Is the Netflix Merger story a hidden opportunity for investors, or a warning that growth now depends on deals that never arrive?

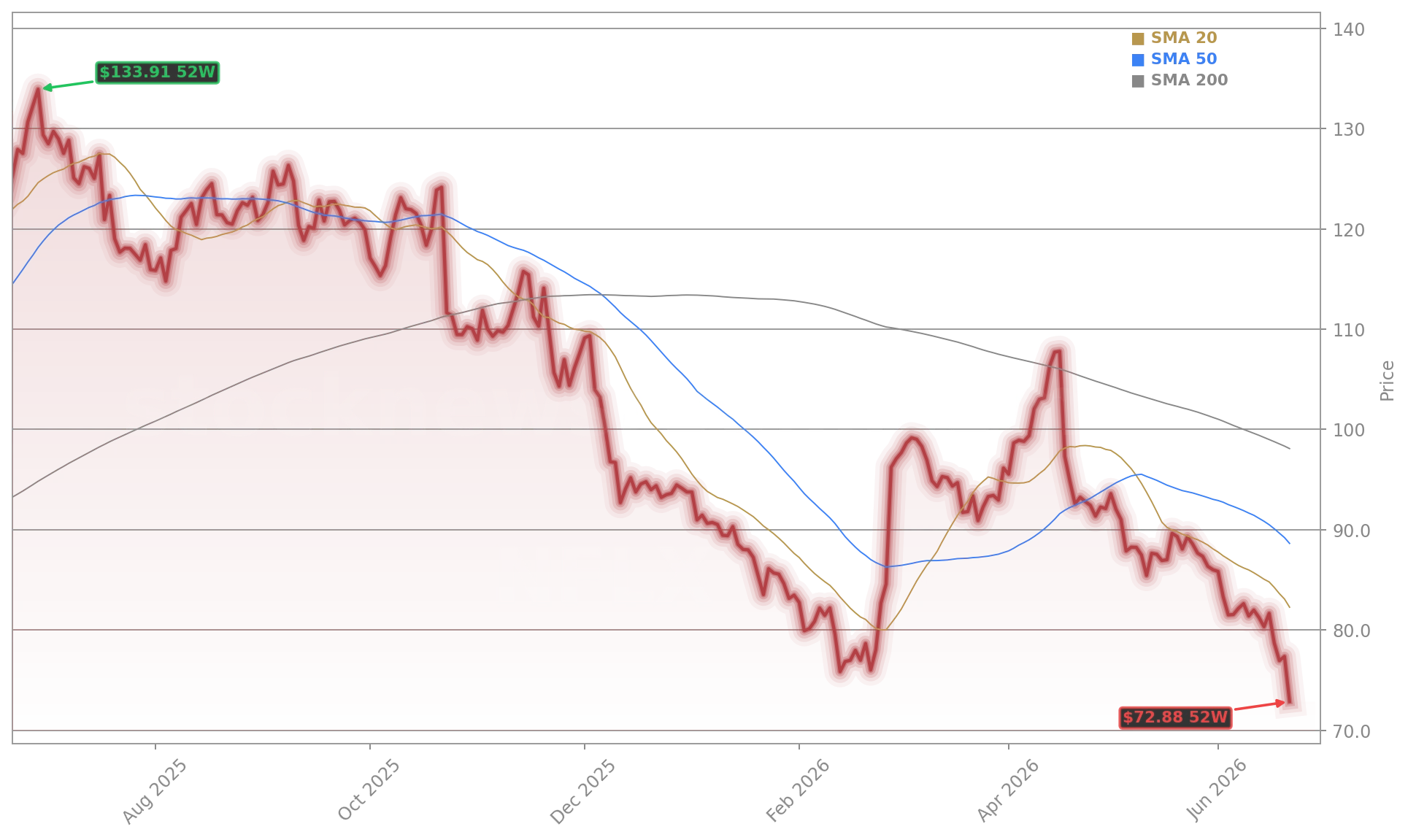

Why Did Netflix Hit a 52-Week Low?

Netflix closed Monday at $72.84—the lowest level since October 2024 and just $2.17 above its $75.01 52-week low. The drop follows a 17.5% year-to-date decline and a 36.7% slide over the past 12 months. The selloff accelerated after reports surfaced that Netflix lost a $22 billion bidding war for Roku to Fox Corp—then denied interest in Lionsgate Studios, sending the stock down 3.6% on June 16. Bank of America downgraded Netflix from ‘Buy’ to ‘Hold’ on June 15, citing valuation concerns and limited near-term catalysts. Erste Group had already cut its rating in April. Despite 37 ‘Buy’ and 13 ‘Hold’ ratings from analysts, the consensus price target stands at $114.15—implying 56% upside if fundamentals hold.

What’s Behind the Netflix Merger Speculation?

Netflix Merger chatter stems from three high-profile pursuits: Warner Bros. Discovery (WBD), Roku, and Lionsgate Studios. While Netflix walked away from WBD after Paramount Skydance’s $111 billion offer, it collected a $2.8 billion termination fee—funding accelerated buybacks and studio expansion. The Roku bid, reportedly outmatched by Fox’s $160-per-share offer, exposed Netflix’s growing need for first-party ad data and distribution control. Meanwhile, the Lionsgate rumor—quickly denied—highlighted investor anxiety over Netflix’s lack of a legacy film library, unlike Apple, Disney, and Comcast. Ted Sarandos, Netflix co-CEO, acknowledged on the Q1 call that pursuing WBD helped ‘build our M&A muscle,’ but stressed the company remains ‘very disciplined’—a stance echoed by Citizens analyst Matthew Condon, who reiterated a ‘Market Perform’ rating citing ‘softer engagement assumptions.’

Is Netflix’s Ad Business Enough to Offset M&A Setbacks?

Yes—according to the numbers. Ad revenue is projected to double to $3 billion in 2026, with advertiser count up 70% year over year to over 4,000. The ad-supported tier now drives more than 60% of new sign-ups in markets where it’s available. With 325 million+ paid memberships and only 45% penetration of its 800 million addressable smart-TV households, Netflix’s ad scalability remains underleveraged. Futurum Equities’ Shay Boloor called the current valuation ‘the cheapest in four years,’ noting Netflix trades at just 24x forward P/E—on par with the S&P 500—despite 16% YoY revenue growth and a 31.5% targeted operating margin. Free cash flow guidance was raised to $12.5 billion, and Q1 buybacks totaled $1.3 billion.

How Do Competitors Compare on Wall Street?

While Netflix struggles with perception, peers like Meta and NVIDIA benefit from AI-driven narratives and stronger ad-tech integration. Meta’s Instagram for TV expansion on Samsung devices directly competes for living-room attention, per M Science. YouTube remains Netflix’s largest TV-viewing competitor, consistently ranking higher in U.S. screen time. Meanwhile, Tesla and Apple dominate the Nasdaq-100’s AI infrastructure theme—where Netflix is now the smallest top-10 holding at 1.2% weight. Analysts at RBC Capital Markets see Netflix’s valuation disconnect as a near-term opportunity, while Citigroup maintains a $120 price target, citing ‘robust pricing power and margin resilience.’ The stock’s 1.49 beta amplifies broader market swings—especially as the S&P 500 surges 9.5% YTD while Netflix lags.

What’s Next for Netflix Investors?

Q2 2026 earnings on July 16 will be the ultimate stress test. Netflix guided for $12.57 billion in revenue—below the $12.64 billion Wall Street consensus—and $0.78 EPS versus $0.84 expected. Content amortization is expected to peak in Q2 before easing in H2. If the ad business delivers and margins hold near 32.6%, the Netflix Merger narrative may shift from ‘frustrated acquirer’ to ‘disciplined compounder.’ With $6.8 billion in buyback authorization remaining and a $400 million acquisition of Radford Studio Center in the works, Netflix is betting on organic scale—not forced consolidation.

Related coverage: Is Netflix chasing the wrong deals, or could the latest merger drama create a rare buying opportunity? Netflix Merger $22B Warning as Roku Loss Rattles Bulls. Can Alphabet’s massive AI backlog outweigh the shock of losing two of DeepMind’s most important researchers? Alphabet DeepMind Departures: -6% Warning for AI Bulls.

To me, that retention data is probably the most important data point… Netflix raised prices, and retention improved anyway. That is real pricing power to me.— Shay Boloor, Futurum Equities

Netflix Merger pressure is real—but so is Netflix’s execution. The company remains a cash-generating powerhouse with a scalable ad model and unmatched global reach. For U.S. investors, this isn’t a turnaround story—it’s a valuation reset aligned with fundamentals. The next quarterly earnings will show whether the market rewards patience. Long-term investors should watch Q2 margins and ad revenue growth closely—and position accordingly.