Can Super Micro’s massive capital raise secure its AI backlog, or will dilution and execution risk keep crushing sentiment?

Why is Super Micro Financing needed now?

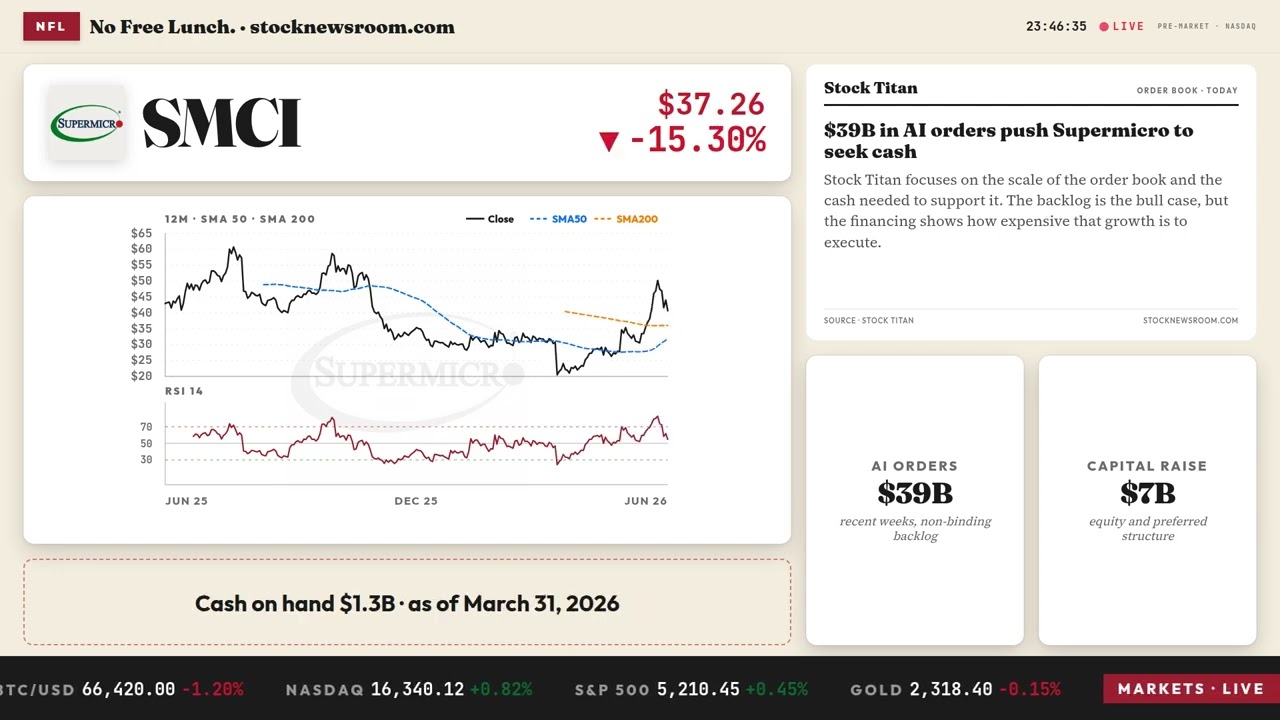

Super Micro Computer, Inc. is executing one of the largest hardware-focused capital raises in recent memory—not to shore up balance sheet weakness, but to scale fulfillment velocity. With $39 billion in AI server orders received in recent weeks, the company faces an unprecedented procurement challenge: memory costs have more than tripled, and lead times for high-bandwidth interconnects and liquid-cooling systems remain stretched. Its $1.3 billion in cash as of March 31, 2026, is insufficient to cover component prepayments and supply chain deposits required to lock in production slots. The $7 billion Super Micro Financing is explicitly structured to bridge that gap—prioritizing speed over cost, with J.P. Morgan, Goldman Sachs & Co. LLC, and Citigroup serving as joint bookrunners.

How does this compare to peers like Dell and HPE?

Unlike Dell Technologies, which reported 181% year-over-year growth in Infrastructure Solutions Group revenue and funded expansion through operating cash flow and debt, Super Micro Computer, Inc. is leaning heavily on equity. Hewlett Packard Enterprise (HPE) recently raised $1.5 billion in convertible notes—but for strategic M&A, not working capital. The contrast highlights Super Micro’s unique position: a pure-play AI server assembler with minimal vertical integration, making it more capital-intensive per dollar of backlog. That dynamic has drawn scrutiny from analysts at RBC Capital Markets, which downgraded SMCI to ‘Underperform’ last week, citing ‘execution risk on the $39 billion order book and mounting dilution pressure.’

What’s the dilution impact on shareholders?

The Super Micro Financing includes up to $1.25 billion in new common shares and $3.75 billion in depositary shares—each representing 1/20th of a newly issued mandatory convertible preferred stock. With conversion slated for June 1, 2029, and no current public market for SMCIP, investors face near-term equity dilution without clear near-term upside. Morgan Stanley analysts noted in a June 9 research note that ‘even with strong order visibility, the timing and scale of this raise increases near-term overhang risk for retail-heavy holders.’ That sentiment contributed to SMCI’s 9% after-hours slide—outpacing broader tech selloffs, as Yahoo Finance reported AI hardware stocks like Dell and Hewlett Packard Enterprise also dropped sharply amid high-beta rotation.

Super Micro Financing: What’s next for the NASDAQ listing?

While the $2 billion at-the-market program won’t begin until Q3 2026, the underwritten offerings are expected to close within weeks. Super Micro Computer, Inc. plans to list the depositary shares on the Nasdaq Global Select Market under the symbol ‘SMCIP.’ Regulatory filings—including an updated Form 8-K filed June 9—also disclose expanded risk factors related to export controls, supply chain dependencies, and ongoing legal proceedings. That disclosure coincides with recent coverage on export-control scrutiny, including Super Micro Computer Export Controls: SMCI Jumps 7%, which analyzed how geopolitical constraints could affect delivery timelines for Chinese and Middle Eastern customers.

Is this a buy-the-dip moment for S&P 500 tech exposure?

Not yet—for most institutional portfolios. While SMCI remains a key enabler for NVIDIA-driven AI clusters and has deep integration ties with cloud providers, its valuation multiple has surged to 32x forward earnings—well above the NASDAQ Composite’s 27x average. Citigroup analysts maintain a ‘Neutral’ rating with a $42 price target, emphasizing ‘execution clarity over order size’ as the next catalyst. Meanwhile, the $39 billion backlog remains non-binding per SEC disclosures and subject to cancellation or delay. For investors seeking AI infrastructure exposure with lower volatility, diversified plays like Apple—with its AI-integrated silicon roadmap—or Tesla, leveraging AI for autonomous driving, offer more balanced risk profiles. Super Micro Financing is a signal of demand intensity—not yet a signal of margin sustainability.

Even with strong order visibility, the timing and scale of this raise increases near-term overhang risk for retail-heavy holders.— Morgan Stanley analyst, June 9, 2026

Super Micro Financing underscores a pivotal inflection point: massive AI infrastructure demand is real, but scaling to meet it requires capital discipline that Wall Street is still pricing in. For U.S. investors, this isn’t just about one stock—it’s about how AI hardware supply chains absorb pressure without breaking. The next quarterly earnings will test whether Super Micro Computer, Inc. can convert backlog into revenue without eroding margins or shareholder value. For aggressive growth portfolios, the opportunity remains compelling—but only after the financing closes and execution evidence mounts.