Could Alibaba AI Regulation turn China’s export controls into an unexpected profit catalyst for one of its biggest tech champions?

What’s Driving Alibaba’s 11% Pre-Market Jump?

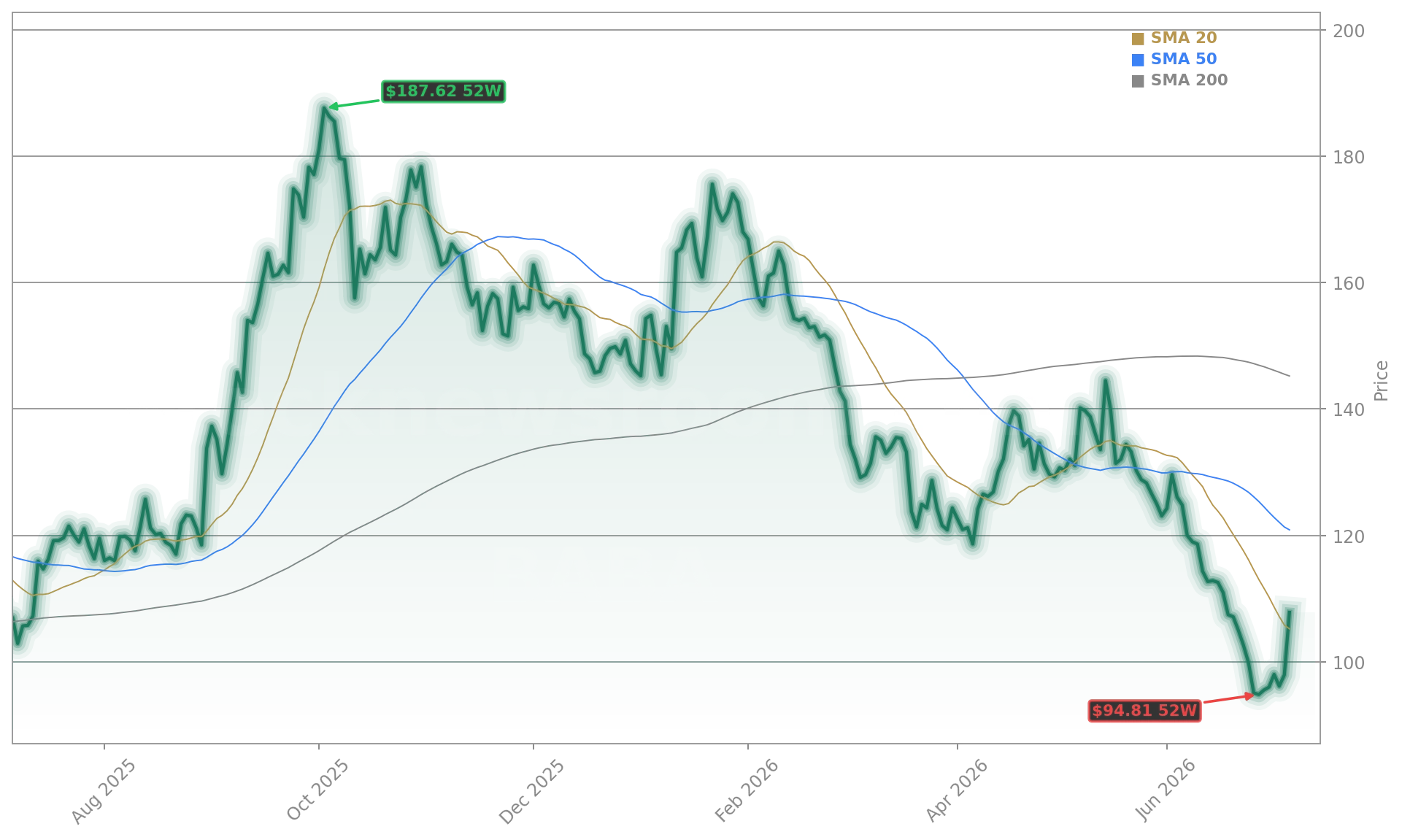

Alibaba Group Holding Limited surged in pre-market trading after a confluence of catalysts: a positive business update ahead of its August 28 earnings report, a judicial reprieve from a U.S. lobbying ban, and intensifying speculation around Alibaba AI Regulation. According to Bloomberg, the company briefed analysts that losses in its instant-commerce unit narrowed meaningfully in the June quarter, while overall profitability remained stable — a critical reassurance amid persistent concerns about margin erosion from AI investment. The stock’s 11.3% pre-market gain to $109.27 — up from $98.14 at Tuesday’s close — marks its strongest intraday move since September 2025 and comes as the Hang Seng Index rose 3.0%, outperforming a plunging KOSPI (-5.4%) and flat Nasdaq 100 futures (-1.1%).

How Does Alibaba AI Regulation Reshape Global AI Markets?

Reuters reported that Chinese regulators, including the Ministry of Commerce and National Development and Reform Commission (NDRC), held talks with Alibaba, ByteDance, and Z.ai about restricting overseas access to unreleased, high-end AI models. While still under discussion and not yet finalized, such Alibaba AI Regulation would treat unauthorized export of proprietary AI as a national security violation — mirroring recent U.S. restrictions on Anthropic’s Mythos model. The policy could create scarcity for low-cost, high-performance models like Alibaba’s Qwen series, potentially lifting token pricing and cloud margins. As Barron’s noted, Chinese AI models are already gaining traction globally due to their cost advantage over OpenAI and Anthropic — and tighter controls may accelerate that trend. This isn’t just geopolitics: it’s a direct margin catalyst for Alibaba’s cloud division, which Jefferies Hong Kong analyst Thomas Chong expects to post faster year-over-year growth this quarter.

Why Are U.S. Investors Rotating Into Alibaba Now?

After shedding 33% year-to-date, Alibaba trades at just 15.2x forward earnings — a steep discount to peers like NVIDIA (32x) and Apple (30x), despite possessing a top-tier open-source LLM stack and growing AI chip capabilities. Morningstar cut its fair value estimate by 7% to $241 — but still calls the stock ‘cheap’, citing overdone concerns about AI computing costs and cloud delivery losses. The rotation is real: while U.S. tech futures slumped, Alibaba outperformed rivals JD.com (+3.8%) and Baidu (+6.4%) and dwarfed the 12% rally in Kingsoft Cloud (KC), which Morgan Stanley recently initiated with an Overweight rating and $15 price target. ETF investors are also taking notice — Alibaba is a top-10 holding in the SPDR NYSE Technology ETF (XNTK), meaning inflows could compound momentum.

What’s Next for Alibaba’s AI Strategy and Valuation?

Alibaba’s internal pivot is accelerating: the company banned employee use of Anthropic’s Claude Code effective July 10, citing ‘backdoor intelligence risks’, and mandated adoption of its in-house Qoder assistant. This follows Anthropic’s claim that Alibaba attempted to distill its AI capabilities — a flashpoint in the broader U.S.-China AI war. Simultaneously, Alibaba is developing its own AI chips, reducing reliance on foreign hardware and lowering long-term cloud infrastructure costs. While Morningstar warns that state-led data center buildouts could pressure public cloud revenue, Chelsey Tam’s 10% annual forecast cut begins only in fiscal 2030 — leaving near-term cloud growth intact. With earnings due August 28 and Wall Street projecting $38.72 billion in revenue and $2.51 EPS — up 12% and 22% year-over-year — the next catalyst is clear: execution on AI monetization.

How Do Insider Moves Signal Confidence?

Insider activity reinforces the bullish narrative: CEO Wu Yongming exercised 41,333 RSUs on July 1, increasing his direct stake to 1,014,418 shares. Board member Joseph Tsai also added 10,833 shares via RSU vesting. Neither transaction involved open-market purchases — yet both signal alignment with long-term AI execution. This comes just weeks after the company disclosed a $1.5 billion bid for grocery delivery platform Pupu, signaling continued confidence in its consumer-tech integration thesis. Meanwhile, the $600 million U.S. compliance settlement — while a near-term cost — mandates cross-border system overhauls that could strengthen Alibaba’s global trust infrastructure ahead of AI-driven international expansion.

Related coverage: Alibaba Claude Code Ban: $600M Warning for BABA Stock unpacks how the Anthropic ban isn’t just a security move — it’s a strategic pivot in the splintering global AI market. The article details how this decision may accelerate Alibaba’s shift toward sovereign AI stacks and tighter integration with Chinese data sovereignty frameworks.

Alibaba’s A.I. has gained widespread developer adoption due to its open-source nature, making it a global hit. However, this open-source model, while attracting users by being cheaper than proprietary systems, presents a significant challenge for Alibaba in turning its popularity into a profitable business.— The New York Times

Alibaba Group Holding Limited remains a high-conviction AI play for value-oriented investors seeking exposure to China’s AI ascent. The convergence of Alibaba AI Regulation, stable core profitability, and accelerating AI monetization creates a rare inflection point. For U.S. portfolios underweight Chinese tech, this rally is more than a bounce — it’s a signal to reposition before earnings confirm the turnaround. The next quarterly earnings report will be the definitive test of whether Alibaba’s AI strategy is finally translating into scalable, profitable growth.