Can AutoZone keep investors confident when profit beats estimates but revenue, margins, and international growth start raising tougher questions?

Why are AutoZone Earnings moving the stock?

AutoZone Earnings showed a familiar split for high-priced retail compounders: better-than-expected EPS, but a more complicated operating picture underneath. For the 12 weeks ended May 9, net sales rose 8.4% year over year to $4.84 billion, while net income climbed to $641.5 million from $608.4 million. Diluted EPS reached $38.07, ahead of the roughly $36.18 Wall Street consensus carried by AP and other market trackers. Revenue, however, missed forecasts near $4.86 billion, and investors quickly punished the shares.

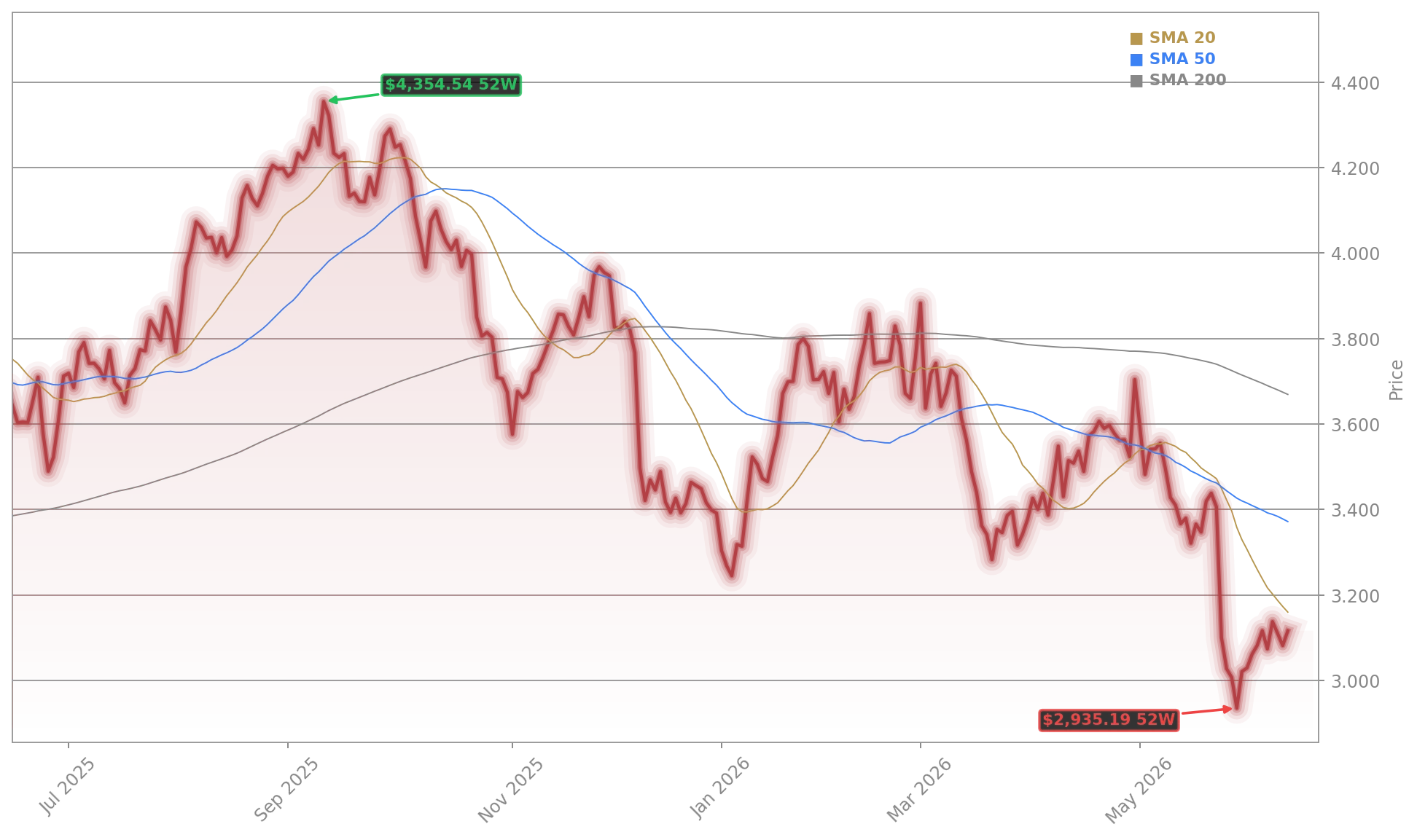

That reaction has been severe. AutoZone stock was down 8.99% intraday at $3,100.29, far below the prior close of $3,433.15. The move suggests the market is looking past the headline earnings beat and focusing instead on sales quality, margin compression, and whether the company can sustain its premium valuation if top-line momentum cools.

Can AutoZone offset pressure with domestic demand?

Domestic trends were still solid. Same-store sales in the U.S. increased 4.1%, supported by both do-it-yourself and commercial customers. Total company same-store sales rose 3.9% in constant currency, while reported international same-store growth was 16.6%, dropping to just 1.6% in constant currency. That gap matters because it highlights how much foreign exchange helped headline growth.

Chief Executive Phil Daniele said Mexico and Brazil performed similarly to last quarter and remained below plan, even as the company believes it is still taking share in those markets. Investors appear unconvinced for now. The international business has been part of the long-term growth narrative, so weak constant-currency traction there likely carried outsized weight in Tuesday’s selloff. In a market that has rewarded operational consistency at companies like Apple and NVIDIA, even a modest revenue miss can trigger a sharper reset when expectations are high.

What do margins say about AutoZone?

Margins were mixed. Gross profit as a percentage of sales was 52.2%, down 57 basis points from a year ago. Management attributed the decline primarily to a 77-basis-point non-cash LIFO impact, partly offset by other gross margin improvements. Operating expenses improved slightly to 33.1% of sales from 33.3%, helping operating profit rise 6.6% to $923.8 million.

Still, margin compression is exactly what some bearish commentary highlighted after the release. Investors are also watching return on invested capital more closely as the company expands its footprint and keeps repurchasing stock aggressively. AutoZone bought back 164,000 shares during the quarter for $586.3 million, paying an average of $3,582 per share. About $0.8 billion remains under the current authorization. Buybacks continue to support per-share earnings, but they do not fully offset concern when revenue growth or store productivity appears less robust.

How does AutoZone compare on outlook?

AutoZone Earnings also included continued expansion. The company opened 82 stores in the quarter, including 57 in the U.S., 20 in Mexico, and five in Brazil, bringing total locations to 7,856. Management still expects to open roughly 355 to 365 stores this fiscal year. Inventory increased 10.8% from a year earlier, driven by growth initiatives and inflation, while net inventory per store remained negative, a long-standing efficiency marker for the chain.

I want to thank our AutoZoners across the globe for delivering on our promise of WOW customer service and strong financial results this past quarter.— Phil Daniele

For investors comparing the name with other consumer and retail compounders such as Tesla or industrial leaders like United Rentals, the message is clear: execution remains strong, but the bar is higher than just beating EPS. MarketBeat data published ahead of the report showed Wall Street’s broader analyst consensus at Moderate Buy, with an average target around $4,290.91, though the latest quarterly print may test those assumptions if international growth does not accelerate. AutoZone Earnings reaffirm the chain’s profitability and buyback discipline, but the next report will need cleaner revenue momentum and firmer overseas execution to rebuild confidence.