Why did Rocket Lab reach the Nasdaq-100 before SpaceX, and could forced ETF buying become RKLB’s next major catalyst?

Why Did Rocket Lab Beat SpaceX Into the Nasdaq-100?

Rocket Lab USA, Inc. entered the Nasdaq-100 on Monday, June 22 — weeks before SpaceX, despite the latter’s $2.22 trillion valuation and blockbuster IPO. Nasdaq’s recent rule changes fast-tracked mega-cap newcomers like SpaceX, but the exchange applied its existing eligibility criteria to Rocket Lab, an established public company with over three years of NASDAQ listing and consistent quarterly reporting. Unlike SpaceX, which must wait through the revised ‘seasoning period,’ Rocket Lab qualified immediately based on market cap, liquidity, and financial transparency. Its inclusion alongside Astera Labs, CoreWeave, Nebius Group, and Teradyne replaces Charter Communications, Cognizant, Insmed, Verisk Analytics, and Zscaler — signaling a tech-forward rebalancing aligned with AI infrastructure and national security themes.

What Does Rocket Lab Nasdaq-100 Inclusion Mean for Index Funds?

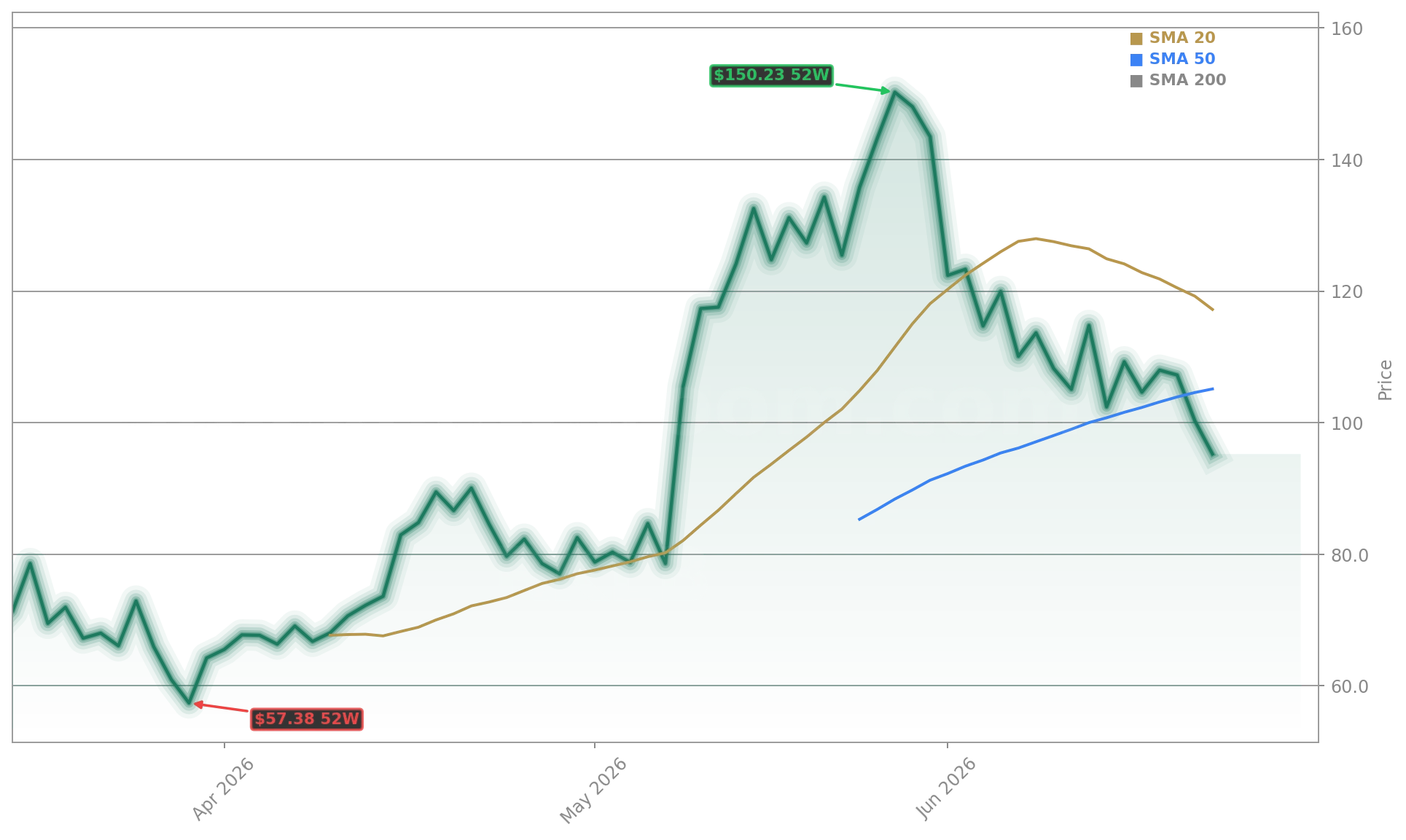

For investors holding passive exposure to the Nasdaq-100, Rocket Lab Nasdaq-100 Inclusion is non-negotiable: QQQ, Invesco’s $300+ billion flagship ETF, and hundreds of institutional index funds must now own RKLB shares. According to Nasdaq data, over $400 billion in assets track the index directly or indirectly. That creates sustained buying pressure — especially during the June 22–26 rebalancing window. While RKLB shares declined 8% on debut day amid broader space-sector weakness, analysts note this reflects short-term sentiment, not structural demand. KeyBanc Capital Markets upgraded Rocket Lab USA, Inc. to Overweight on June 15 with a $135 price target, calling it ‘the clear #2 to SpaceX.’ Stifel Nicolaus followed with a $132 target, while New Street Research set $150 — all citing the index inclusion as a near-term catalyst that anchors downside risk.

How Does Rocket Lab Compare to SpaceX and Other Space Stocks?

Rocket Lab USA, Inc. stands apart from SpaceX not just in valuation — trading at 91x sales versus SpaceX’s 130x — but in business model diversification. Over 50% of its Q1 2026 revenue came from its Space Systems segment, which builds satellites, flight software, solar arrays, and components for clients like the U.S. Space Development Agency and Raytheon. That contrasts sharply with SpaceX’s reliance on Falcon 9 launches and Starlink. Competitors like NVIDIA and Tesla dominate their respective infrastructure stacks, but Rocket Lab USA, Inc. is building the ‘pick-and-shovel’ layer of the space economy — a strategy that resonates with defense portfolios and infrastructure-focused ETFs. Its $190 million HASTE hypersonic defense contract and five-firm Neutron launch deal — the only reusable medium-lift rocket poised to challenge Falcon 9 — position it for margin expansion beyond launch services alone.

Is Rocket Lab USA, Inc. Positioned for Q2 2026 Growth?

This quarter has been phenomenal, the strongest Q1 in Rocket Lab’s history.— Peter Beck, CEO of Rocket Lab USA, Inc.

Yes — and the numbers confirm it. Q1 2026 delivered $200.3 million in revenue (up 63.5% YoY), $43.0% non-GAAP gross margin (up from 33.4%), and a $2.2 billion backlog (up 20.2% sequentially). Management guided Q2 revenue to $225–240 million. Crucially, Rocket Lab USA, Inc. booked 31 missions in Q1 — including 5 Neutron contracts — and launched the VICTUS HAZE mission in under 17 hours after notice, shattering the prior U.S. Space Force rapid-response record. With over $2 billion in liquidity and no near-term dilution risk, the company is scaling vertically via acquisitions: Mynaric for optical communications, Motiv Space Systems for Mars-proven robotics, and GA’s electric propulsion line. That execution contrasts with the uncertainty surrounding SpaceX’s $20 billion bond offering and its AI/data-center capital allocation — a concern flagged by Citigroup analysts as a potential headwind for space-sector liquidity.