Will the Rocket Lab Share Sale prove harmless profit-taking, or is the market signaling deeper doubts ahead of Neutron’s next milestone?

What Does the Rocket Lab Share Sale Mean for Investors?

Equatorial Trust’s registration of 5 million restricted shares—representing roughly 1.4% of Rocket Lab USA, Inc.’s current float—marks the largest single Form 144 filing for the company since Q4 2025. While the shares may be sold at any point over the next 90 days, timing coincides with multiple inflection points: Neutron’s final pre-flight certification review by the FAA is scheduled for mid-July, and integration planning for the Iridium acquisition has accelerated across engineering, spectrum, and ground-station teams. Unlike typical secondary offerings, this Rocket Lab Share Sale stems from pre-existing holdings, suggesting no immediate dilution—but heightened scrutiny on insider sentiment. For NASDAQ-traded space equities, this development arrives as NVIDIA’s AI-driven satellite data processing demand surges and Tesla’s Starlink-dependent vehicle autonomy roadmap deepens reliance on resilient LEO infrastructure.

How Does Neutron Change Rocket Lab’s Competitive Position?

Neutron isn’t just Rocket Lab USA, Inc.’s next rocket—it’s its strategic pivot from small-sat launch provider to full-stack space infrastructure operator. Standing 136 feet tall and capable of lifting 13,000 kg to low Earth orbit, Neutron directly challenges Apple-backed SpaceX’s Falcon 9 dominance in the mid-lift segment. With 70 missions already booked—including U.S. Space Force, ESA, and commercial constellation contracts—Neutron’s revenue runway exceeds $4.2 billion through 2029, per Morgan Stanley’s June 2026 update. Crucially, Neutron’s reusable first stage and rapid reusability cadence (target: 10 launches per vehicle per year) aim to slash per-launch costs by 65% versus Electron. That cost advantage positions Rocket Lab USA, Inc. not just as a competitor, but as a potential anchor tenant for U.S. government’s new National Space Transportation Policy, which prioritizes domestic, resilient launch capacity.

Why Did Rocket Lab USA, Inc. Acquire Iridium?

The $8 billion Iridium acquisition transforms Rocket Lab USA, Inc. from a launch services company into a vertically integrated space platform—mirroring how SpaceX leveraged Starlink to fund Starship development. Iridium’s 66-satellite constellation, serving 2.55 million government and commercial users across aviation, maritime, and defense, delivers stable $871 million in annual revenue and 82% gross margins. When combined with Rocket Lab’s in-house satellite manufacturing (Photon platform) and upcoming Neutron launch capacity, the merged entity gains end-to-end control over design, build, launch, and operations—cutting customer time-to-orbit from 24 months to under 9. Citigroup analysts note the deal “de-risks revenue visibility” and lifts 2026 consolidated revenue estimates to $1.78 billion, up from $914 million pre-acquisition. That scale now places Rocket Lab USA, Inc. within striking distance of major defense contractors on contract size—and within valuation range of mid-cap aerospace peers like L3Harris (LHX) and Northrop Grumman (NOC).

Is Rocket Lab USA, Inc.’s Valuation Justified?

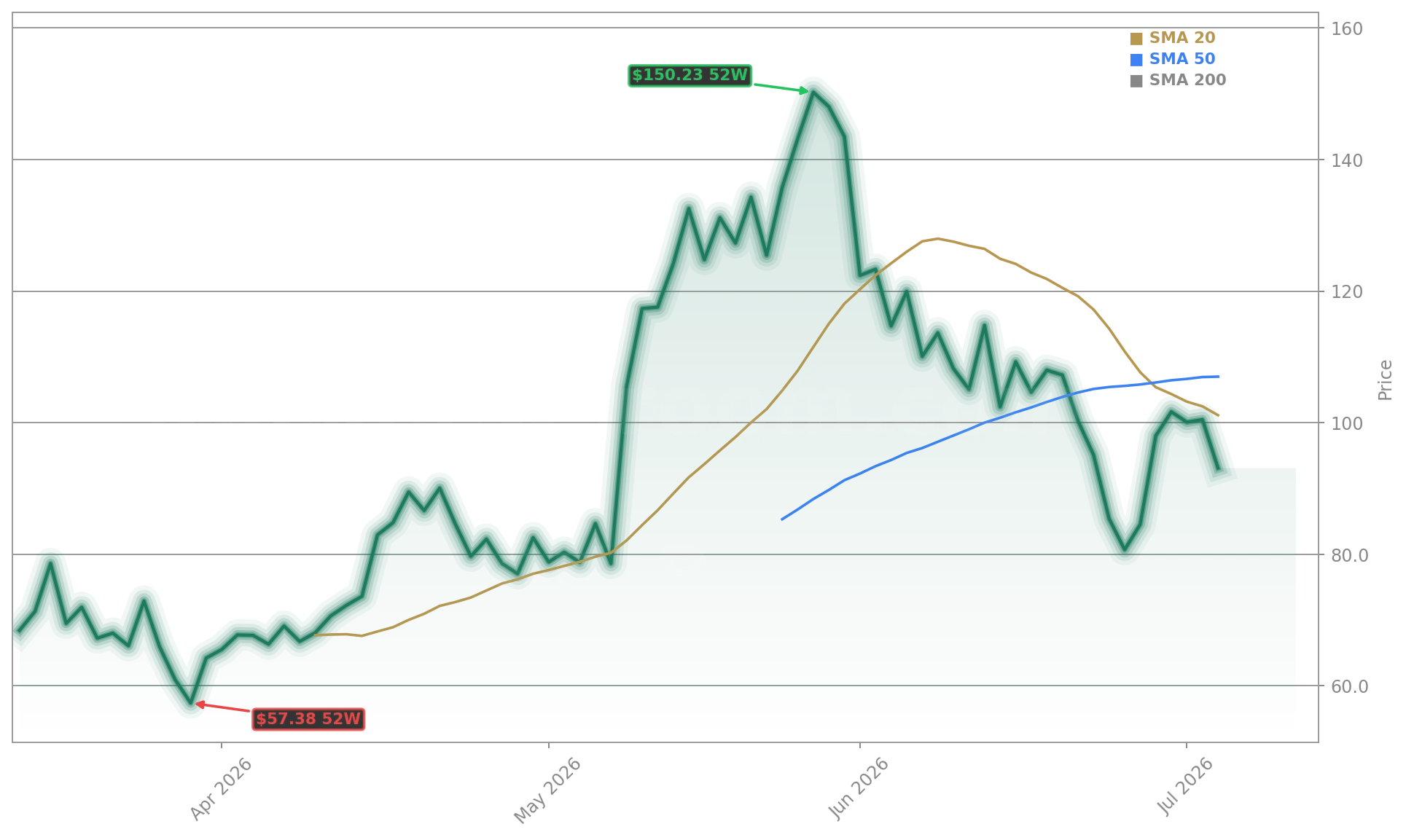

At a $58 billion market cap and 30.8x estimated 2026 revenue, Rocket Lab USA, Inc. trades at a premium—but one increasingly backed by execution. RBC Capital Markets recently upgraded the stock to ‘Outperform’, citing “accelerating Neutron integration timelines and Iridium’s cash flow stability.” The firm raised its 12-month price target to $112, implying 23% upside from current levels. Still, volatility remains. RKLB’s -2.34% intraday move on July 7 reflects broader NASDAQ caution ahead of Fed commentary—but also sector rotation into space infrastructure names ahead of Q3 earnings season. With S&P 500 space-related stocks up 18% year-to-date, Rocket Lab USA, Inc. remains among the top three contributors to the index’s technology subsector performance, alongside NVIDIA and Tesla.

What’s Next After the Rocket Lab Share Sale?

The next 90 days will be pivotal. Beyond potential sales from the registered 5 million shares, investors await FAA approval for Neutron’s first orbital test (target: August 15), the SEC’s review of the Iridium merger (expected August 22), and Q2 2026 earnings—due August 6. Unlike many growth stocks, Rocket Lab USA, Inc. is generating positive operating cash flow from Electron launches and has $1.4 billion in cash and equivalents. That balance sheet strength supports its aggressive capital deployment, including $420 million in new Neutron production facility investments announced last week. As Wall Street recalibrates space infrastructure valuations, the Rocket Lab Share Sale serves less as a red flag and more as a liquidity checkpoint ahead of transformational scale.

The Iridium acquisition isn’t about scale—it’s about sovereignty. Rocket Lab USA, Inc. now controls the entire stack, from satellite design to spectrum rights to launch cadence.— Peter Beck, Founder and CEO, Rocket Lab USA, Inc.

Related coverage: The strategic implications of the Iridium deal are explored in depth in Rocket Lab Acquisition +10.4% as Iridium Deal Sparks Surge, while broader valuation pressures across industrial and tech sectors are analyzed in Caterpillar Short Bet -7% as Valuation Fears Deepen.