Has the Netflix Merger story finally died, and could live sports be the real catalyst behind the stock’s next move?

Did Netflix Merger Rumors Just Vanish?

Yes — and decisively. Reports suggesting Netflix was preparing a bid for NBCUniversal collapsed this week after Comcast CEO Brian Roberts publicly ruled out any sale, citing the need for NBCUniversal to operate independently for at least one year to preserve tax-free spinoff status. Analyst Craig Moffett of MoffettNathanson dismissed the speculation as baseless, noting that vertical consolidation in streaming has historically created value destruction, not synergy. This clarity removed a major overhang: Netflix shares rose sharply on Thursday, outperforming the Nasdaq-100, which fell over 2%. The move reflects investor relief — and a broader recognition that Netflix’s long-term value lies not in mega-acquisitions, but in scaling its global platform, deepening ad-tech infrastructure, and locking in exclusive live content. The Netflix Merger distraction is officially over.

What’s Driving Netflix’s Live-Sports Bet?

Netflix is betting big on live sports to counter subscription fatigue and boost retention. The company secured five NFL games for the 2026 season, added WWE’s flagship programming, and is positioning for a high-profile Floyd Mayweather–Manny Pacquiao rematch — though that stream faces legal challenges. Unlike traditional broadcasters, Netflix treats sports as a ‘sticky’ engagement engine, not a standalone profit center. With over 300 million subscribers globally and limited exposure to China, the platform offers unparalleled scale for live-event distribution. This strategy also aligns with a broader market rotation: as Information Technology now represents a record 39% of the S&P 500, investors are seeking durable attention assets — and live sports deliver recurring, appointment-based viewing that on-demand libraries cannot replicate. Competitors like Meta and Apple remain focused on hardware and AI ecosystems, leaving Netflix with a unique window to own premium live entertainment.

How Strong Are Netflix’s Q2 2026 Earnings Prospects?

Netflix reports Q2 results on July 16, 2026 — and Wall Street expects acceleration. Analysts forecast $12.58 billion in revenue (up 13.5% year-over-year) and $0.79 in EPS (up 9.7% YoY). The ad-supported tier, launched in 2022, now accounts for over 35% of new subscriber growth, and management has signaled aggressive investment in ad-tech partnerships to expand yield per impression. Valuation remains reasonable at a forward P/E of 23.9x — well below peers like NVIDIA and Tesla. Price targets reflect strong conviction: BofA Securities maintains a $125.00 target with a Buy rating, Guggenheim holds $120.00, and Piper Sandler recently raised its target to $115.00. The consensus Buy rating and $113.36 average target imply 45% upside from current levels.

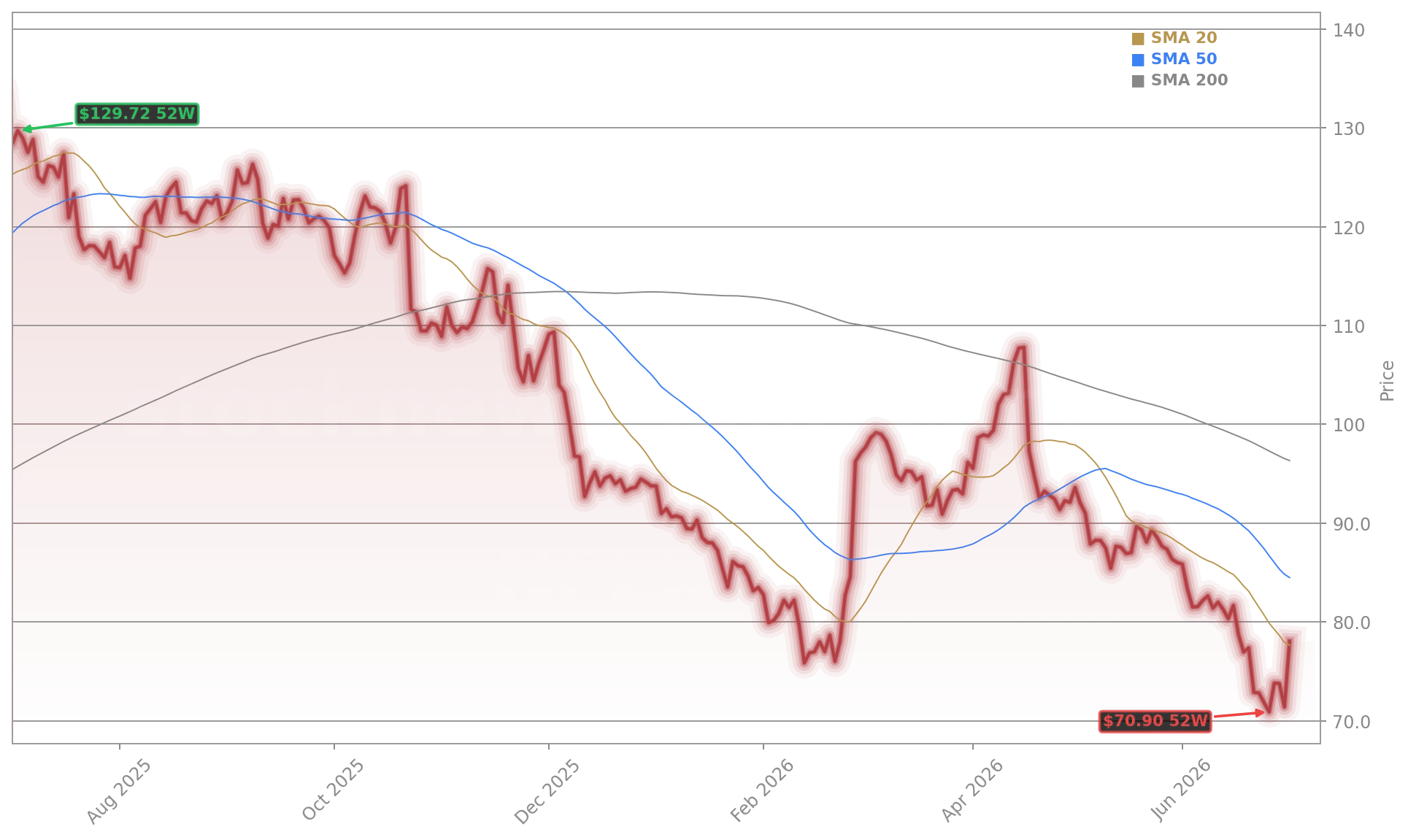

Is Netflix’s Technical Setup Improving?

Yes — but cautiously. At $77.83, Netflix remains 7.2% below its 50-day moving average ($84.13) and 18.7% below its 200-day SMA ($96.11), signaling the longer-term downtrend is intact. However, Thursday’s volume surge and RSI reading of 48.46 suggest the bounce is not yet overextended. Key resistance sits at $91.50 — the threshold for reclaiming the 50-day — while $71.00 remains critical support, just above the June 52-week low of $70.86. Benzinga Edge scores highlight Netflix’s strength in Quality (92.22) and Growth (89.74), but weakness in Momentum (5.38) and Value (20.71) confirms the rally needs follow-through to be sustainable. For long-term investors, the technicals matter less than execution — and Q2 will be the first major test of the live-sports and ad-tier thesis.

What Do Hedge Funds See in Netflix Today?

Netflix’s decision to walk away from the transaction reinforced its disciplined approach to capital allocation and reduced concerns around leverage and integration risk.— Brown Advisory, Q1 2026 Investor Letter

Netflix remains a core holding for institutional investors: 144 hedge fund portfolios held the stock at the end of Q1 2026, per Brown Advisory’s investor letter. That’s down only slightly from 146 in Q4 2025 — a sign of stability amid volatility. Brown Advisory noted Netflix outperformed during the quarter as concerns over a potential acquisition of Warner Bros. Discovery subsided, reinforcing management’s disciplined capital allocation. The firm emphasized strong engagement metrics and improving monetization — not M&A — as the real drivers. While hedge funds acknowledge AI stocks like Apple may offer higher short-term upside, Netflix’s quality profile and global scale make it a durable anchor in growth portfolios, especially as market leadership broadens beyond the megacap tech cohort.