Can Super Micro Computer’s AI momentum outrun the export-control risks now hanging over one of Wall Street’s most volatile hardware names?

What’s Driving SMCI’s 7% Rally Today?

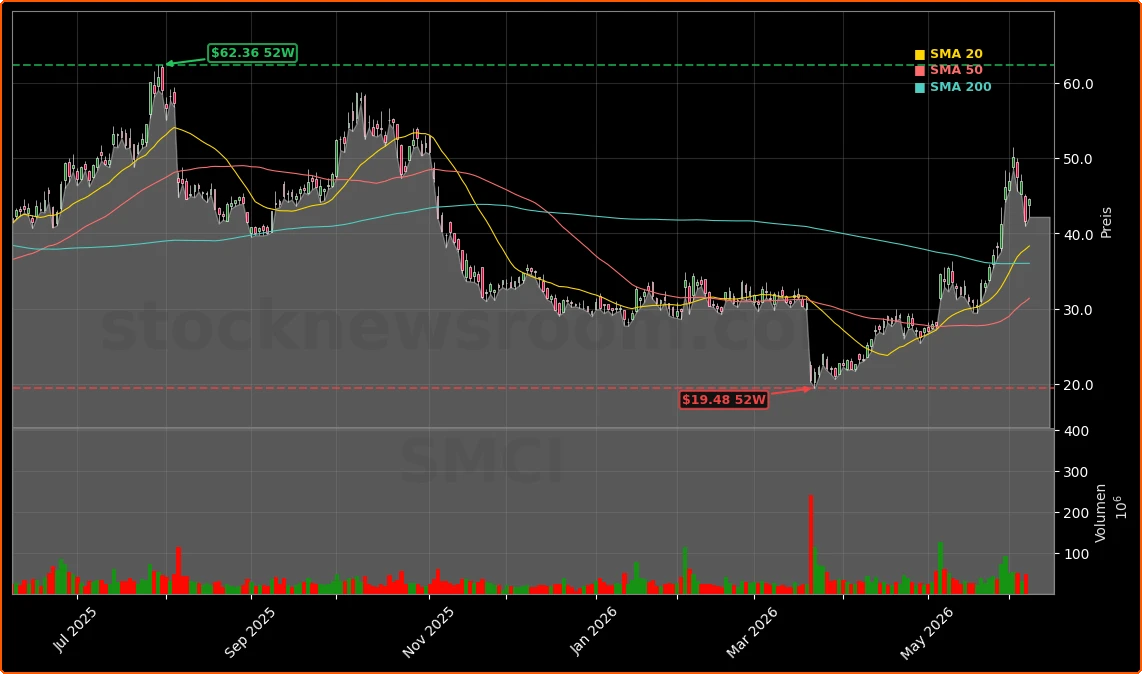

Super Micro Computer, Inc. surged in premarket and intraday trading Monday as chip stocks rebounded from Friday’s 4.8% Nasdaq 100 collapse. While Micron (MU) and Intel (INTC) led the semiconductor bounce, SMCI’s 7% gain stood out—especially given its recent volatility and Friday’s sharp drop, triggered by a hotter-than-expected May jobs report (172,000 vs. 80,000 consensus) and Broadcom’s soft AI guidance. Traders interpreted the move as a dip-buy opportunity, reinforced by tangible product momentum: the June 2 Computex launch of its AMD Helios 72-GPU rack and a new Arm AGI server collaboration. A $2 billion AI infrastructure agreement with Gorilla Technology for India deployments also added near-term revenue visibility—bolstering the case that SMCI remains deeply embedded in the global AI build-out.

How Do Super Micro Computer Export Controls Impact U.S. Investors?

This is the defining question for American portfolios holding SMCI. Unlike peers such as Dell Technologies and Hewlett Packard Enterprise, Super Micro Computer, Inc. faces active federal scrutiny over alleged violations of U.S. export controls. In March 2026, prosecutors charged SMCI’s co-founder and two others with conspiring to divert $2.5 billion in Nvidia-equipped servers to China via shell companies in Southeast Asia. Though SMCI is not named as a defendant, the company confirmed cooperation with Taiwanese authorities that led to three arrests and seizure of 50 servers in late May. Crucially, Super Micro Computer Export Controls failures could trigger secondary sanctions—potentially restricting U.S. vendors from supplying components, jeopardizing contracts with federal agencies, and accelerating market-share loss to more compliant rivals. That dynamic explains why Dell posted outsized gains amid SMCI’s recent weakness: institutional buyers are rotating toward regulatory safety.

Can SMCI’s AI Growth Offset Its Trust Deficit?

Fiscal Q3 2026 (ended March 31, 2026) delivered 123% year-over-year revenue growth—but also a 19% sequential decline, starkly contrasting with Dell’s and Micron’s strong sequential expansion. Net profit margins remain stuck at or below 5%, far short of Dell’s AI-driven margin surge. Meanwhile, trust issues linger: Hindenburg Research’s 2024 short report alleging accounting manipulation still casts a shadow, and SMCI missed its own Q3 FY26 revenue guidance by $2.1 billion ($10.2B delivered vs. $12.3B guided). Mizuho analyst Vijay Rakesh recently raised SMCI’s price target from $36 to $44 but maintained a ‘Neutral’ rating, citing persistent CPU and memory supply constraints through 2027. The firm emphasized upside potential in agentic AI demand—but flagged Super Micro Computer Export Controls as a material, unresolved overhang.

Where Does SMCI Fit in the Broader AI Hardware Landscape?

While agentic AI creates strong server tailwinds, SMCI’s exposure to export control enforcement remains a non-negotiable risk factor for U.S. institutional allocations.— Vijay Rakesh, Mizuho Securities

Super Micro Computer, Inc. occupies a unique niche: custom AI server motherboards, liquid-cooling racks, and full-stack infrastructure optimized for chips from NVIDIA, AMD, and now Arm. Its Vera Rubin-based Data Center Building Block Solutions (DCBBS) aim to accelerate large-scale AI deployments, while its partnership with NANO Nuclear Energy on KRONOS microreactors signals long-term thinking about AI’s energy demands. Yet relative to peers, SMCI lacks the balance sheet strength of Apple or the enterprise channel depth of Dell. Its valuation—still trading well below all-time highs despite 1,000%+ gains over five years—reflects investor hesitation. With Goldman Sachs now forecasting zero Fed rate cuts in 2026 and money markets pricing in a 25-basis-point hike by year-end, high-multiple AI hardware names like SMCI face mounting pressure to prove operational execution—not just hype.