Are the latest Amazon Earnings the start of a multi-year AWS AI supercycle or just an unusually strong quarter?

How did Amazon Earnings reset expectations?

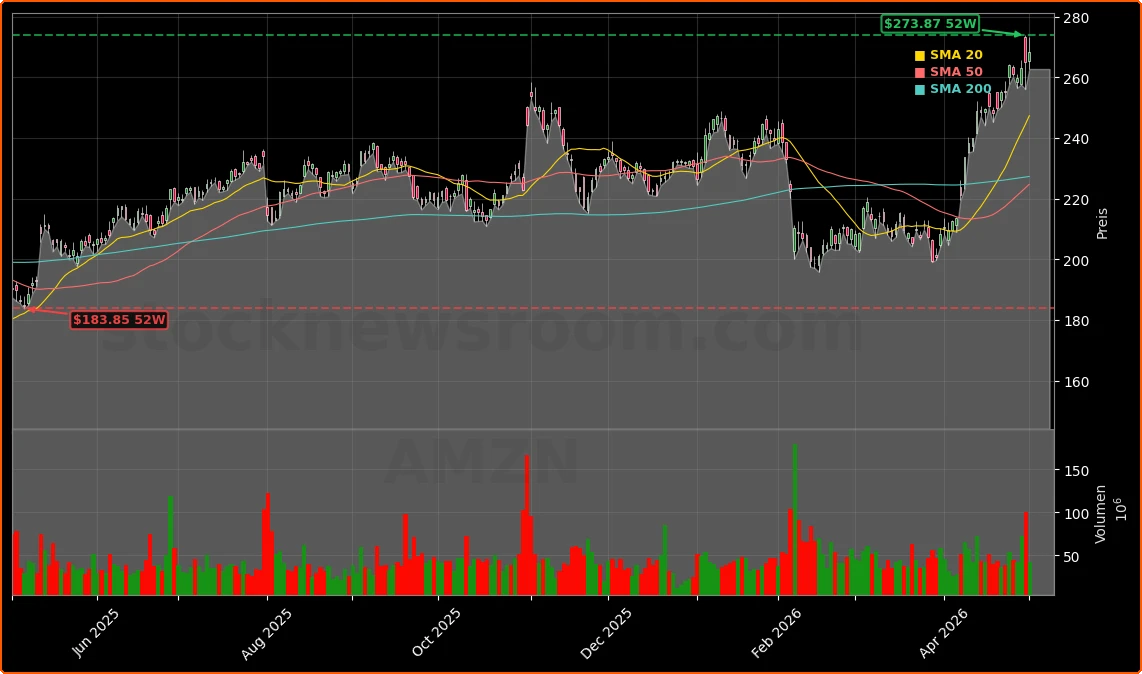

Amazon.com, Inc. posted Q1 2026 revenue of $181.5 billion, up 17% year over year and comfortably ahead of roughly $177 billion expected by Wall Street. Diluted EPS landed at $2.78, far above consensus near $1.70, helped by strong operating leverage and a sizeable pre‑tax gain of about $16.8 billion from the company’s stake in Anthropic. Operating income rose to $23.9 billion, up from $18.4 billion a year ago, as North American retail margins and advertising profitability continued to improve.

The standout in Amazon Earnings was Amazon Web Services. AWS revenue climbed 28% year over year to about $37.6 billion, marking the fastest growth in 15 quarters and extending an acceleration trend from 17% to 28% over the last four quarters. CEO Andy Jassy highlighted that AWS now represents a roughly $150 billion annualized revenue run rate, calling it “very unusual” to see this pace of growth on a base that large. Management guided Q2 revenue to a range of $194–199 billion, above prior Street expectations around $189 billion.

Why are analysts so bullish on Amazon?

The strong Amazon Earnings and AWS re‑acceleration triggered an “upgrade wave” across Wall Street. Barclays reiterated its Overweight rating and lifted its price target from $300 to $330, arguing that Amazon is building the largest AI capacity footprint among hyperscalers and that “all roads lead to AWS” as so‑called agentic AI applications scale. Morgan Stanley also kept an Overweight rating with a $330 target, raising its AWS growth forecasts to 35% and 36% for 2026 and 2027 and boosting its 2027 EPS estimate by roughly 9% to about $11.30.

Citi remains positive with a Buy rating and a $285 price target, citing accelerating AWS growth, better visibility on capacity, expanding backlog, and margin gains in retail and advertising. Raymond James upgraded Amazon to Outperform and raised its target from $225 to $280, framing AWS as one of Wall Street’s most under‑appreciated AI beneficiaries. Other large houses including Goldman Sachs and Bank of America pushed targets into the $300+ range, reinforcing a consensus that the latest Amazon Earnings mark the beginning of a multi‑year AI‑driven upcycle rather than a one‑off beat.

How central is AWS and custom silicon to the story?

For US investors focused on AI infrastructure, AWS is now the core of the Amazon Earnings narrative. The AWS backlog reached about $364 billion at quarter‑end, even before factoring in a new commitment from Anthropic reportedly exceeding $100 billion. On the AI platform Bedrock, customers processed more tokens in Q1 than in all prior periods combined, with customer spend up a striking 170% sequentially, underscoring rapid early monetization of generative AI workloads on AWS.

Behind that growth sits a fast‑expanding chip empire. Amazon’s custom silicon portfolio—Graviton CPUs, Trainium accelerators, and Nitro offload cards—has crossed an annualized revenue run rate of more than $20 billion, growing at a triple‑digit pace. Jassy has said that if this chip unit were standalone, it would be on the scale of a top‑three data‑center chip vendor globally, putting it in the same strategic conversation as NVIDIA. Trainium2 chips are largely sold out, Trainium3 is ramping with capacity mostly reserved, and Trainium4—about 18 months from broad availability—already has most of its output pre‑allocated. OpenAI has committed to roughly 2 GW of Trainium capacity on AWS starting in 2027, while Anthropic has reserved up to 5 GW, anchoring long‑term demand.

What about AI capex and free cash flow pressure?

The flip side of strong Amazon Earnings is an aggressive investment cycle. Capital expenditures in Q1 surged to about $44.2 billion, up sharply from $25 billion a year earlier, driven primarily by AI data‑center build‑outs, power infrastructure, and memory costs that Jassy says have “skyrocketed.” Industrywide, hyperscalers including Amazon, Microsoft, Alphabet, and Meta now plan to spend an estimated $700+ billion on AI‑related capex this year, with Amazon alone projected near $200 billion.

That spending has crushed near‑term free cash flow. On a trailing 12‑month basis, Amazon’s free cash flow has fallen to roughly $1.2 billion, compared with about $25.9 billion a year earlier. Even so, Amazon has notably not raised its formal capex forecast this week, suggesting that part of the apparent surge versus prior Street estimates reflects higher component prices—especially for GPUs and high‑end memory—rather than an even more ambitious build plan. For portfolio managers, the key debate is whether AWS can convert its massive chip run rate and Trainium commitments into structurally higher margins once this capex wave normalizes.

How does Amazon stack up against other tech giants?

On the NASDAQ, Amazon now sits in the same AI “super‑cap” cohort as Apple, Tesla, Microsoft, and Alphabet, but its strategic posture looks different. Unlike Apple, which so far has avoided locking itself into hundreds of billions of dollars in AI data‑center commitments, Amazon is explicitly betting its future on enterprise AI workloads. That approach more closely resembles Microsoft and Alphabet, though Amazon’s heavy emphasis on homegrown silicon could pressure GPU demand over time and challenge NVIDIA’s pricing power.

Amazon’s stock has rallied about 27% in April alone, helping power the NASDAQ Composite to its best month since 2020, alongside big AI winners in chips and cloud. With a roughly $2.9 trillion market cap, some strategists now argue Amazon could reach $4 trillion before Microsoft if AWS growth continues to accelerate, the chips business scales, and the advertising arm—already a roughly $70 billion trailing revenue stream—keeps compounding. At around 32x earnings, many on Wall Street view the valuation as reasonable relative to the company’s growth profile and AI optionality.

Related Coverage

Investors who want a deeper dive into how Amazon Earnings intersect with its AI spending can read our in‑depth feature “Amazon Earnings Q1: AWS Surge and $200B AI Capex Bet”. That analysis examines whether a $200 billion data‑center program is sustainable, how it impacts free cash flow, and what it might mean for long‑term shareholders if AWS and the custom chip business meet current growth expectations.

AWS is now a $150 billion annualized revenue run rate business. It’s very unusual for a business to grow this fast on a base this large.— Andy Jassy, CEO of Amazon.com, Inc.

In sum, the latest Amazon Earnings underscore a company leaning hard into AI infrastructure, with AWS, custom silicon, and advertising driving a powerful multi‑year story despite near‑term cash flow strain. For US investors seeking AI exposure beyond pure‑play chip stocks, Amazon offers a diversified way to participate in cloud, e‑commerce, and agentic AI growth. The next quarters will show whether AWS can sustain 28%‑plus growth and turn today’s heavy capex into tomorrow’s outsized returns.