Can Rocket Lab’s $8 billion Iridium deal finally turn RKLB from a launch story into a durable space-and-defense powerhouse?

What Does the Rocket Lab Acquisition Mean for Wall Street?

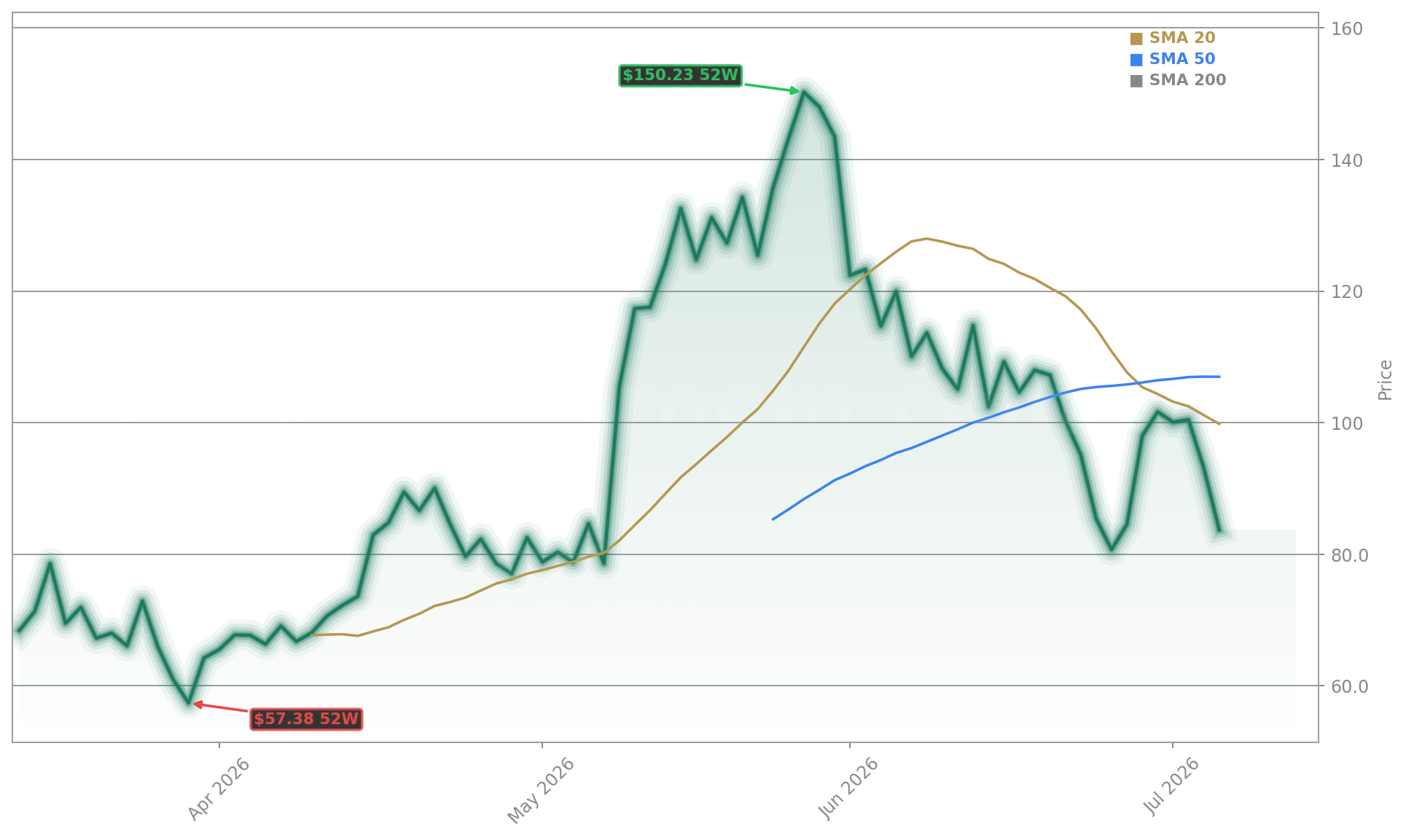

The $8 billion Rocket Lab Acquisition of Iridium Communications (IRDM) — announced June 29 and expected to close by mid-2027 — is a strategic inflection point. Unlike SpaceX’s Starlink-driven broadband model, Rocket Lab now controls launch, satellite manufacturing, L-band spectrum, and a global 66-satellite constellation with 2.5 million recurring subscribers. This end-to-end architecture mirrors defense-integrated models used by Boeing and Lockheed Martin — but at a fraction of the scale and with faster execution. Morgan Stanley’s $293 bull-case target hinges on three near-term catalysts: on-time Neutron debut, Iridium regulatory clearance, and Golden Dome program awards converting to signed contracts. With RKLB trading at $84.55 — 46% below its $151 52-week high — the valuation gap reflects skepticism around execution, not fundamentals.

How Does RKLB Stack Up Against Space Competitors?

Rocket Lab USA, Inc. remains a clear contrast to SpaceX: 35 launches in 2026 versus SpaceX’s 255, $602 million in annual revenue versus $18.7 billion, and a pure-play space focus versus SpaceX’s AI, xAI, and Starlink Mobile ambitions. Yet RKLB’s vertical integration — now accelerated by the Iridium deal, the $325 million Geost sensor acquisition, and Mynaric integration — delivers margins and visibility rare among NASDAQ-listed space names. Roth Capital Partners analyst Suji Desilva recently raised his price target to $130 from $100, maintaining a ‘Buy’ rating and citing Iridium’s high-margin recurring revenue as a key accretive driver. Bank of America Securities also reiterated a ‘Buy’ with a $115 target — underscoring broad institutional confidence beyond Morgan Stanley’s outlier case.

Is RKLB’s $2.20 Billion Backlog Enough to Sustain Growth?

Yes — and it’s arguably the strongest near-term catalyst. The $2.20 billion backlog includes 70+ contracted missions, the $816 million Space Development Agency (SDA) contract, and multiple U.S. Space Force awards — including the record-breaking VICTUS HAZE mission, completed 16 hours and 42 minutes ahead of schedule. That responsive launch capability — demonstrated in after-hours trading gains on July 7 — signals RKLB’s ability to win fast-turn defense contracts, a critical segment under the Pentagon’s Golden Dome initiative. While SpaceX dominates volume, RKLB’s niche in precision, responsive, and classified missions gives it pricing power and contract stickiness. Q1 FY26 revenue of $200.35 million — up 63.5% year over year — confirms execution is scaling. Institutional ownership stands at 71.78%, with QRG Capital Management increasing its stake by 84.2% in Q1 alone.

What’s Next for Neutron and Golden Dome?

Neutron’s debut — targeted before year-end 2026 — is the linchpin. At 13,000 kg to LEO, Neutron unlocks medium-lift contracts currently dominated by SpaceX’s Falcon 9, including Space Based Interceptor (SBI) components under Golden Dome. The $151 billion Golden Dome opportunity won’t convert to revenue overnight, but RKLB’s recent wins — including VICTUS HAZE and Synspective deployments — prove its ability to deliver full-stack solutions. The Iridium acquisition adds immediate cash flow: Iridium’s $1.6 billion annual revenue and 75%+ EBITDA margins provide a stabilizing foundation as Neutron ramps. Without the Rocket Lab Acquisition, RKLB would remain a high-beta launch play. With it, the company becomes a defense-anchored, cash-flow-aware growth story — a rare profile in the NASDAQ’s high-growth cohort.

Reaching $293 by year-end 2026 would require Neutron’s on-time debut, Iridium accretion, and major Golden Dome awards converting to signed dollars.— Morgan Stanley

Related Coverage: The recent Rocket Lab Share Sale -2.3%: 5M Shares Hit the Market has raised questions about insider sentiment, though the filing reflects converted preferred shares from the 2021 business combination — not new issuance. Meanwhile, analysts continue to weight the Iridium synergies heavily, with Morgan Stanley’s $293 target now widely cited as the most aggressive bull case on Wall Street. For investors seeking exposure to the $1.2 trillion global space economy — and not just AI or cloud infrastructure — the Rocket Lab Acquisition marks a decisive pivot toward durability.