Can the massive Amazon Anthropic Deal really reignite AWS growth and reshape the race between the biggest AI hyperscalers?

How does the Amazon Anthropic Deal reshape AI spending?

The latest phase of the Amazon Anthropic Deal commits Amazon to invest up to $25 billion in the fast-growing AI start-up, on top of roughly $8 billion already deployed since 2023. In return, Anthropic has agreed to spend more than $100 billion on AWS technologies over the next decade, cementing AWS as its primary cloud and training partner while still maintaining secondary relationships with Microsoft and Google.

The agreement secures up to 5 gigawatts of capacity for Anthropic to train and deploy its Claude models on Amazon’s custom Trainium chips, including nearly 1 gigawatt of Trainium2 and Trainium3 capacity expected online by year-end. For investors, this is a clear signal that Amazon is willing to match or exceed hyperscaler rivals in capital intensity to stay competitive in generative AI, even as chip suppliers like NVIDIA dominate the underlying GPU market.

Anthropic’s rapid product cadence — from Claude Opus 4.7, its most advanced reasoning model, to the more controversial Claude Mythos “hyper-agentic” system — underscores why it needs massive compute commitments. The Amazon Anthropic Deal directly ties that need to AWS infrastructure and silicon, creating a powerful multi-year demand pipeline for Amazon’s cloud segment.

What could Anthropic mean for AWS growth?

Wall Street is increasingly focused on how Anthropic’s growth flows through to AWS revenues. KeyBanc analyst Justin Patterson highlights that Anthropic’s annual recurring revenue has jumped from $9 billion in December 2025 to roughly $30 billion by early April 2026. With the assumption that about 60% of Anthropic’s cloud spend lands on AWS, the firm sees a “meaningful tailwind” to Amazon’s cloud growth trajectory.

AWS generated $128.7 billion in revenue in 2025, up 20% year over year. Patterson now sees a realistic path to around 30% year-over-year AWS growth in the current quarter, with potential further acceleration in 2026 as AI workloads scale. That would mark a sharp re-acceleration after several years of decelerating cloud growth across the sector and would likely be well received by investors comparing Amazon to peers such as Apple and other mega-cap tech names in the S&P 500 and NASDAQ 100.

Beyond pure cloud services, chips sold through AWS have already surpassed $20 billion in revenue with triple-digit growth. CEO Andy Jassy has signaled openness to selling Amazon’s Trainium chips to third parties more broadly, creating another lever for monetizing the AI infrastructure underpinning the Amazon Anthropic Deal.

How are analysts valuing Amazon’s AI pivot?

Analysts are turning increasingly bullish on Amazon’s overall setup heading into earnings. Bank of America recently lifted its price target on Amazon shares to $298 and reiterated a Buy rating, expecting Q1 revenue to beat consensus. The bank is modeling about $21.4 billion in EBITDA, modestly above Wall Street estimates near $20.7 billion, and sees upside surprise potential driven primarily by AWS.

KeyBanc’s Justin Patterson also rates the stock a Buy, with a price target of $325, emphasizing that the story this quarter is AWS, not the retail segment. He points to AI-related demand, Anthropic’s commitments and strong data points from semiconductor suppliers such as Taiwan Semiconductor as confirmation that hyperscalers’ infrastructure spending cycle is still in the early innings.

At the same time, Amazon’s own stake in Anthropic has ballooned in value. At the end of last year, Amazon held $45.8 billion in convertible notes and $14.8 billion in nonvoting preferred stock in Anthropic, for a total stake valued at about $60.6 billion. With Anthropic’s latest funding round marking a $380 billion valuation — and reported investor interest near $800 billion — the equity and convertible exposure embedded in the Amazon Anthropic Deal could become a strategically important asset on Amazon’s balance sheet.

Where does this leave Amazon versus other AI giants?

On the competitive front, Amazon is racing to keep pace with hyperscaler peers that are also investing aggressively in AI models and custom chips. Alphabet, for example, is pushing its own TPUs and has partnered with Marvell to scale its AI chip ambitions, directly challenging NVIDIA’s dominance and reshaping cloud economics. Meanwhile, OpenAI and Microsoft continue to deepen their integration, creating a rival ecosystem to Anthropic and Amazon’s Claude-Trainium stack.

Within the consumer and commerce ecosystem, Amazon is also rolling out AI-native features such as the shopping assistant Rufus and an upgraded Alexa Plus, which could eventually turn AI into a top-line growth driver for the core retail business. Analysts expect cost efficiencies from AI-driven automation across logistics and workforce optimization as well, as management reevaluates roles in light of emerging AI tools and humanoid robotics.

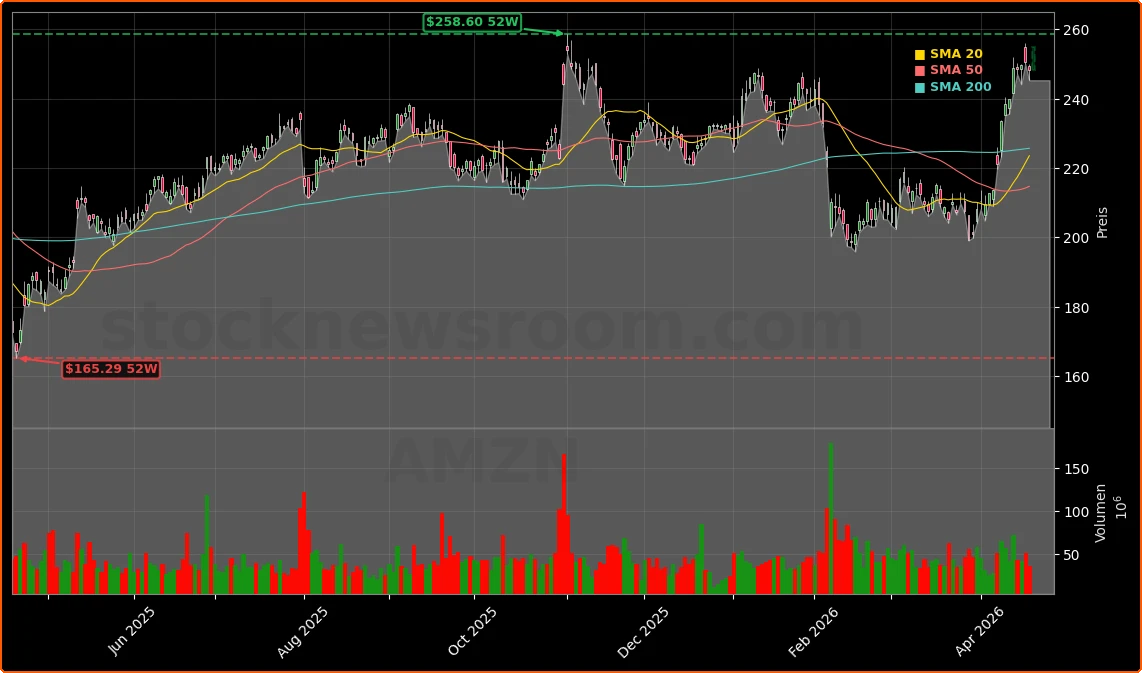

Despite being the laggard among the so-called “Magnificent 7” last year, Amazon shares have staged a strong rebound in 2026 and now trade not far from their 52-week highs, though still below any true all-time price records. Investors are betting that AWS’s renewed growth, supported by the Amazon Anthropic Deal and rising chip revenue, can justify a re-rating closer to faster-growing cloud and AI peers.

Related coverage: what else should investors watch?

For a broader view of Amazon’s infrastructure ambitions beyond cloud AI, investors can read how the company is moving into space-based connectivity in “Amazon Globalstar Acquisition: $11.6 Billion Bet to Close the Gap With Starlink”, which examines the strategic logic of combining Globalstar’s satellite assets with Amazon’s customer reach. The deal ties into Project Kuiper and could complement the AI build-out by improving global network coverage.

To understand the competitive AI-chip backdrop, it’s also worth looking at Alphabet’s strategy in “Alphabet AI Chips Boom: Custom TPUs and Marvell Deal Shake Up Nvidia”, which details how Alphabet’s custom TPU efforts and its partnership with Marvell might erode NVIDIA’s pricing power and influence cloud cost structures. Together, these pieces show how hyperscalers are vertically integrating from satellites to silicon to defend margins in the AI era.

Anthropic’s commitment to run its large language models on AWS Trainium for the next decade reflects the progress we’ve made together on custom silicon.— Andy Jassy, CEO of Amazon.com, Inc.

The Amazon Anthropic Deal underlines how aggressively Amazon is leaning into generative AI, from multi-billion-dollar equity stakes to long-term cloud and chip commitments. For investors, the key questions now are whether AWS can deliver the anticipated 30% growth inflection and how much incremental value Amazon can capture from Anthropic’s success. The upcoming Q1 earnings and 2026 guidance will be pivotal in confirming whether this AI-heavy strategy can sustain Amazon’s newfound momentum in the S&P 500 and NASDAQ over the next leg of the cycle.