Can SanDisk’s explosive AI-fueled earnings surge really turn a notoriously cyclical memory business into a long-term compounder?

How strong were SanDisk Earnings this quarter?

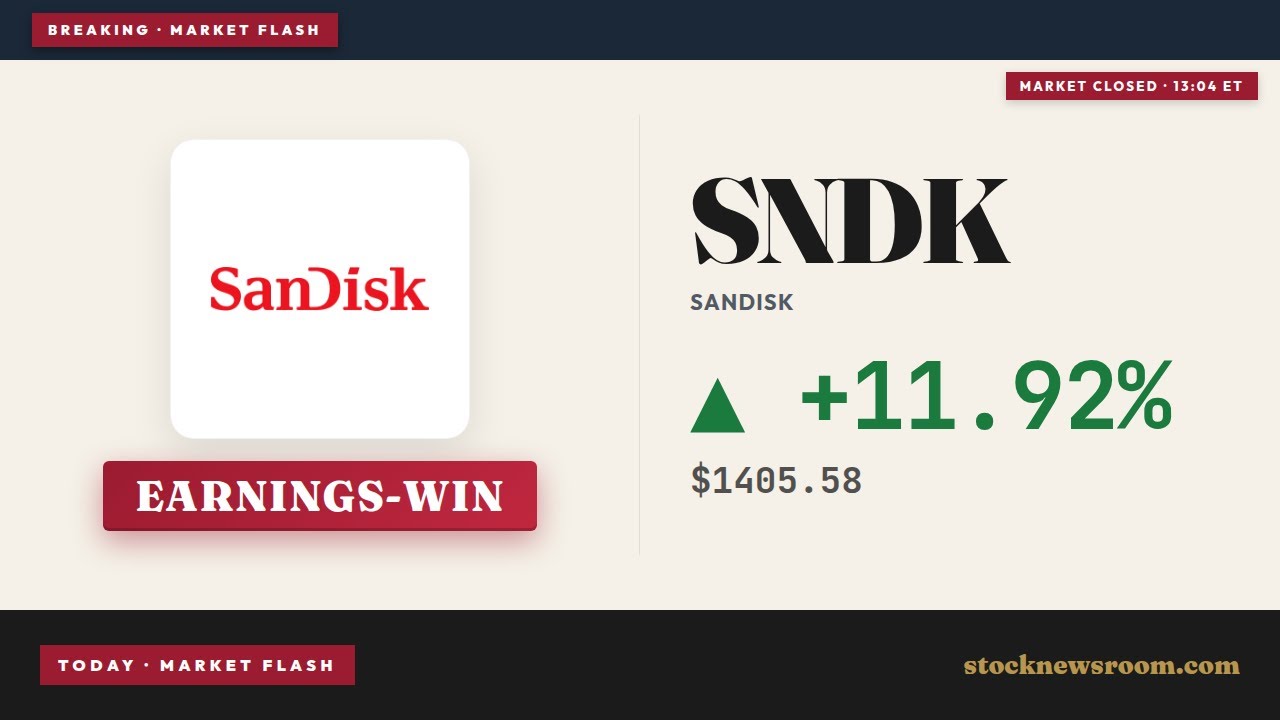

SanDisk (Western Digital) delivered one of the most eye‑catching reports of this earnings season. For fiscal Q3 2026, revenue jumped 251% year over year to roughly $5.9 billion–$6.0 billion, driven by surging demand for NAND flash tied to AI infrastructure. The data center segment led the charge, with sales rocketing about 645% to $1.47 billion as hyperscale cloud providers ramped purchases of high‑performance SSDs.

Profitability flipped dramatically. Non‑GAAP earnings per share came in around $23–$23.41, compared with a loss of $0.30 a year ago and far ahead of prior guidance of $12 to $14. Gross margin expanded to approximately 78%–78.4%, up from just 22.5% last year and 50.9% in Q2, reflecting sharply higher NAND prices and a richer mix of enterprise drives.

Management’s outlook was equally aggressive. For fiscal Q4, SanDisk guided revenue to $7.75–$8.25 billion, up from about $1.9 billion in the prior‑year quarter, with gross margin expected between 78.9% and 80.9%. Non‑GAAP EPS is projected to jump from $0.29 a year ago to $30–$33. On the back of these SanDisk Earnings, the stock touched fresh 52‑week highs last week and is now trading around $1,397, up 11.33% today and nearly 500% in 2026.

What is driving SanDisk’s AI and NAND supercycle?

At the core of the SanDisk Earnings story is a structural shortage in memory, especially NAND. After a brutal downturn a few years ago, major memory makers cut NAND output and shifted capacity to DRAM. That left supply tight just as AI data centers began scaling aggressively, fueling a sudden need for massive, high‑performance SSDs to store training data and large language models alongside GPUs from leaders like NVIDIA.

SanDisk develops a broad portfolio of NAND‑based products, from embedded flash for mobile and automotive to enterprise SSDs for cloud and AI workloads. The company’s joint venture with Kioxia in BiCS 3D NAND gives SanDisk access to low‑cost wafers, allowing it to compete on price while still expanding margins as selling prices rise.

Management is also pushing new technologies such as high‑bandwidth flash (HBF), designed to bridge the performance gap between GPU compute and storage throughput by feeding data into HBM faster. Sampling of HBF is planned for the second half of this year, positioning SanDisk as a key enabler of real‑time AI inference at scale, alongside ecosystem partners like Apple in devices and cloud rivals of Tesla’s in‑house AI efforts.

Do long-term contracts change the SanDisk Earnings profile?

One of the most important developments this quarter was the move to longer‑duration supply agreements. SanDisk signed five new “new business model” (NBM) contracts, three during Q3 and two shortly after. The three signed in the quarter alone represent at least $42 billion in committed purchases and are backed by about $11 billion in third‑party financial guarantees, significantly improving visibility.

These agreements combine fixed and variable pricing and are expected to cover more than one‑third of SanDisk’s BiCS production next fiscal year. For investors, that means part of the company’s volume and pricing is locked in over as long as five years, a notable shift for a sector infamous for boom‑and‑bust swings. If management continues to add such contracts, future SanDisk Earnings could become less volatile, supporting higher sustained valuation multiples.

The strengthened balance sheet adds another pillar. SanDisk recently paid down roughly $650 million in debt, leaving it essentially debt‑free, and approved a new share repurchase program funded by robust free‑cash‑flow generation. Wall Street consensus currently sees adjusted earnings growing at about a 25% annual rate through fiscal 2028, even assuming a slowdown beyond that.

How is Wall Street valuing SanDisk versus peers?

Analysts across Wall Street have been racing to update models following the SanDisk Earnings surprise and the stock’s surge. Cantor Fitzgerald’s CJ Muse, one of the more vocal bulls, recently set a $1,800 price target on SNDK, implying more than 25% upside from current levels and arguing that SanDisk still looks attractive at roughly 38 times forward adjusted earnings given its AI leverage.

Not everyone is all‑in at these prices. Barclays, for example, has maintained an “Equal Weight” or Hold stance on the shares even as it has raised its target to around the low‑$1,200s, flagging the risk that memory pricing could normalize later in the decade. Research at 24/7 Wall St. pegs a one‑year fair value closer to $1,181.83, slightly below today’s price, implying modest downside after the huge rally.

From a broader NASDAQ and S&P 500 perspective, SanDisk now sits alongside NVIDIA as a core AI infrastructure beneficiary. Memory rival Micron is also riding the wave, but recent commentary from multiple banks suggests SanDisk may offer greater operational torque to NAND pricing given its higher exposure to flash and its new contract structure. With the stock up over 3,000% in 12 months, however, volatility around future SanDisk Earnings and any shift in AI spending remains a key risk.

Related Coverage

For a deeper dive into how the AI memory boom could impact the next phase of the rally, readers can review our earlier analysis in SanDisk Forecast +7.2% Rally: Record AI Memory Boom. That piece explores whether current demand trends mark the beginning of a new multiyear supercycle or a perfection‑priced peak, and how position sizing in SNDK might fit into a diversified tech portfolio.

NAND flash is emerging as the only economically viable solution to deliver the capacity, performance, and efficiency required to keep models accessible for real-time inference at scale.— David Goeckeler, CEO of SanDisk (Western Digital)

In sum, the latest SanDisk Earnings underscore how central the company has become to AI infrastructure, combining record revenue, margin expansion, and multi‑year contracts with a fortress balance sheet. For US investors, SNDK is now a high‑beta lever on both AI spending and NAND pricing, with analyst targets ranging from cautious to extremely bullish. The next few quarters of SanDisk Earnings and contract wins will be crucial in determining whether today’s valuation is a staging ground for further gains or a plateau after an extraordinary run.