Are SanDisk Earnings signaling a durable AI super‑cycle in memory, or just the hottest phase of a classic boom‑bust?

How strong were SanDisk Earnings this quarter?

The latest SanDisk Earnings for fiscal Q3 2026 marked a clear inflection point for the company’s AI strategy. Revenue jumped 251% year over year to $5.95 billion for the quarter ended April 3, driven primarily by explosive demand from cloud and AI datacenter customers. Non‑GAAP earnings swung from a loss of $0.30 per share a year ago to a profit of $23.41 per share, underscoring how quickly the pricing environment in both DRAM and NAND has turned in SanDisk’s favor.

Datacenter revenue alone reached about $1.47 billion, with AI‑focused storage shipments leading the way. Management highlighted that hyperscalers are no longer buying just spot capacity; they are signing multiyear supply agreements to secure access to high‑performance memory. Year to date, SanDisk has secured five new long‑term contracts, with three of them in the prior quarter representing roughly $42 billion in minimum contractual revenue — more than triple the company’s revenue over the last 12 months.

On the outlook side, SanDisk guided for fiscal Q4 sales of around $8 billion, alongside rising gross margins and projected profits between $30 and $33 per share. Those figures lean heavily on continued tightness in AI‑class DRAM and NAND, with April DRAM prices reportedly up about 57% versus Q1 averages and NAND pricing higher by 65% to 70%.

What is driving SanDisk versus Micron and peers?

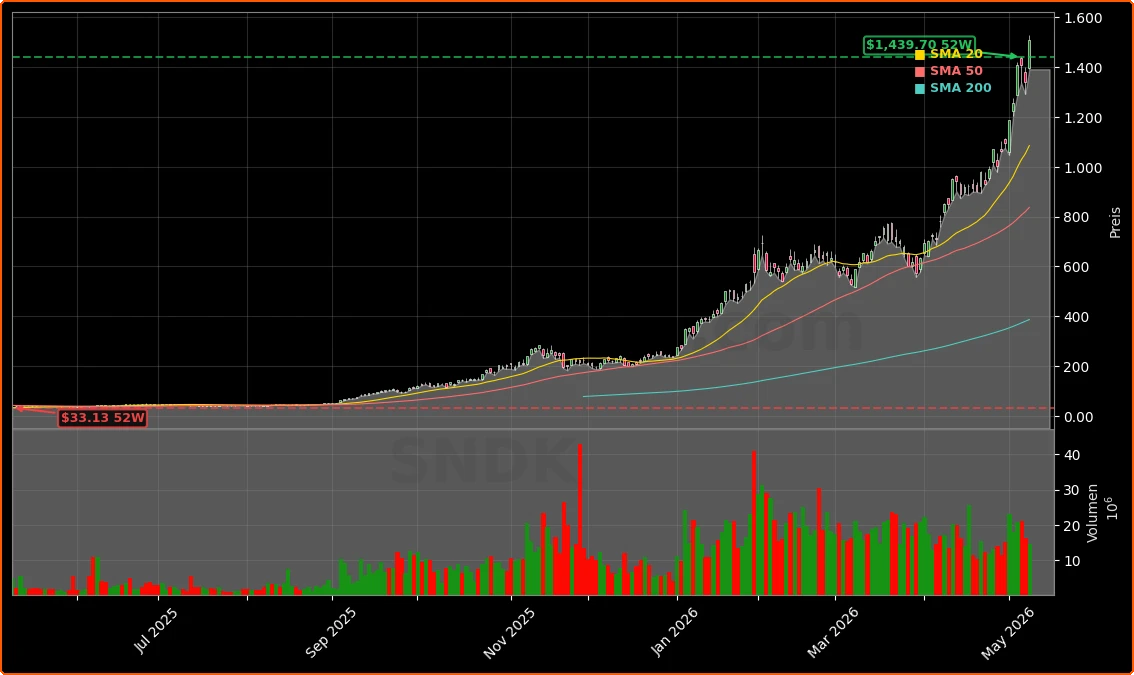

SanDisk’s rally is unfolding against the backdrop of an AI‑led melt‑up across the semiconductor complex. The PHLX Semiconductor Sector index has massively outperformed the S&P 500 over the past three years, and memory names are now at the center of the trade. Micron Technology and Western Digital have also posted outsized gains, but SanDisk stands out with a roughly 528% surge in 2026 alone, putting it firmly in price‑discovery mode.

Investors have increasingly come to see memory suppliers as leveraged beneficiaries of the same trends powering NVIDIA and other AI GPU makers. While GPUs grab the headlines, every high‑end AI accelerator stack requires vast pools of DRAM and NAND to train and run large language models. That reality has turned what was once viewed as a notoriously cyclical segment into a potential structural growth story, at least for this phase of the AI build‑out.

Wall Street analysts are taking note. Bernstein, which recently warned about spot‑market volatility, still believes SanDisk can be attractive up to roughly $1,700 per share. Mizuho Securities analyst Vijay Rakesh reiterated a Buy rating and lifted his price target to $1,625, citing the strength of AI‑related contracts and SanDisk’s improving profitability. Several research shops now model SanDisk’s earnings increasing more than 20x this fiscal year and another 2.6x next year if supply shortages persist.

Are SanDisk shares overheating despite strong SanDisk Earnings?

The same SanDisk Earnings that are fueling the bull case are also raising questions about sustainability. After a 400%‑plus year‑to‑date run heading into this week, Thursday brought a sharp pullback as traders took profits. Short interest has ticked higher, and some high‑profile bears such as Michael Burry have warned broadly that parts of the market resemble the 1999 tech bubble. Technical indicators like the relative strength index (RSI) suggest the stock is heavily overbought, a point several trading desks have echoed.

Fundamentally, there are clear risk flags. Memory has historically been the most cyclical corner of semis, and Bernstein recently cautioned that elevated DRAM and NAND prices are already forcing some OEMs and module houses to trim purchases. That could cause price increases to slow meaningfully into Q3 2026, even if near‑term guidance is still secure. Any pause or reset in hyperscaler capital spending for AI infrastructure would feed quickly through to demand for SanDisk’s products.

At the same time, AI infrastructure spending remains enormous. Research highlighting roughly $725 billion of committed hyperscaler capex for 2026 suggests that SanDisk and peers like Micron and Western Digital may still be early in the deployment cycle. For long‑term U.S. investors with diversified portfolios containing names such as Apple or Tesla, SanDisk increasingly represents a higher‑beta, AI‑levered satellite holding rather than a core defensive position.

How should investors read the SanDisk Earnings surprise?

For now, the SanDisk Earnings beat cements the company as a central player in the AI memory and storage boom. The combination of triple‑digit revenue growth, multiyear contracted backlog and a favorable pricing environment offers a compelling narrative, particularly compared with more mature megacaps where growth has normalized. Yet valuation and volatility risks are rising in tandem with the share price.

Active traders may focus on whether today’s gains hold into the close and how the stock behaves around upcoming AI conferences and hyperscaler updates. Longer‑term investors will be watching closely for signs that DRAM and NAND shortages persist into 2027 and that AI workloads continue to expand beyond cloud training into edge devices and enterprise deployments. If that scenario plays out, SanDisk’s current earnings power could prove to be less of a spike and more of a baseline.

Related Coverage: For a deeper dive into how the latest SanDisk Earnings fit into the broader AI memory supercycle, readers can explore our earlier analysis in SanDisk Earnings +251% Rally on Record AI Demand, which examines whether a traditionally cyclical memory business can evolve into a durable AI compounder.

In summary, SanDisk Earnings showcase a company riding the center of the AI infrastructure wave, with record demand, expanding margins and a growing long‑term contract base. For U.S. investors, the stock offers high‑octane exposure to AI data center growth but demands a strong stomach for swings and careful position sizing. The next few quarters of AI capex data and memory pricing trends will determine whether today’s momentum can translate into a sustained leadership role in the NASDAQ’s AI ecosystem.