Can Rocket Lab Nasdaq-100 status turn a space stock rally into a lasting institutional bid?

What Does Rocket Lab Nasdaq-100 Mean for Index Funds?

The June 22 inclusion of Rocket Lab USA, Inc. in the Nasdaq-100 Index triggers automatic buying by over $200 billion in index-tracking ETFs and mutual funds — including the Invesco QQQ Trust (QQQ). Unlike smaller-cap space names, RKLB now joins the ranks of Apple, NVIDIA, and Tesla in a benchmark that accounts for nearly 45% of the NASDAQ Composite’s total market cap. That structural demand shift comes as RKLB’s revenue mix pivots decisively: space systems now delivers over 65% of total revenue, dwarfing launch services — a critical evolution for long-term margin expansion and earnings visibility.

Is Rocket Lab USA, Inc. Still a Launch-Only Play?

No — and Wall Street is pricing it accordingly. While Electron remains the most-flown U.S. orbital rocket outside SpaceX, Rocket Lab USA, Inc. now derives over $420 million in annualized defense-related revenue, including $187 million under contract with the Space Development Agency’s Tracking Layer Tranche 3 program. Its Lightning satellite platform — built with in-house IR sensors, optical terminals, and StarLite space protection systems — directly competes with offerings from Lockheed Martin and Northrop Grumman in the $34 billion U.S. missile defense satellite market. That diversification has pushed RKLB’s backlog to a record $1.84 billion, up 41% year-over-year — a figure Citigroup highlighted in its May 2026 sector note as ‘unmatched among non-SpaceX launch providers.’

How Does Rocket Lab USA, Inc. Stack Up Against Peers?

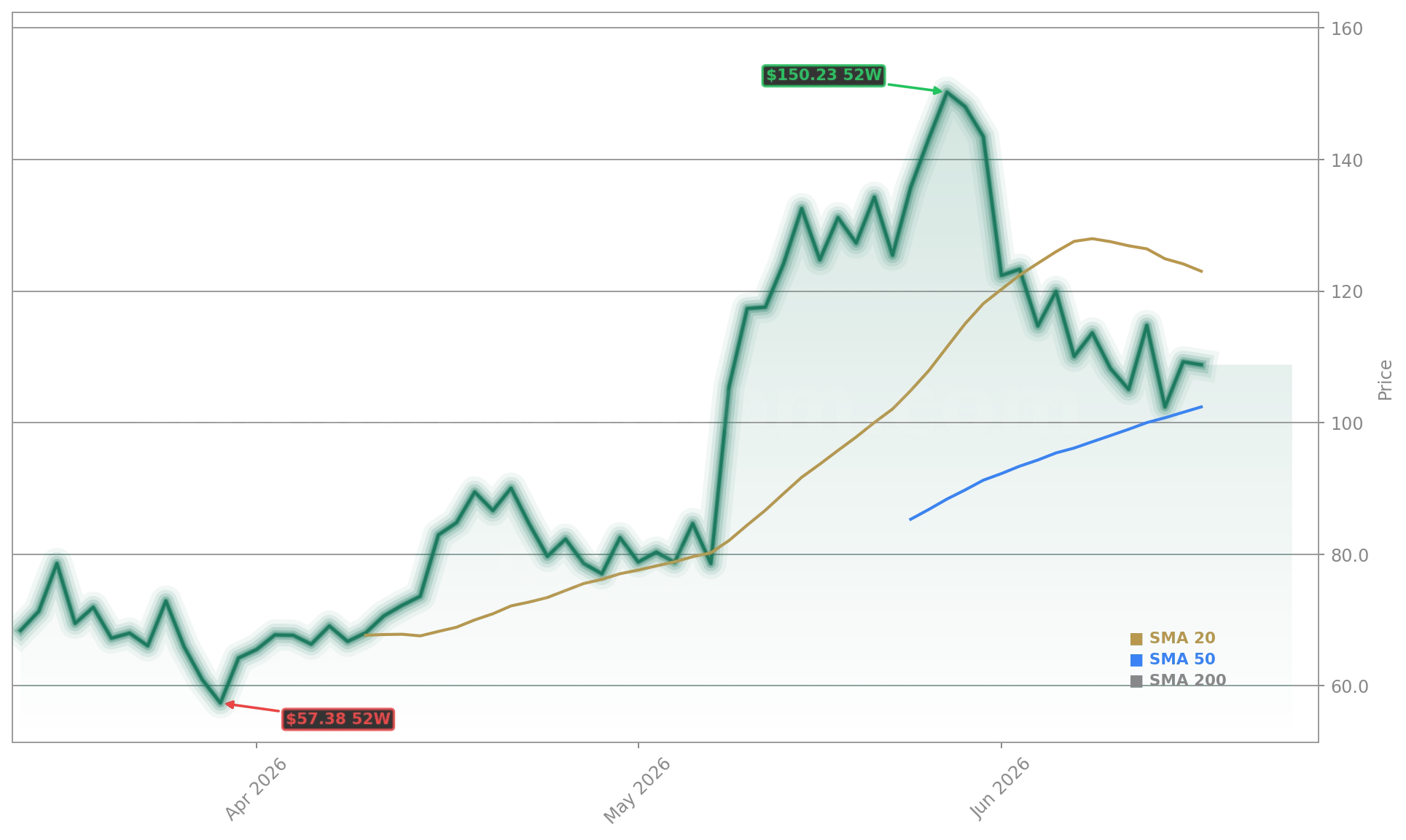

At 65x forward sales, RKLB trades at a steep premium — but one increasingly justified by execution. While Redwire (RDW) and Planet Labs (PL) struggle with margin compression and delayed Neutron alternatives, Rocket Lab USA, Inc. achieved 64% revenue growth in Q1 2026 and reported positive EBITDA for the first time in its history. Its Neutron medium-lift vehicle remains on track for 2027 inaugural flight, targeting national security and commercial mega-constellations — a segment where Tesla’s Starlink-aligned partners and Apple’s satellite connectivity ambitions are driving long-term capacity demand. RBC Capital Markets recently noted RKLB’s ‘infrastructure moat’ — vertical integration across propulsion, avionics, and spacecraft manufacturing — gives it a distinct edge versus peers reliant on third-party subsystems.

What’s Driving the $129 Price Target?

Clear Street analyst Greg Pendy raised RKLB’s price target to $129 from $98 on June 3, citing accelerating launch undersupply, Neutron’s growing pipeline, and ‘near-term path to GAAP profitability’ by Q4 2026. Pendy emphasized that Rocket Lab USA, Inc. is now generating $14.2 million in average revenue per launch — nearly triple the industry median — thanks to its end-to-end model. The firm also flagged HASTE, Rocket Lab’s hypersonic test platform, as a stealth defense growth vector: already under multi-year contract with the U.S. Air Force, it positions RKLB to capture spillover demand from the Pentagon’s $28 billion hypersonics R&D budget. With RKLB debt-free and holding $1.1 billion in cash, the balance sheet supports aggressive capital deployment without dilution — a rarity in the space sector.

Related Coverage

Rocket Lab’s a one-stop shop. It builds the rockets that fly to space and the satellites that operate once they get there.— Jim Cramer, CNBC’s Mad Money

For deeper analysis on execution risks, Rocket Lab Upgrade -3.7% as Neutron Hype Meets Reality examines whether Photon satellite delivery timelines and Neutron’s certification path remain on track. Meanwhile, Honeywell Spin-off: $4B M&A War Chest After Separation highlights how industrial conglomerates are reshaping defense and aerospace M&A — a trend that could accelerate strategic partnerships for Rocket Lab USA, Inc. as it scales its U.S.-based manufacturing footprint.