Can Chipotle keep investors satisfied if digital growth rises but margins and traffic keep moving the wrong way?

What’s Driving Chipotle Earnings Expectations?

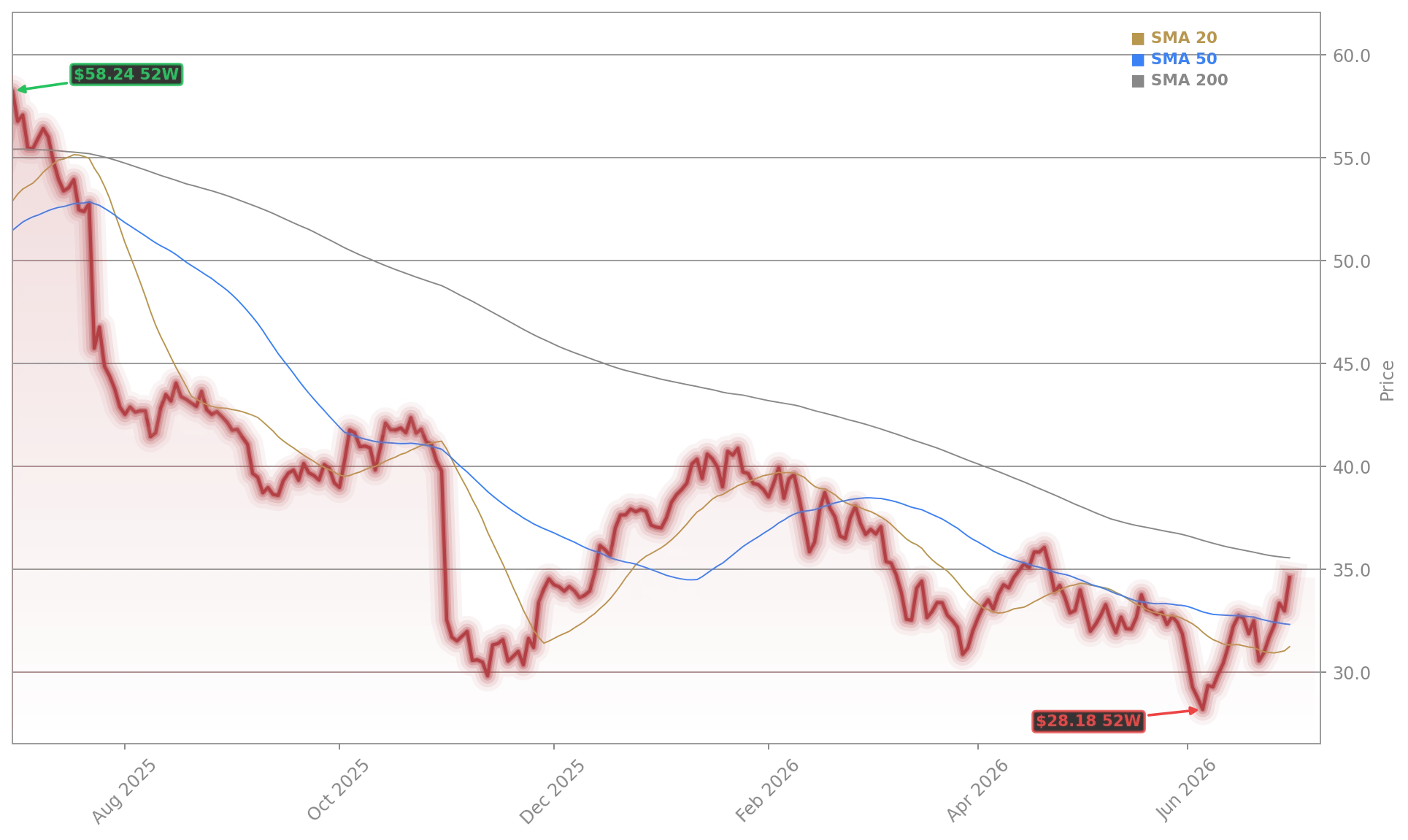

Analysts at Barchart.com project Chipotle Mexican Grill, Inc. will report Q2 EPS of $0.32—down 3% year-over-year—despite revenue growth, citing persistent labor and food cost inflation. The company’s 26.1% labor cost ratio in Q1 (up from 25% in 2025) signals margin pressure that’s unlikely to ease before fall. While TIKR.com maintains a $43 price target—implying 29% upside from the current $34.57—their bullish case hinges on EBITDA reacceleration by March 2027, not near-term Chipotle Earnings surprises.

How Is Traffic Growth Really Holding Up?

Chipotle Mexican Grill, Inc. reported just 0.5% comparable restaurant sales growth in Q1—its weakest in over a decade. That follows a 2.5% decline in 2025, a sharp reversal from 8.4% growth in 2023. Management now expects flat comp sales for full-year 2026, a stark pivot from its historic double-digit growth narrative. The slowdown coincides with the August 2024 departure of CEO Brian Niccol—now driving 6.2% comp growth at Starbucks. With customers trading down amid elevated inflation, Chipotle’s premium positioning is under renewed scrutiny, especially as rivals like McDonald’s and Wendy’s lean into value menus and drive-thru efficiency.

Can Digital Sales Offset Store-Level Weakness?

Digital remains Chipotle Mexican Grill, Inc.’s strongest lever: $1.2 billion in Q1 digital sales represented 38.3% of total revenue, per AlphaStreet. That’s up from 35% in Q4 2025, and the company’s loyalty program now boasts over 32 million active members. Yet digital growth hasn’t translated to higher average order values or frequency—key drivers of comp sales. Meanwhile, new restaurant openings continue at pace (200+ planned for 2026), but underperforming units are compressing margins. As Simply Wall Street notes, Chipotle’s DCF model values the stock at $30.49—$4.08 below current levels—highlighting valuation risk if Chipotle Earnings miss on profitability.

What Do Analysts Say About the Road Ahead?

Citigroup maintains a ‘Buy’ rating with a $45 target, citing ‘disciplined unit economics and unmatched throughput capacity.’ RBC Capital Markets rates Chipotle Mexican Grill, Inc. ‘Outperform’ but warns that ‘labor inflation and wage mandates in key states could delay margin recovery until late 2027.’ Morgan Stanley recently downgraded its margin outlook, noting ‘new-store payback periods have extended by 6–9 months versus 2023.’ The divergence underscores how much hinges on Chipotle Earnings: one more quarter of decelerating comps could trigger broader sector skepticism, especially as the NASDAQ’s consumer discretionary index trades near all-time highs.

How Does Chipotle Compare to Tech-Driven Peers?

Unlike Apple or NVIDIA, whose earnings momentum is fueled by AI infrastructure and ecosystem lock-in, Chipotle Mexican Grill, Inc. lacks a scalable technology moat. Its digital platform is robust—but replicable. Meanwhile, Tesla’s margin resilience amid EV demand softness offers a cautionary parallel: operational excellence alone can’t override macro headwinds. Chipotle’s 2026 focus on throughput, loyalty monetization, and gaming partnerships (e.g., Roblox integration) aims to build defensibility—but Wall Street remains anchored on quarterly Chipotle Earnings execution. With the S&P 500’s consumer discretionary sector up 12% YTD, underperformance by Chipotle Mexican Grill, Inc. could signal broader fast-casual fatigue.

Related Coverage: For deeper context on how rising costs are reshaping expectations, see Chipotle Earnings +2.9% Surge as Margins Get Squeezed. Investors also watching global tech momentum may find relevance in Alibaba AI Cloud +2.4% as China Tech Momentum Builds, which highlights how infrastructure plays are gaining traction amid shifting valuation regimes.

Digital sales are strong, but traffic is the foundation—and that foundation is cracking under inflationary pressure.— RBC Capital Markets analyst

Chipotle Mexican Grill, Inc. faces a defining moment: can it prove its growth story is evolving—not ending? Chipotle Earnings will reveal whether traffic softness is cyclical or structural. For U.S. investors, the stakes extend beyond one stock—Chipotle Mexican Grill, Inc. is a bellwether for premium fast-casual resilience in a high-inflation, low-discretionary-spend environment. The next quarterly report sets the tone for second-half positioning in consumer equities.