Can Super Micro Computer Product Launch momentum survive a sharp sell-off, or is Wall Street already questioning the AI infrastructure story?

What triggered Super Micro Computer Product Launch momentum?

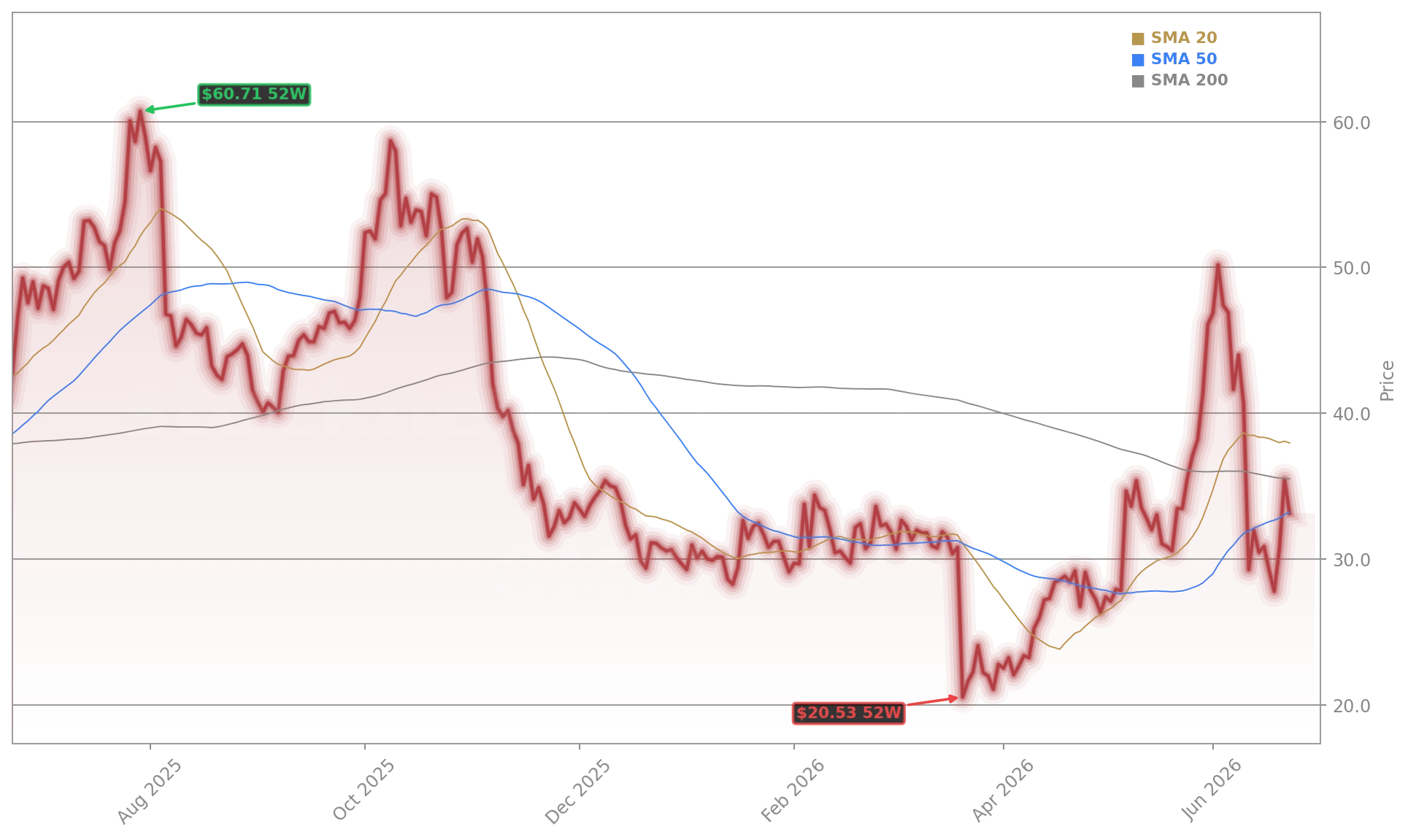

Super Micro Computer, Inc. surged 15.7% to $35.46 on Monday — its strongest single-day gain in over a year — after unveiling its end-to-end Data Center Building Block Solutions (DCBBS) Blueprint for NVIDIA’s Vera Rubin NVL4 platform at the ISC 2026 conference in Hamburg. Unlike previous server announcements, this Super Micro Computer Product Launch delivers a fully integrated, liquid-cooled, turnkey infrastructure solution: each 3.2MW Scalable Unit supports up to 1,152 NVIDIA Rubin GPUs and 576 NVIDIA Vera CPUs, with native FP64 performance for scientific computing. The blueprint covers everything from site survey and power/cooling validation to white-glove deployment and 4-hour on-site support — a critical differentiator in an era where AI infrastructure bottlenecks now constrain model development far more than chip supply.

How does this impact Wall Street’s AI infrastructure thesis?

Wall Street is rapidly recalibrating its AI infrastructure valuation framework — and Super Micro Computer, Inc. is now front and center. While NVIDIA remains the undisputed chip leader, the Vera Rubin NVL4 launch confirms that the next AI growth vector lies in full-stack integration. Competitors like Dell Technologies and Hewlett Packard Enterprise report strong AI server demand, but Super Micro Computer, Inc. is the only major vendor delivering validated, scalable, liquid-cooled HPC-AI convergence at this density and speed. Its DCBBS model — already deployed in clusters exceeding 100,000 GPUs — directly addresses the infrastructure scarcity highlighted by Anthropic’s $1.25 billion/month deal with xAI. That dynamic shifts investor focus from pure GPU exposure to companies enabling physical deployment at scale — a structural tailwind for Super Micro Computer, Inc. and its peers in the NASDAQ’s AI hardware cohort.

Why did GF Securities upgrade — and what’s the price target?

GF Securities upgraded Super Micro Computer, Inc. from ‘Hold’ to ‘Buy’ with a $48 one-year price target — implying 35% upside from Monday’s close. Analyst Evan Lee cited improved visibility into AI server demand, accelerated SpaceX-related orders expected in 2027, and the company’s ability to convert its $39 billion AI server backlog into profitable revenue. Notably, GF Securities called the recent 28% pullback — triggered by the $7 billion equity-linked financing announcement — an ‘attractive entry point.’ The upgrade stands in contrast to Wolfe Research’s ‘Hold’ rating issued earlier this month, which flagged legal risk tied to co-founder Wally Liaw’s indictment and ongoing board review of export-control transactions.

Can margins and balance sheet sustain the growth?

Scientific discovery has always been driven by the tools available to researchers, and AI has become an essential part of the research process.— Charles Liang, CEO of Super Micro Computer, Inc.

Gross margin recovery to 9.9% — up from 6.3% last quarter — signals progress, but pressure remains. The company’s $8.8 billion in bank debt and convertible notes, plus $7 billion in new equity financing, reflects aggressive scaling to meet hyperscaler demand. Yet cash flow remains strained: Super Micro Computer, Inc. burned $6.6 billion in operating cash flow in Q3 FY2026, even as revenue hit $10.24 billion. Management insists the shift toward complete, ready-to-run systems — rather than bare servers — is driving margin expansion. For U.S. investors, the critical question isn’t just top-line growth, but whether Super Micro Computer, Inc. can achieve sustainable profitability without diluting equity or overleveraging — especially as the S&P 500’s tech-weighted index faces increasing scrutiny on valuation and execution risk.