Did the CrowdStrike Stock Split just unlock a new wave of buying power for CRWD investors?

How Did the CrowdStrike Stock Split Change Trading Dynamics?

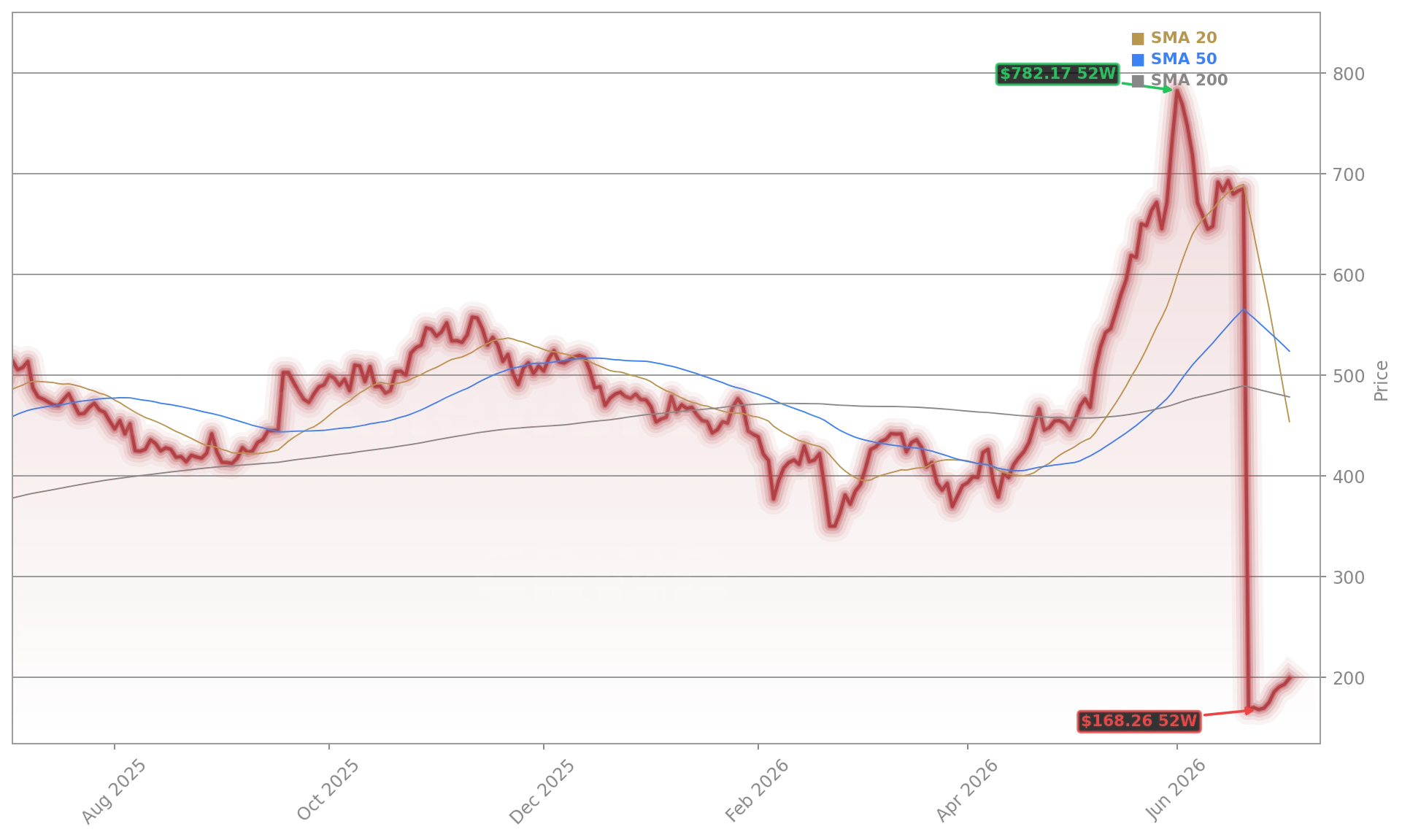

The 4-for-1 CrowdStrike Stock Split — executed on July 2, 2026 — reduced the nominal share price from ~$772 to ~$193, instantly lowering the cost of entry for retail investors and options traders. A standard 100-share lot now sits near $19,300, down from $77,200 — a tactical move that boosted intraday volume and liquidity. Crucially, the split did not alter fundamentals: market capitalization remains unchanged at $173 billion, and the company’s fiscal 2027 ARR midpoint target still stands at $4.2 billion. According to TechStock², the split has already increased options open interest by 22% week-over-week — signaling renewed institutional participation ahead of Q3 earnings.

Why Is CrowdStrike Leading the Cybersecurity Rally?

CRWD’s 5% gain Monday outpaced Palo Alto Networks (PANW), Okta (OKTA), and Fortinet (FTNT) — all up 3–4% — as the First Trust Nasdaq Cybersecurity ETF (CIBR) pushed toward its first record close in over a month. Analysts attribute the momentum to three converging catalysts: (1) the emergence of ‘Avalon,’ a new AI-orchestrated malware framework targeting crypto wallets and identity credentials; (2) CrowdStrike’s Falcon OverWatch AI detection suite gaining traction across Fortune 500 enterprises; and (3) Scotiabank’s recent upgrade of Okta to Outperform with a $165 price target — a sector-wide positive read-through. The rally reflects a broader rotation: while the iShares Semiconductor ETF (SOXX) remains down 8% in July, CIBR is up 14% since June 25 — underscoring cybersecurity’s role as a resilient AI infrastructure play.

What Do Valuation and Growth Signals Say?

CrowdStrike Holdings, Inc. trades at a premium — 30x its fiscal 2027 ARR midpoint — but growth remains robust. Revenue has surged from $874 million in FY2021 to $4.81 billion in FY2026, a 42% compound annual growth rate. Consensus estimates project 22% annual revenue growth through FY2029, driven by cloud migration, zero-trust adoption, and AI-powered endpoint protection. RBC Capital Markets recently reiterated its Outperform rating, citing “irreplaceable telemetry scale” and “Falcon Flex’s 92% net dollar retention.” Still, valuation concerns persist: Zacks Investment Research notes CRWD’s P/S ratio is nearly 3x the software industry median — a premium justified only if execution on AI-driven upsells remains flawless.

How Are Competitors and the Broader Tech Market Responding?

While CrowdStrike leads, the rally lifts the entire cybersecurity ecosystem — and signals strategic recalibration across tech. NVIDIA-driven AI infrastructure demand has spilled into security stacks, with Palo Alto Networks and Zscaler both up over 20% since late June. Meanwhile, the Texas Stock Exchange (TXSE) launched July 6 — adding competitive pressure to NYSE and NASDAQ — yet CrowdStrike Holdings, Inc. remains NASDAQ-listed and benefits from deep liquidity. Notably, the cybersecurity trade remains distinct from software’s AI disruption fears: the median CIBR component trades 27% below its all-time high, but CRWD is within 2% of its $207.77 52-week high — a sign of relative strength. Apple and Tesla remain benchmark tech names, but CRWD’s AI-native architecture positions it as a more direct beneficiary of real-time threat evolution than legacy hardware or consumer-focused peers.

What’s Next for CrowdStrike Investors?

With the CrowdStrike Stock Split now fully digested, attention shifts to Q3 2026 earnings — due in early September — and whether growth sustains at 22%+ pace. Technical indicators suggest near-term opportunity: the 14-day RSI at 19.9 signals oversold conditions, and the $193.19 post-split open aligns with strong support. CEO George Kurtz’s recent $1.94 million share sale — executed under a pre-arranged 10b5-1 plan — reflects routine portfolio management, not concern, given he retains over 2 million shares. As Citigroup analysts note, ‘CRWD remains the benchmark for AI-powered endpoint resilience — and that narrative is only strengthening.’

Related Coverage: For deeper analysis of CrowdStrike’s latest quarterly results, see CrowdStrike Earnings Show Record ARR and Fresh Bullish Calls, which details how the company’s $4.81 billion revenue and 92% net dollar retention are reshaping Wall Street’s valuation models. Also essential is Adobe Upgrade +4.9%: HSBC Turns Bullish on AI Fears, which explores how AI-driven security and identity management are converging across enterprise software — a trend directly benefiting CrowdStrike Holdings, Inc. and its peers.

CRWD remains the benchmark for AI-powered endpoint resilience — and that narrative is only strengthening.— Citigroup analysts

CrowdStrike Stock Split has successfully broadened ownership while preserving growth momentum. For U.S. investors, CRWD remains a core AI infrastructure holding with asymmetric upside in escalating cyber conflict. The next quarterly earnings will confirm whether the 22% growth thesis holds — and whether the CrowdStrike Stock Split has unlocked a new phase of institutional adoption.