Is the Rocket Lab Insider Sale just routine profit-taking, or a real warning before Neutron and Iridium become the next big test?

What does the Rocket Lab Insider Sale signal?

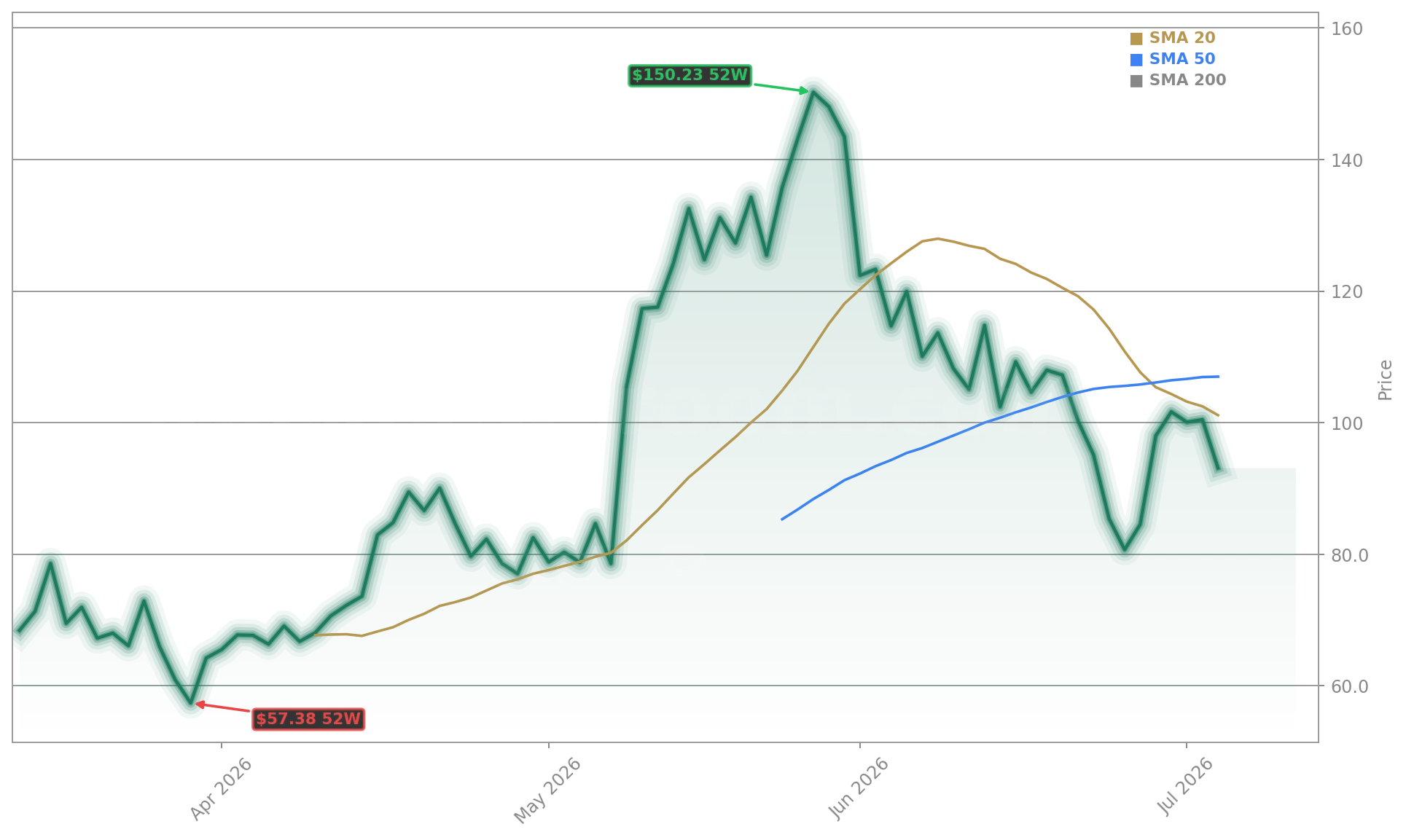

Equatorial Trust, a long-standing beneficial owner, registered 5 million shares for sale via Form 144 with the SEC on July 6, 2026 — a filing that permits sales over the next 90 days. While not unusual for large stakeholders post-lockup, the timing stands out: it follows Rocket Lab USA, Inc.’s record Q1 2026 launch bookings and precedes Neutron’s first orbital test, expected in late Q3 2026. The shares represent roughly 1.8% of the current float and were registered through Goldman Sachs & Co. No disclosure indicates urgency or distress; however, the move adds near-term supply pressure amid a 52-week high of $112.30 — meaning RKLB remains 20% below its peak despite strong fundamentals. For NASDAQ investors, this Rocket Lab Insider Sale is less about insider pessimism and more about portfolio rebalancing amid a rapidly expanding space economy.

How does Neutron change Rocket Lab’s competitive positioning?

Neutron is Rocket Lab USA, Inc.’s answer to SpaceX’s Falcon 9 dominance — a fully reusable, medium-lift launch vehicle designed for daily cadence, human-rated capability, and rapid turnaround. With over 40 missions already booked — including U.S. Space Force and ESA contracts — Neutron shifts Rocket Lab USA, Inc. from a small-sat specialist to a full-stack launch and satellite infrastructure provider. That directly challenges SpaceX’s market share in the $12 billion global medium-lift segment, where margins are expanding faster than in small-lift. Morgan Stanley analysts note Neutron’s first orbital flight “could catalyze a 20–25% re-rating if payload delivery and recovery are validated,” especially as Apple and Tesla explore low-earth orbit connectivity for next-gen vehicle autonomy and AI edge computing.

Why did Rocket Lab USA, Inc. acquire Iridium?

The $8 billion acquisition of Iridium Communications transforms Rocket Lab USA, Inc. into a vertically integrated space infrastructure player — combining launch (Electron, Neutron), satellite manufacturing (Photon), and global L-band communications (Iridium’s 66-satellite constellation). With 2.55 million government and commercial subscribers — including U.S. DoD, maritime fleets, and IoT networks — Iridium delivers predictable, high-margin recurring revenue. That offsets the capital intensity of launch development and creates cross-selling opportunities: new satellite operators now gain one-stop access to launch, build, and beam. Citigroup raised its price target to $105, citing “Iridium’s cash flow stability as a key de-risking catalyst for RKLB’s long-term growth thesis.”

Is Rocket Lab USA, Inc. overvalued ahead of earnings?

At a $58 billion market cap and ~30x estimated 2026 revenue of $1.8 billion (including Iridium), Rocket Lab USA, Inc. trades at a premium — but not an outlier in the space sector. For comparison, NVIDIA trades at 38x forward revenue, while aerospace peers like Lockheed Martin trade at 1.4x book. RBC Capital Markets maintains a ‘Sector Perform’ rating, warning that “near-term volatility will persist until Neutron demonstrates flight reliability and Iridium integration milestones are reported.” Yet the S&P 500’s space-related index has outperformed the broader market by 14% year-to-date — signaling institutional confidence in the sector’s inflection. The Rocket Lab Insider Sale may have triggered a technical pullback, but fundamentals remain intact.

What’s next for Rocket Lab USA, Inc. investors?

Wall Street eyes three near-term catalysts: Neutron’s first orbital flight (Q3 2026), Iridium’s Q2 2026 integration update (due July 22), and RKLB’s Q2 2026 earnings report (August 12). Goldman Sachs recently upgraded Rocket Lab USA, Inc. to ‘Buy’, citing “compelling synergy capture potential and first-mover advantage in sovereign LEO infrastructure.” With $1.2 billion in cash and no debt, Rocket Lab USA, Inc. is financially positioned to execute — and the Rocket Lab Insider Sale appears to be a tactical liquidity event, not a strategic retreat.

Neutron’s first orbital flight could catalyze a 20–25% re-rating if payload delivery and recovery are validated.— Morgan Stanley analysts

Related Coverage: For deeper context on today’s move, see Rocket Lab Share Sale -2.3%: 5M Shares Hit the Market, where Editor-in-Chief Maik Kemper analyzes whether this is routine profit-taking or a warning sign ahead of Neutron’s next milestone. The Iridium acquisition isn’t about scale alone — it’s about control of the full stack, from launchpad to user terminal.