Can AMC Forecast optimism finally outrun debt fears, or is this rally already too close to the new price target?

What Does Macquarie’s AMC Forecast Upgrade Mean for Investors?

Macquarie analyst Chad Beynon maintained a Neutral rating on AMC Entertainment Holdings, Inc. but raised the price target to $2.00 from $1.50 — a decisive vote of confidence in near-term operational stabilization. The firm upgraded its 2026 adjusted EBITDA estimate to $629 million (up from $600 million) and narrowed its full-year adjusted loss forecast to 24 cents per share from 28 cents. That revised AMC Forecast reflects stronger concession attach rates, improved occupancy trends, and disciplined cost management across AMC’s 780-theater footprint. While still Neutral, the move contrasts with more bearish stances from peers like Citigroup and RBC Capital Markets — both of which retain Underperform ratings on the stock amid lingering debt concerns.

How Strong Is the Box Office Recovery Behind This AMC Forecast?

Macquarie’s AMC Forecast rests on concrete box office data: U.S. second-quarter admissions revenue hit $2.97 billion — up 11% year-over-year and the strongest Q2 in six years. Major releases like The Super Mario Galaxy Movie, Michael, and Toy Story 5 drove traffic, while surprise hits Obsession and Backrooms extended holdover demand. The firm now forecasts the full-year domestic box office at $9.8 billion — a 13% increase over 2025 — a critical tailwind for AMC’s high-margin concession sales, which contribute over 40% of gross profit. That recovery outpaces broader consumer discretionary trends, with the S&P 500 Consumer Discretionary Index up only 5.2% YTD — underscoring AMC’s relative operational inflection.

Is AMC Forecast Still Constrained by Debt and Competition?

Yes — and Macquarie explicitly flags rising labor and utility costs as near-term risks. While AMC’s $200 million debt offering in late June (detailed in its recent AMC Offering +2.5% as $200M Raise Reshapes Debt Outlook) improved near-term liquidity, the company still carries $3.1 billion in long-term debt. Competitors like Cinemark and Regal remain capacity-constrained, but streaming giants continue pressuring long-term demand. Notably, Netflix Merger +5% as Sports Push Replaces M&A Buzz highlights how media consolidation is shifting capital away from linear exhibition — a structural headwind Macquarie’s AMC Forecast doesn’t fully offset. Still, AMC’s 2026 EBITDA upgrade implies margin expansion is achievable even amid this pressure.

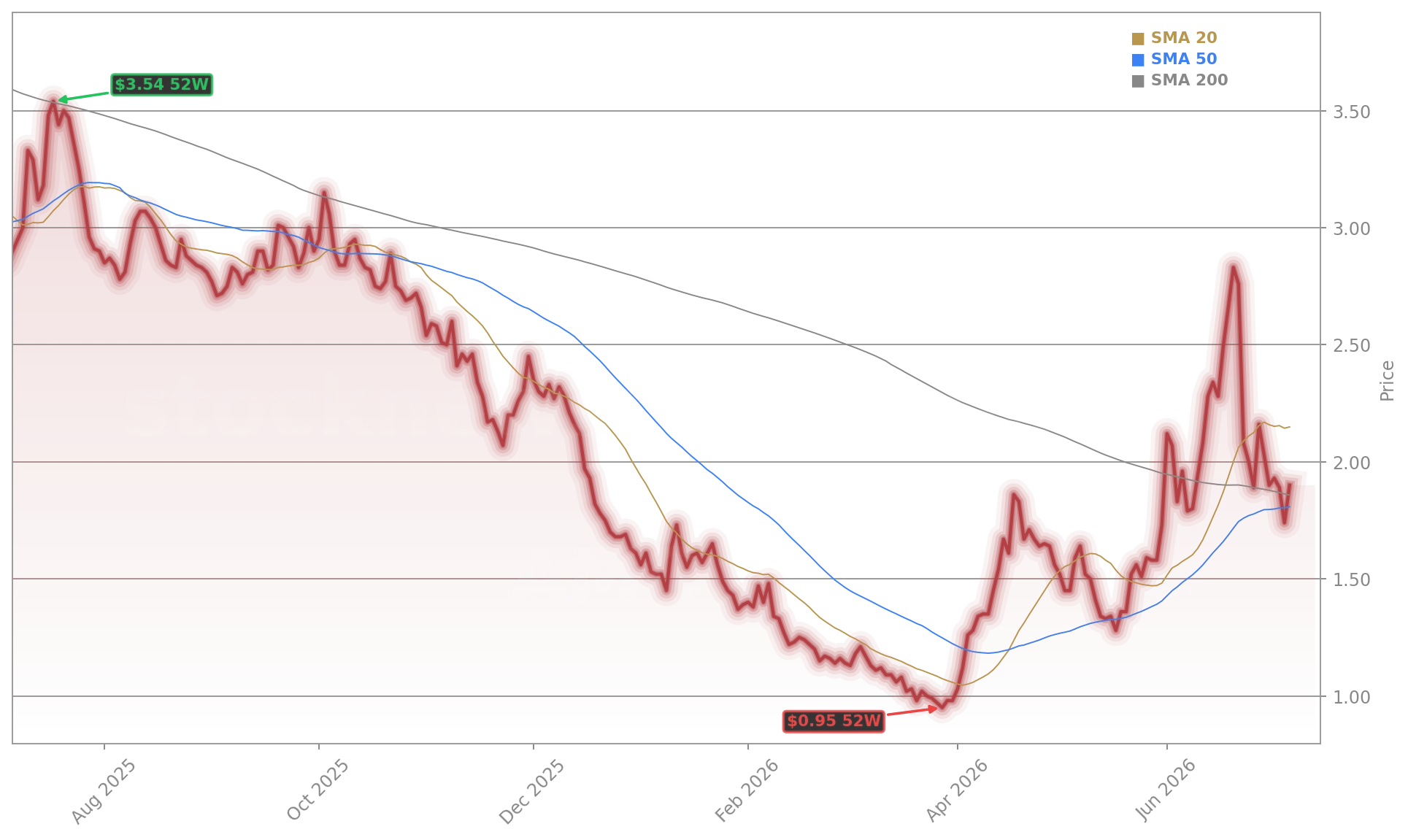

What Do Technicals Say About This AMC Forecast Rally?

AMC shares are trading at $1.95 — just 2.5% below Macquarie’s $2.00 target and 6.9% above the 50-day simple moving average. The RSI sits at 48.82, confirming a healthy, non-overbought bounce — not a speculative blowoff. However, the 20-day SMA at $1.99 creates immediate resistance, and the stock remains 33.1% lower over the past 12 months. That context matters: this AMC Forecast isn’t signaling a full bear-market reversal, but rather a tactical inflection point ahead of the critical August–October corridor, when Deadpool & Wolverine and Wicked: Part Two hit theaters. For NASDAQ investors holding volatile growth names like Tesla, AMC’s rebound offers a rare low-beta exposure to live entertainment recovery.

How Does This AMC Forecast Compare to Broader Market Sentiment?

The box office rebound is real, durable, and flowing directly to AMC’s bottom line — especially in concessions and operating leverage.— Chad Beynon, Macquarie analyst

Wall Street remains split. While Macquarie’s AMC Forecast upgrade is timely, Goldman Sachs maintains its Sell rating, citing “unresolved liquidity risk” and “limited path to investment-grade credit metrics.” Morgan Stanley recently downgraded the sector to Underweight, citing streaming substitution and advertising softness. Yet AMC’s 13.4% intraday gain — outpacing the S&P 500’s 0.3% move — suggests momentum traders are pivoting toward value-driven cyclicals. With the NASDAQ down 2.1% YTD and NVIDIA shares flat over the past month, AMC’s rally reflects a broader rotation into beaten-down, event-driven equities. That makes this AMC Forecast not just about theaters — but about where capital flows next.