Can Alphabet keep its AI edge as top DeepMind talent exits and Wall Street punishes the stock?

What Do Alphabet DeepMind Departures Mean for Wall Street?

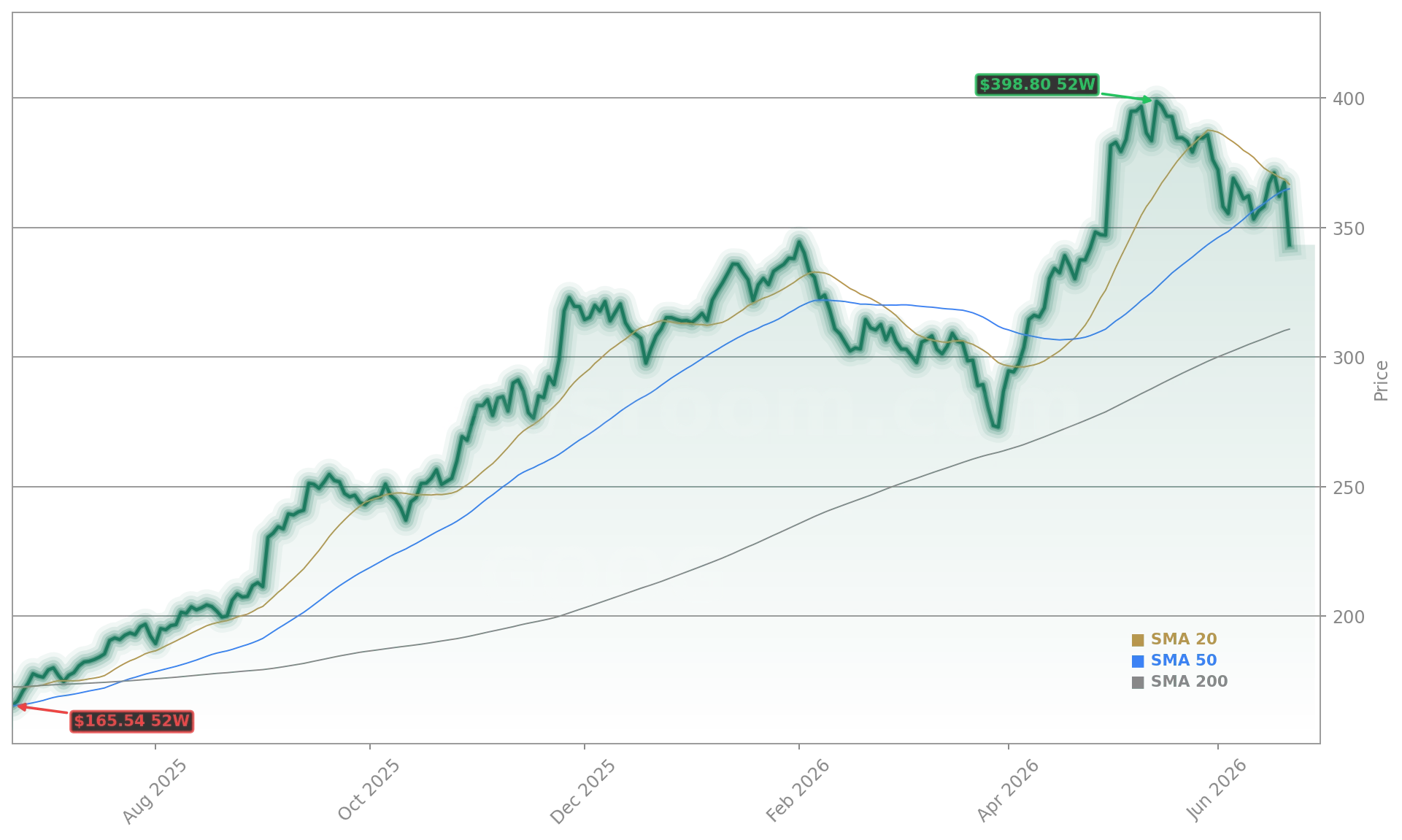

Alphabet DeepMind Departures are no longer isolated events — they’re signaling a structural shift in the AI talent war. Noam Shazeer, co-author of the Transformer and Switch Transformer papers, departed as VP of Engineering; Dean Ball, a key architect of Google’s AI policy framework, followed days later. Their exits to OpenAI — a direct competitor backed by Microsoft — have sparked investor concern about retention, morale, and long-term model leadership. Yet the market’s reaction tells a nuanced story: while GOOGL fell 6.30% intraday to $344.83, the S&P 500 rose 0.6%, suggesting the move reflects idiosyncratic risk rather than broad sector weakness. Analysts at JPMorgan note that while talent loss is real, Alphabet’s integrated stack — from Gemini models to custom TPUs and Vertex AI — remains unmatched in enterprise deployment velocity.

How Is Google Cloud Performance Reshaping the Narrative?

Google Cloud is no longer Alphabet’s growth experiment — it’s the engine. Revenue jumped 63% year-over-year to $20.03 billion, smashing consensus estimates of $18.41 billion. More critically, backlog surged to $462 billion — up from $155 billion just two quarters prior — with over 50% expected to convert within 24 months. That contracted demand dwarfs even Microsoft Azure’s reported $34.68 billion cloud revenue and reflects deep enterprise commitments, including multiple billion-dollar deals and a 45% over-delivery by existing customers. Morgan Stanley rates Alphabet overweight with a $375 price target, citing this backlog as evidence that compute scarcity is translating directly into monetized demand — not just cost pressure.

Why Is Alphabet Spending $190B on AI Infrastructure?

Alphabet’s revised 2026 capex guidance — $180 billion to $190 billion — isn’t speculation. It’s a response to unprecedented compute demand. CEO Sundar Pichai stated plainly: “Our Cloud revenue would have been higher if we were able to meet the demand.” The company is now renting 110,000 NVIDIA GB300 GPUs from SpaceX at $920 million per month — a $11.04 billion annualized expense — while also deploying custom silicon with Broadcom. That scale mirrors Meta’s $125–$145 billion capex range and Microsoft’s $190 billion forecast, confirming a hyperscaler-wide infrastructure sprint. But unlike peers, Alphabet owns the full stack: frontier models, silicon, and cloud — a vertical advantage analysts at Goldman Sachs cite as key to its $450 price target.

How Do Competitors Compare in the AI Infrastructure Race?

Alphabet’s AI infrastructure push stands in sharp contrast to Microsoft’s $37 billion AI revenue run rate — up 123% — and Meta’s $145 billion capex plan. Yet while Microsoft’s Azure growth was just 39% (in line with estimates), Alphabet’s Cloud growth accelerated for the fourth straight quarter — from 32% to 63%. That momentum is fueling enterprise adoption: HSBC just signed a multi-year deal to deploy over 200 new AI use cases using Gemini Enterprise and Google Cloud infrastructure. Meanwhile, NVIDIA remains the indispensable hardware partner, and Apple feels the strain — CEO Tim Cook recently called memory cost inflation a “100-year flood,” directly attributing the surge to hyperscaler demand from Alphabet, Microsoft, and Meta. Tesla’s AI ambitions remain focused on autonomous driving, not cloud infrastructure, placing it outside this particular capex arms race.

What Are Analysts Saying About GOOGL’s Valuation?

We are compute constrained in the near term. As an example, our Cloud revenue would have been higher if we were able to meet the demand.— Sundar Pichai, CEO of Alphabet

Despite the recent volatility, Wall Street remains overwhelmingly bullish. JPMorgan raised its target to $460, citing 19% Search growth and 63% Cloud acceleration. Goldman Sachs lifted its target to $450, highlighting Alphabet’s expanding AI opportunity. Wells Fargo reiterated its overweight rating, arguing that Google’s AI rollout reduces disruption risk to Search. Bank of America maintains a buy rating, while Citi raised its target to $405. The consensus target stands at $432.83 — implying 25% upside from current levels. With a forward P/E of 26 and 82% YoY earnings growth, Alphabet trades at a discount to its growth trajectory — a gap analysts say reflects short-term talent concerns, not long-term fundamentals.