discount to peers like Apple or NVIDIA in adjacent infrastructure sectors.

Will Regulatory Approval Delay the Rocket Lab Acquisition?

This is a defining moment for the space industry and the start of a new era of strategic, accelerated growth for Rocket Lab and Iridium.— Sir Peter Beck, founder and CEO of Rocket Lab

The deal is expected to close in mid-2027, subject to Iridium shareholder approval, FCC consent for spectrum transfer, and Hart-Scott-Rodino antitrust clearance. Unlike mega-mergers in telecom or defense, this transaction faces limited overlap — Iridium operates in L-band narrowband; Rocket Lab has no existing telecom assets. The FCC’s recent approval of similar spectrum transfers (e.g., Ligado’s 2025 waiver) signals favorable precedent. Still, Citigroup highlights ‘the need for robust government engagement’ given Iridium’s role in U.S. national security PNT architecture — a factor that may accelerate, not hinder, approval. The ‘no-shop’ clause and board voting agreements further de-risk the timeline, with a hard deadline of December 28, 2027.