Is the SanDisk NAND Boom losing steam after a parabolic run, or is today’s sharp drop just another shakeout in a supercycle?

Is the SanDisk NAND Boom finally cooling?

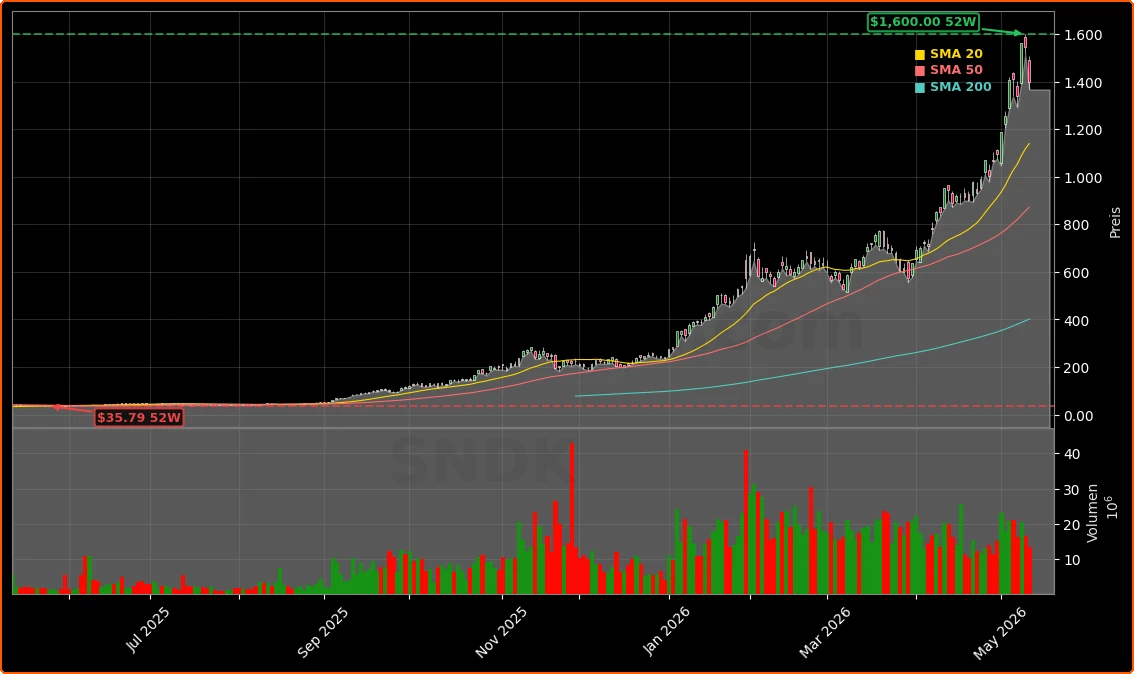

SanDisk stock has been one of Wall Street’s most explosive AI infrastructure winners since its spinoff from Western Digital in February 2025. From just under $40 at listing to recent levels around $1,400, the move of more than 3,000% in a little over a year has turned the SanDisk NAND Boom into a core high‑beta proxy for AI data center demand. On Tuesday, however, the stock is giving back some of that upside, trading roughly 9.69% below Monday’s close of $1,538 as profit‑taking sweeps through the memory and storage complex.

The pullback is sector‑wide rather than company‑specific. Micron Technology and Western Digital are each down high single digits, while other chipmakers tied to AI infrastructure, including NVIDIA, also trade lower. With SanDisk shares still up more than 500% year to date and more than 3,000% over 12 months, even a near‑10% drop looks like a routine consolidation within an extreme uptrend rather than a fundamental break in the SanDisk NAND Boom story.

How strong are SanDisk (Western Digital) fundamentals?

The latest quarterly figures underpin why the stock became a poster child for the AI memory cycle. In fiscal Q3 2026, which ended April 3, SanDisk (Western Digital) delivered adjusted earnings of $23.41 per share, a dramatic swing from a loss of $0.30 a year earlier. Revenue surged to $5.95 billion, up 251% year over year, with the data center segment soaring 645% as hyperscalers raced to secure high‑performance NAND flash for AI training and inference clusters.

Market research from Gartner points to a brutal supply‑demand imbalance, with NAND prices projected to jump more than 200% in 2026 as AI data centers, smartphones, PCs and edge devices all compete for wafers. Counterpoint Research expects elevated memory pricing to persist beyond 2027, suggesting that the SanDisk NAND Boom may be more than a short‑lived spike. Importantly for investors, management has been able to lock in that favorable backdrop via multi‑year supply agreements: three contracts signed last quarter carried minimum revenue commitments of $42 billion, followed by two additional long‑term deals this quarter whose values have not yet been disclosed.

Those agreements include variable pricing clauses designed to “capture upside if prices rise,” giving SanDisk leveraged exposure to any further NAND price appreciation. That optionality, combined with aggressive earnings momentum, has driven a wave of upward estimate revisions from Wall Street research desks, with some models now projecting nearly $172 in earnings per share within a couple of fiscal years.

What does the pullback signal for US investors?

For American portfolios, the current drop is less about deteriorating fundamentals and more about position management after a parabolic advance. Heading into this week, SNDK had rallied roughly 65% in a single month and closed Monday near $1,548, not far from its recent peak. At these levels, SanDisk has arguably become the highest‑beta memory play tied to the AI build‑out, a role that means both outsized upside in risk‑on phases and violent reversals when traders rotate or de‑risk.

Compounding the volatility, global policy headlines are creeping into the narrative. Political debate in South Korea over potential windfall taxes on AI‑driven “excess profits” has reminded investors that governments, not just competitors, may seek a share of the economic rents created by AI infrastructure. While SanDisk is a US company with limited direct exposure to Korea, it does maintain manufacturing relationships across Asia, including China and Japan, where similar policy ideas could eventually surface.

So far, large US brokerages remain focused on earnings power rather than policy risk. Research teams at Goldman Sachs and Morgan Stanley have highlighted the durability of the AI memory upcycle and the earnings torque from tight supply, even as they warn clients about the potential for steep drawdowns after such massive gains. Several houses, including JPMorgan and Bank of America, continue to frame SanDisk as a core play on the AI storage stack, though updated ratings and price targets following this latest move have yet to be published.

Is a SanDisk NAND Boom stock split on the table?

With the SNDK share price having recently approached $1,500, speculation about a potential stock split is intensifying. Technology leaders from Apple to Tesla and NVIDIA have used forward stock splits in the past decade to make their shares more accessible to retail investors during strong bull runs. For SanDisk, a 10‑for‑1 forward split would theoretically bring the price down to around $150 without changing its market capitalization, simply multiplying the share count.

Such a move would be cosmetic from a valuation standpoint, but history suggests splits can improve liquidity, tighten spreads and support inclusion in a broader range of retail portfolios and some index products. Citigroup and RBC Capital Markets have both flagged the high nominal share price as a potential constraint for smaller investors, arguing that a split could marginally expand the shareholder base even in an age of fractional trading. Still, both banks emphasize that the long‑term trajectory of the SanDisk NAND Boom will be dictated by earnings, contract visibility and the shape of the AI investment cycle, not the number of shares outstanding.

Related coverage: what else should investors read?

For a deeper dive into how recent numbers fit into the broader AI cycle, investors can review our detailed earnings breakdown in SanDisk Earnings +251% Surge: Is the AI Boom Sustainable?. That analysis explores whether SanDisk’s 251% revenue jump and massive EPS beat are early signs of a durable AI super‑cycle in memory or simply the hottest phase of a classic boom‑bust pattern in semiconductors.

In summary, the SanDisk NAND Boom remains intact fundamentally, even as the stock finally digests a year of extraordinary gains with a near‑10% daily drop. For US investors, the key question is not whether today’s pullback marks the end of the story, but whether earnings, contracts and AI capex can continue to compound fast enough to justify even higher levels over the next few years. As the next quarters reveal how long the NAND shortage and AI spending wave can last, SanDisk (Western Digital) will stay a central barometer for the entire AI memory trade.