Can the Rocket Lab Iridium Acquisition justify RKLB’s premium valuation even as a 5-million-share registration rattles investors?

What Does the Rocket Lab Iridium Acquisition Mean for NASDAQ?

The Rocket Lab Iridium Acquisition redefines Rocket Lab USA, Inc.’s role in the $420 billion global space economy. Unlike pure-play launch providers, Rocket Lab now controls end-to-end capability — from building Neutron rockets to operating a fully licensed, mission-ready satellite constellation serving 2.55 million government and commercial users. Analysts at RBC Capital Markets note this integration could compress customer acquisition costs by up to 35% across defense and IoT verticals. With Iridium’s 2025 revenue of $871 million added to Rocket Lab’s projected $914 million in 2026 launch and hardware sales, the combined entity is on track for ~$1.8 billion in annual revenue — a figure that would place it among the top three U.S. space infrastructure companies by revenue, trailing only SpaceX and Lockheed Martin. The deal also grants Rocket Lab immediate access to Iridium’s $1.2 billion backlog and global regulatory approvals — critical advantages as the S&P 500’s technology sector seeks scalable, non-China-exposed infrastructure plays.

Why Did Equatorial Trust Register 5 Million Shares?

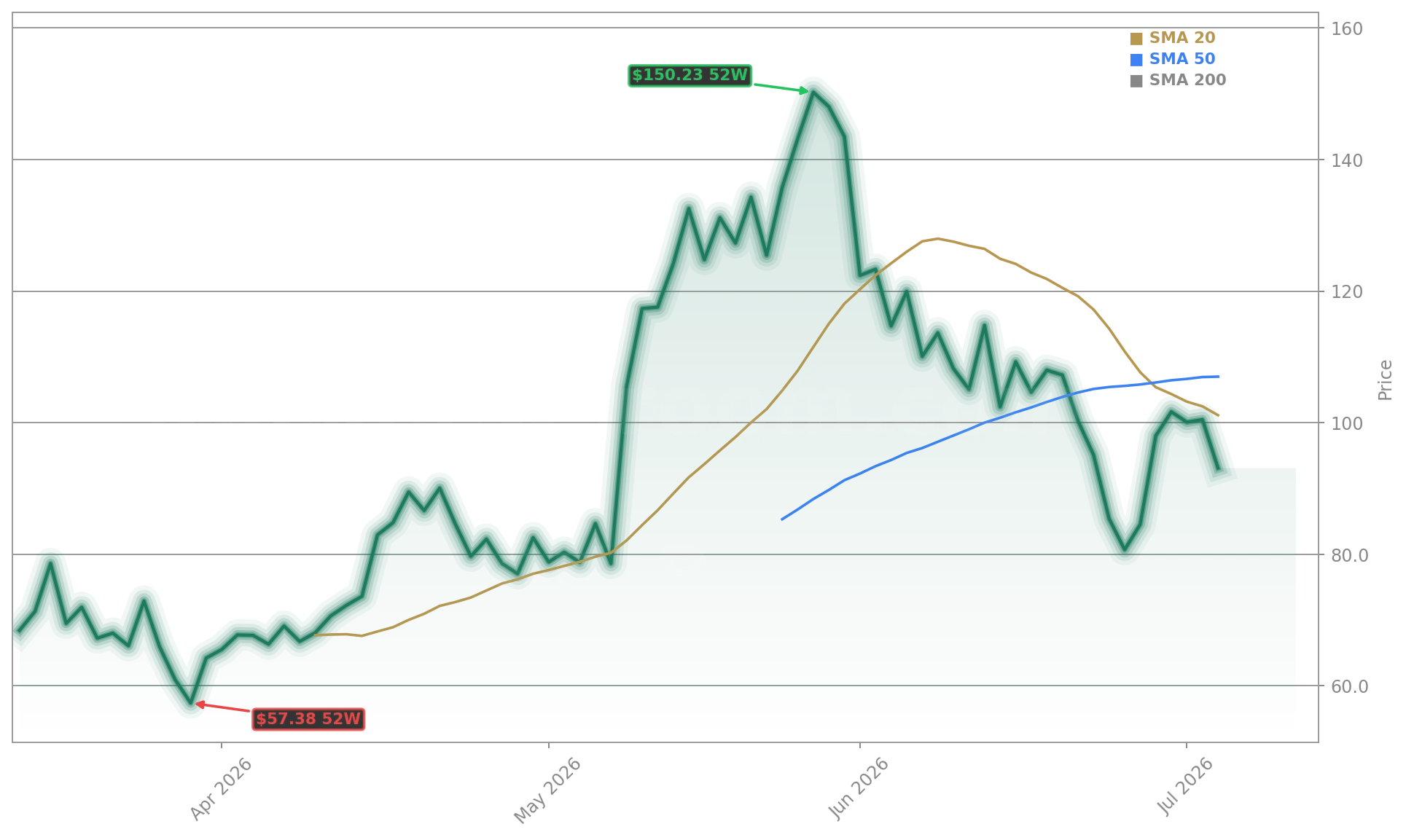

Equatorial Trust — a long-standing beneficial owner — filed Form 144 on July 6, 2026, registering 5,000,000 shares of Rocket Lab USA, Inc. for potential sale via Goldman Sachs & Co. The filing signals no material change in beneficial ownership but reflects standard liquidity planning ahead of the Iridium integration and Neutron’s first orbital flight, expected in late Q3 2026. While RKLB fell 2.52% to $90.72 in pre-market trading — its lowest level since April — the volume-weighted average price over the past 20 days remains 12% above the 52-week low, suggesting institutional accumulation continues beneath the surface. Citigroup analysts reiterated their ‘Buy’ rating last week, citing ‘unmatched vertical alignment’ and upgraded the 12-month price target to $118, citing Iridium’s EBITDA margin profile (38%) and cross-selling runway.

How Does This Stack Up Against SpaceX and Starlink?

Rocket Lab USA, Inc. isn’t aiming to replace SpaceX — it’s building the first credible, public-market alternative to Starlink’s integrated stack. Where Starlink relies on proprietary ground infrastructure and proprietary user terminals, Rocket Lab’s acquisition of Iridium brings certified, interoperable L-band services already embedded in U.S. DoD, maritime, and aviation supply chains. That gives Rocket Lab immediate credibility in federal contracting — a sector where Apple and Tesla face growing scrutiny over supply chain dependencies. Meanwhile, Neutron’s reusable architecture, designed for 15+ flights per vehicle, positions Rocket Lab to undercut Falcon 9’s marginal launch cost by 2027, per Morgan Stanley’s latest space infrastructure model. Importantly, unlike SpaceX’s private status, Rocket Lab’s public listing offers U.S. investors direct exposure to both launch services and satellite comms — a rare dual-leveraged bet in the NASDAQ’s top-performing subsector this year.

What’s Next for Rocket Lab’s Valuation?

At a $58 billion market cap and 30x estimated 2026 revenue, Rocket Lab USA, Inc. trades at a steep premium — but one that’s increasingly justified. The Rocket Lab Iridium Acquisition adds $1.1 billion in annual EBITDA potential, lifts gross margins by ~1400 bps, and de-risks Neutron’s commercialization path through guaranteed payload demand. Goldman Sachs analysts now forecast 42% compound annual growth in adjusted EPS from 2026–2029 — outpacing the S&P 500’s tech sector median by 17 percentage points. With Q3 2026 earnings due August 12, 2026, all eyes are on Neutron’s first orbital test and Iridium’s Q2 subscriber growth — both key triggers for a potential upgrade to ‘Outperform’ by major Wall Street firms.

The Rocket Lab Iridium Acquisition is the most consequential vertical integration in commercial space since SpaceX acquired Starlink in 2015. It transforms RKLB from a launch vendor into a sovereign infrastructure platform.— RBC Capital Markets Space Analyst

Related Coverage: Is the Rocket Lab Insider Sale just routine profit-taking, or a real warning before Neutron and Iridium become the next big test? Rocket Lab Insider Sale -2.7% Warning Before Neutron Debut. For context on how satellite infrastructure valuations are shifting across the sector, see Space Infrastructure Valuation Shift: Iridium, SES, and Viasat Under Pressure. Also critical: Neutron Rocket First Flight Delay: What It Means for RKLB and Competitors.