Can Super Micro Computer Financing turn a battered AI server stock into a real comeback story?

What Does the Super Micro Computer Financing Mean for AI Infrastructure?

Super Micro Computer Financing delivers immediate balance sheet flexibility to fulfill its massive $39 billion AI server order book — a figure that dwarfs the $10.24 billion in revenue reported for Q3 FY2026. Unlike traditional server vendors, Super Micro Computer, Inc. designs, validates, and delivers full-rack AI solutions tailored for generative AI workloads, competing directly with custom builds from NVIDIA-powered OEMs and cloud-native infrastructure providers. The $7 billion package — led by J.P. Morgan, Goldman Sachs, and Citigroup — was structured to avoid near-term dilution while providing runway: the 7.0% Series A mandatory convertible preferred shares mature in 2029 and convert into common stock at a 30% premium to the $27.50 common offering price. That structure signals confidence in sustained top-line acceleration and margin recovery — two critical levers Wall Street is watching closely.

How Does SMCI Compare to Dell and HPE Today?

Super Micro Computer, Inc. rose 11.02% on Thursday, while Dell Technologies traded flat at $417 and Hewlett Packard Enterprise fell 2% to $47 — underscoring divergent investor sentiment within the AI server ecosystem. Dell’s 231% YTD gain and HPE’s 97% rally highlight their stronger margin profiles and broader enterprise software integration, whereas Super Micro Computer, Inc. trades at a steep 15x trailing P/E versus Dell’s 33x and HPE’s 46x. That discount reflects ongoing concerns: a board-led independent review of export-control compliance and $8.8 billion in total debt. Yet the Super Micro Computer Financing de-risks near-term execution — and analysts are taking notice. Citigroup recently raised its SMCI price target to $37.25, citing improved component procurement visibility. RBC Capital Markets maintains a ‘Sector Perform’ rating but notes the financing ‘removes a key overhang for near-term delivery confidence.’

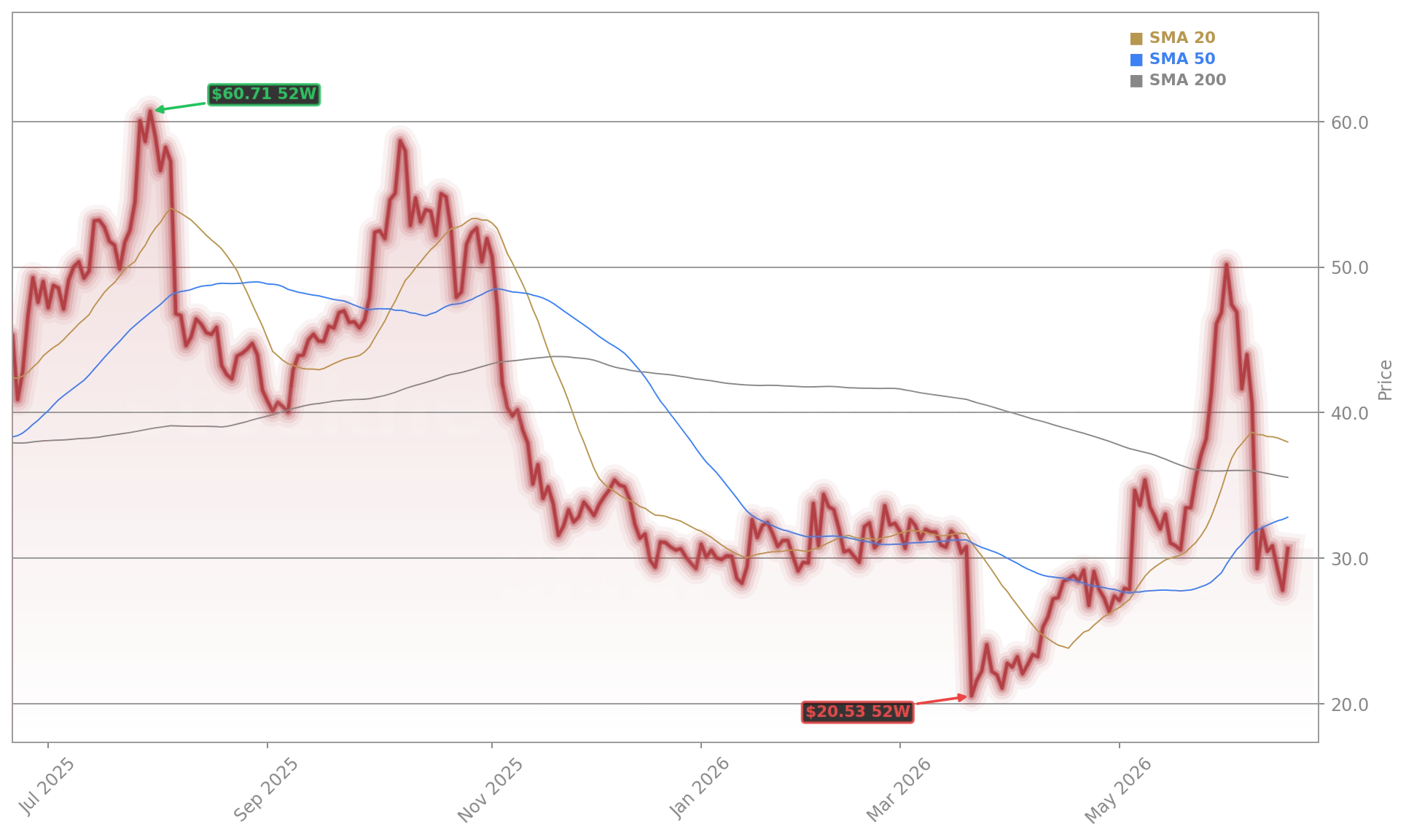

Is the Momentum Breakout Real or Just a Short Squeeze?

SMCI’s technical picture remains conflicted. While the stock rebounded sharply from $27.78 to $30.84, it still trades 20.3% below its 20-day SMA and 7% below its 50-day SMA. The 200-day SMA remains a hard ceiling at $35.60 — just above the critical $36.00 resistance zone. MACD remains negative, and the ‘death cross’ formed in December 2025 remains intact. Yet Benzinga’s Edge Scorecard reveals a compelling fundamental setup: Quality (96.78) and Value (86.58) scores rank in the top 5% of the S&P 500, while Growth (66.49) and Momentum (9.54) lag. This divergence suggests the Super Micro Computer Financing may catalyze a longer-term re-rating — if price can clear $36 and hold above the 50-day moving average for three consecutive sessions.

What’s Next for Super Micro Computer, Inc.?

Next week’s focus shifts to gross margin trajectory and updates on the export-control review. With AI server lead times stretching beyond 20 weeks, Super Micro Computer, Inc. must convert its $39 billion order book into high-margin revenue — not just backlog. The company’s modular, open-architecture approach gives it agility versus vertically integrated rivals, but also exposes it to component cost volatility. Meanwhile, competitors like Tesla and Apple are building sovereign AI stacks with in-house silicon, raising the bar for infrastructure partners. Goldman Sachs expects Q4 FY2026 revenue to grow 22% sequentially and gross margin to expand 180 basis points — a forecast that hinges on successful execution of the Super Micro Computer Financing. For investors, the near-term test is simple: hold $36, confirm volume-supported follow-through, and watch for margin validation in the next earnings release.

The financing removes a key overhang for near-term delivery confidence.— RBC Capital Markets

Related coverage includes a deep dive into the strategic implications of the Super Micro Computer Stock Offering: $7B Raise Tests Bulls, and how global chip dynamics are shifting with Taiwan Semiconductor AI Growth Surges 5.7% on AI Demand.