Can Texas Instruments turn rising AI power demand into a lasting growth story, or is this rally getting ahead of itself?

Why is the Texas Instruments Forecast improving?

Texas Instruments Incorporated delivered Q1 2026 revenue of $4.8 billion, up 9% sequentially and 19% from a year earlier, helping confirm that demand is recovering after a long semiconductor slowdown. That fundamental turn is now being reinforced by analyst upgrades tied to AI infrastructure, especially the rising power intensity inside modern server racks.

Seaport Research upgraded Texas Instruments to Buy from Neutral and set a $400 price target. Analyst Jay Goldberg argued that higher electricity usage in data centers is forcing redesigns of power distribution systems, creating a meaningful opportunity for analog semiconductor suppliers. BofA also turned more constructive, raising its price target to $370 from $320 and saying Texas Instruments has the largest data center business among its peer group. Mizuho lifted its target to $300 from $255 while maintaining a Neutral rating, citing stronger AI server demand across analog and memory markets.

Can Texas Instruments outgrow peers?

The market is beginning to treat Texas Instruments less as a mature cyclical chip name and more as a strategic supplier to power-hungry AI systems. That matters because analog and power management chips do not always get the same investor attention as GPUs from NVIDIA, yet they are essential for converting, regulating, and distributing electricity efficiently inside data centers.

This is where the Texas Instruments Forecast is gaining momentum. Analysts increasingly see a second leg of growth beyond traditional industrial and automotive markets. Trading interest has also been supported by optimism around the company’s internal manufacturing strategy and newer automotive semiconductor products with AI-related features. The combination gives Texas Instruments exposure to both AI infrastructure and electrification trends, while maintaining a broad customer base across embedded processing and analog products.

Competitor comparisons are becoming more favorable as well. While firms such as Qualcomm remain more tied to mobile and communications cycles, Texas Instruments is positioned around power content, industrial recovery, and automotive electronics. That diversification could help the stock remain resilient if spending patterns shift across end markets.

What does Texas Instruments stock action say?

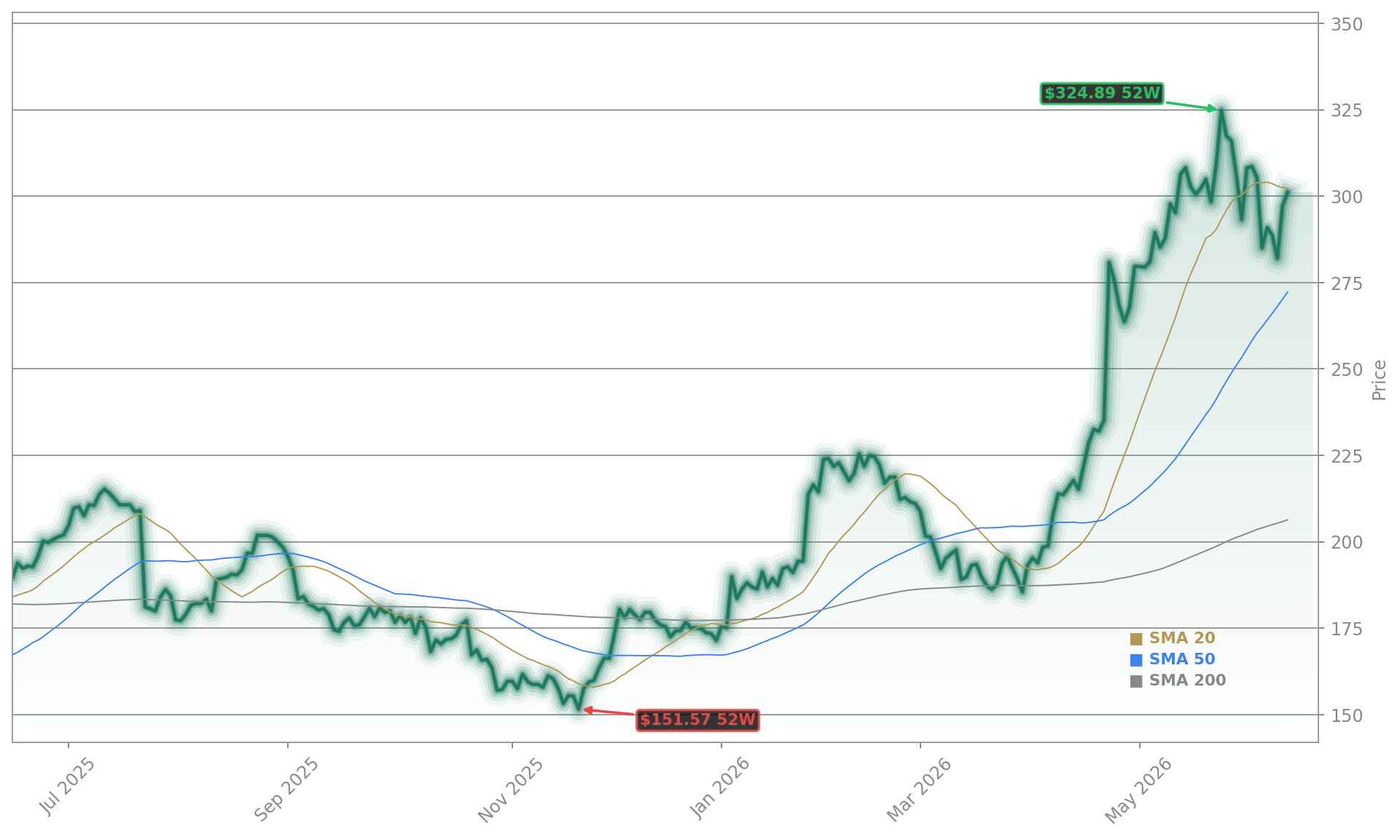

At $322.83, the stock is trading well above the May 22 close of $309.21 cited in recent market commentary, showing that bullish sentiment has accelerated over the past few sessions. Investors should still be careful with headline claims about “new highs” unless confirmed by full 52-week data, but the recent move clearly signals strong momentum.

The Texas Instruments Forecast is also being helped by rising institutional interest. Hedge fund ownership rose to 78 portfolios at the end of the fourth quarter from 72 in the prior quarter. Momentum-focused research has highlighted the stock’s outperformance against the broader semiconductor group and the S&P 500, while valuation-focused bulls argue that improving factory utilization and moderating capital spending could support stronger free cash flow in 2026.

There are still risks. Analog demand can remain cyclical, supply constraints across semiconductors may persist into 2027, and large acquisitions can introduce integration uncertainty. Investors are also watching the planned Silicon Labs deal and broader spending trends from hyperscalers and enterprise customers such as Apple and Tesla that influence electronics demand across multiple verticals.

What should investors watch next?

The next test for the Texas Instruments Forecast will be whether data center power demand translates into sustained revenue acceleration and margin expansion over coming quarters. If management continues to post better-than-expected guidance, Wall Street could keep revising estimates higher, especially with Seaport Research at $400 and BofA at $370 now framing the upside debate.

Related Coverage: Investors looking for a deeper read on the company’s last major catalyst can revisit this analysis of the Texas Instruments earnings surge after its big beat. That earlier report explains why analog chips may be emerging as quiet winners in the AI infrastructure buildout and provides useful context for today’s stronger price action.

The Texas Instruments Forecast has turned more constructive as AI data center demand, analyst upgrades, and a recovering analog cycle align. For investors, the key question is whether these tailwinds can justify the stock’s sharp rerating. If upcoming quarters confirm stronger power-management demand and improving cash flow, Texas Instruments could remain one of Wall Street’s more compelling large-cap semiconductor stories.