Is the Netflix Rebound the start of a real trend change, or just a sharp bounce from a deeply oversold level?

Is Netflix Rebound a Technical Signal or Just Relief?

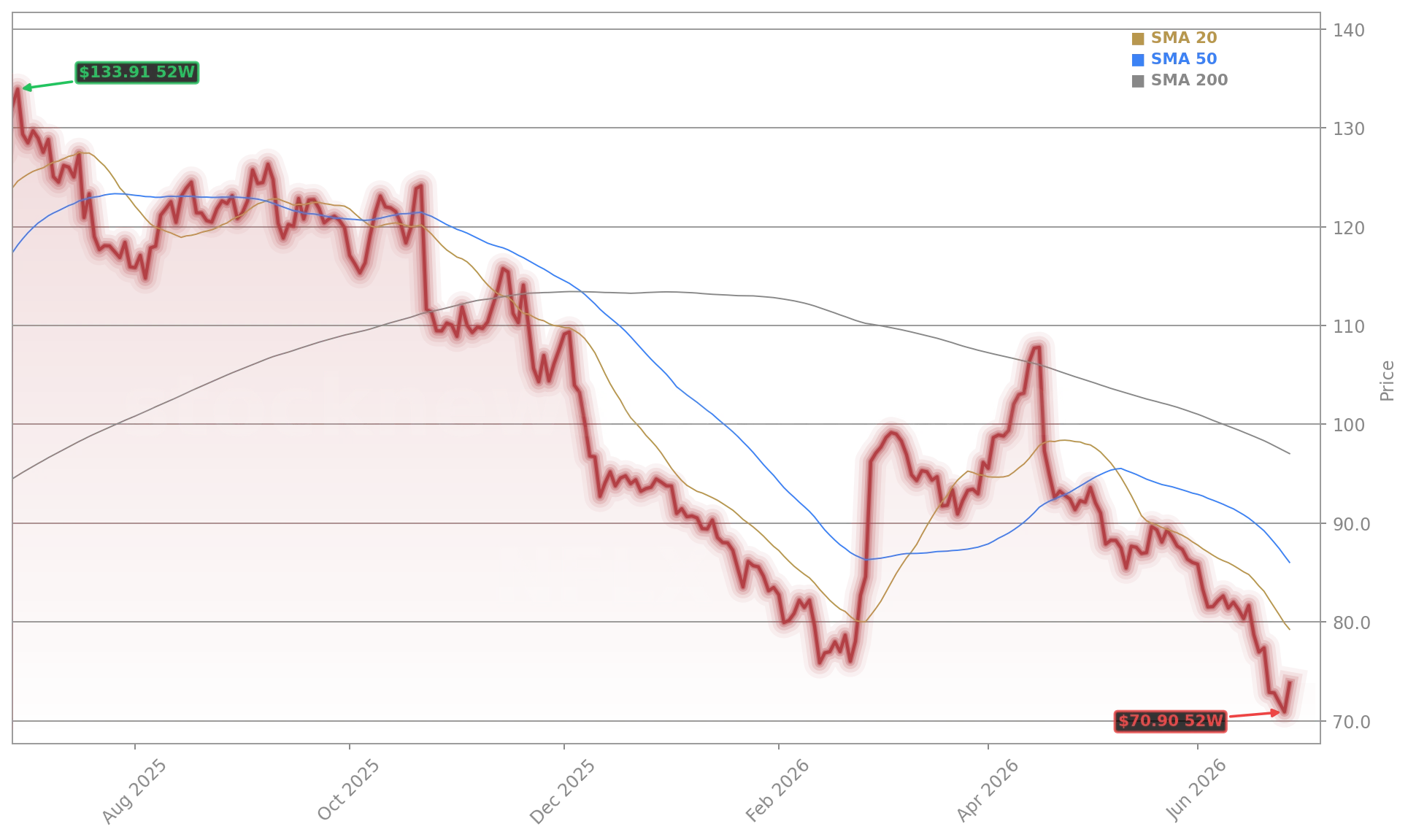

Netflix shares rallied decisively from the $70.90 intraday low — a level that aligned precisely with the 200-week moving average, a historically strong support zone. The bounce wasn’t random: volume spiked, and the stock ranked eighth most active in the S&P 500 and ninth in the Nasdaq 100. Traders noted a textbook ‘V-rejection’ — with price rejecting the $70 zone and climbing nearly $4 in under two hours. While short-term momentum is now bullish, the broader context remains challenging: Netflix is still down 20.2% month-to-date and 44.2% year-to-date. That puts it in bear market territory alongside peers like Coinbase, ServiceNow, and Oracle, all of which have shed over 40% from recent highs. Unlike those firms, however, Netflix’s core business remains profitable and growing — raising the stakes for whether this Netflix Rebound reflects renewed confidence in its content flywheel or simply short-covering.

What’s Driving the Netflix Rebound?

Three converging forces catalyzed Friday’s move. First, the stock had become oversold — hitting its lowest level in 20 months, with valuation compressed to just 18x forward earnings, well below its five-year median of 32x. Second, competitive fears around engagement and subscription saturation appear temporarily priced in, especially after rival streaming services reported weaker Q2 subscriber growth than expected. Third, Wall Street is quietly recalibrating: Citigroup lifted its price target to $82 last week, citing improved international ad-tier monetization and stable churn. RBC Capital Markets upgraded Netflix to ‘Outperform’, calling the current valuation ‘unjustifiably punitive’ given 12% year-over-year revenue growth and 22% operating margin. Notably, Netflix’s rebound occurred while Meta and Apple traded flat — suggesting this isn’t just broad tech momentum, but stock-specific re-rating.

How Does Netflix Compare to Broader Tech?

Netflix’s 44.2% decline from its June 2025 peak places it fifth-worst among major tech names — behind only Coinbase (-67%), Oracle (-57%), ServiceNow (-55%), and Palantir (-46%). Yet its fundamentals diverge sharply: unlike those firms, Netflix carries zero net debt, generated $2.1 billion in free cash flow in Q1 2026, and added 5.2 million paid subscribers globally — beating consensus by 0.8 million. That contrast explains why Goldman Sachs recently added Netflix to its ‘Conviction Buy List’, citing ‘asymmetric upside’ if engagement metrics stabilize. Meanwhile, the Nasdaq 100 is down 7.3% in Q2 2026, dragging down mega-caps like NVIDIA and Tesla, but Netflix’s relative strength — up 5.5% on the day while the index rose just 0.8% — suggests investors are rotating into high-quality, cash-generative names trading at distressed valuations.

Netflix Rebound: What’s Next for Investors?

Technical analysts point to $77.40 — Netflix’s June 18 close — as the immediate resistance level. A sustained break above that would confirm the Netflix Rebound as more than a bounce and open the path toward $85. But the real test comes in Q2 2026 earnings, due July 18: investors will scrutinize ad-tier penetration (now at 31% of total subscribers), cost-per-subscriber trends, and international operating margin expansion. If guidance holds, the Netflix Rebound could accelerate — especially with rival Take-Two Interactive (TTWO) gaining investor attention ahead of its GTA VI launch, highlighting how premium content franchises remain in high demand. For U.S. portfolios, Netflix offers a rare blend of growth, profitability, and valuation margin — but only if the rebound proves durable beyond next week’s follow-through.

Netflix’s current valuation is unjustifiably punitive given its free cash flow generation, subscriber growth, and margin profile.— RBC Capital Markets

Related coverage: Netflix Merger -5.9%: Stock Sinks on M&A Shock and Ad Hopes explores whether recent M&A speculation reflects strategic urgency or overreaction. Meanwhile, Take-Two GTA VI Launch: Why $8.2B Is Driving Bullish TTWO Calls underscores the broader market’s renewed focus on scalable, high-margin entertainment IP — a dynamic that benefits Netflix’s content advantage.