Can Dell AI Infrastructure turn a massive AI backlog into lasting margin power, or is this surge already pricing in perfection?

What just turbocharged Dell’s AI infrastructure?

Dell Technologies Inc. surged 6.3% on Monday, June 22, after unveiling its next-generation Dell AI Factory — a turnkey supercomputing infrastructure built on the new PowerEdge XE8812 server and NVIDIA’s Rubin architecture. The system is designed for HPC-class AI training and inference, targeting both cloud providers and national AI initiatives. Unlike legacy server deployments, this AI Factory integrates networking, liquid cooling, and orchestration software — reducing time-to-ai from months to days. The announcement directly follows Q1 FY27 results, where AI-optimized server revenue exploded 757% year-over-year to $16.13 billion — now representing over 36% of total Infrastructure Solutions Group (ISG) revenue.

How does Dell AI Infrastructure compare to rivals?

While Super Micro Computer posted a 13.8% intraday jump on similar AI infrastructure momentum, Dell’s scale and integration depth set a new benchmark. Unlike Super Micro’s component-focused model, Dell’s AI Factory bundles full-stack support, firmware validation, and NVIDIA AI Enterprise software licensing — a model favored by Meta and Microsoft. NVIDIA remains the foundational enabler, but Dell’s margin expansion in ISG (10.5% in Q1, up from 9.7%) shows hardware OEMs can capture value beyond component assembly. By contrast, Hewlett Packard Enterprise and Tesla — which filed a ‘Megapod’ trademark last week — are still in early-stage infrastructure plays. Tesla’s move signals ambition, but Dell has shipped $24.4 billion in AI orders in one quarter alone.

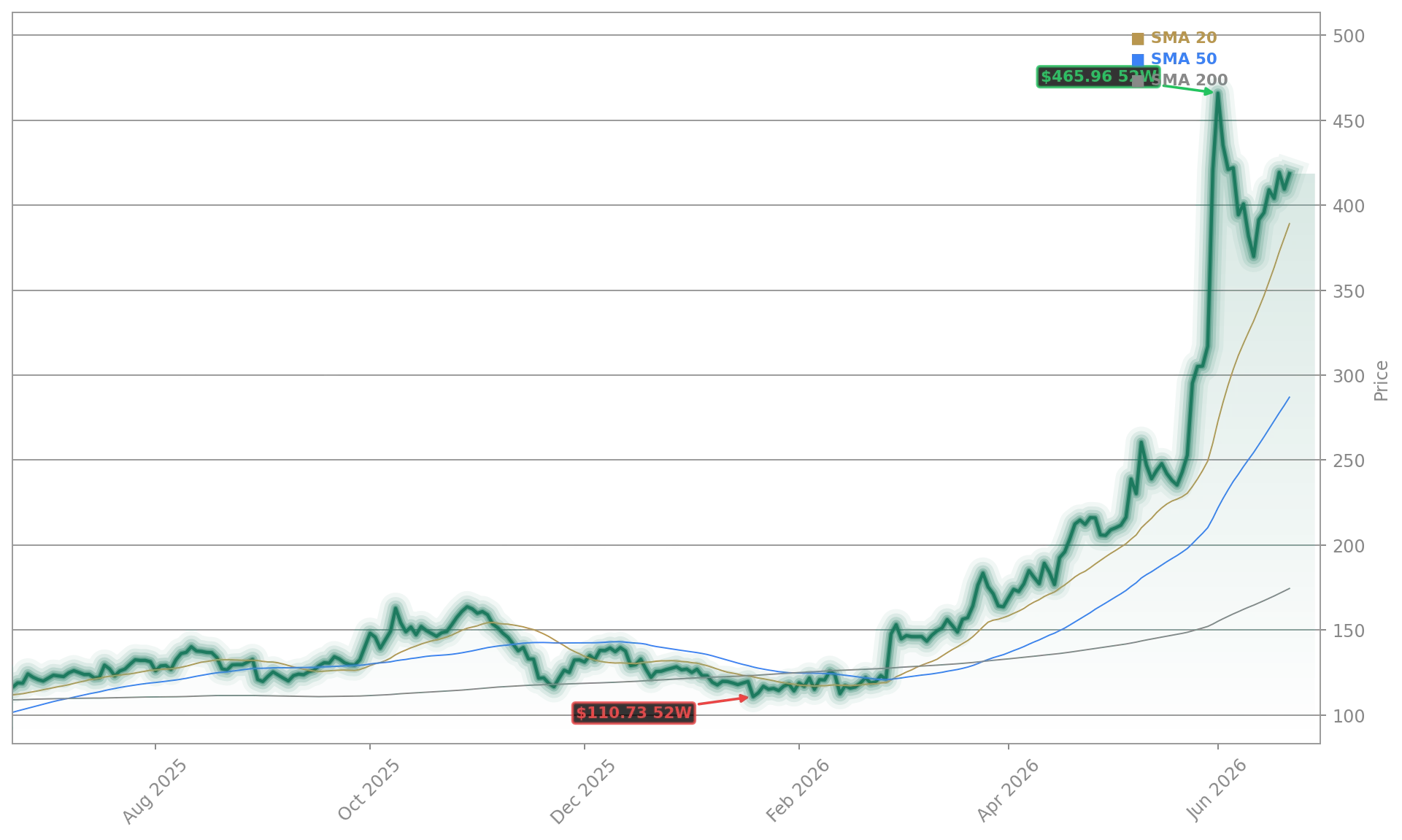

Why are analysts raising targets — not just ratings?

Truist raised its price target on Dell Technologies Inc. from $170 to $360 on June 1, citing ‘exceptionally strong demand and a tight supply environment.’ Citigroup followed on June 18 with a $495 price target and ‘Buy’ rating, emphasizing Dell’s ‘unmatched execution velocity in AI server fulfillment.’ Morgan Stanley upgraded to ‘Overweight’ with a $487 target, noting Dell’s AI backlog now exceeds $51 billion — more than double its total FY26 ISG revenue. Of 26 analysts covering the stock, 18 rate it ‘Buy’ or ‘Strong Buy,’ with a consensus target of $483.83. The 24/7 Wall St. model projects $489.60 — a 16.8% upside — with a 90% confidence level and a bull case of $510.57 if AI server margins hold above 18% in H2.

What’s behind the insider selling — and does it matter?

Multiple insiders sold shares in early June — including Silver Lake entities ($371–$406 range), CFO Yvonne McGill’s predecessor David Kennedy, and COO Jeffrey Clarke — totaling over $1.2 billion in disclosed sales. However, officer Jane Tunnell gifted 519 shares on June 16, and Director Lynn Radakovich filed a Form 144 on June 22 to sell 12,022 shares — a routine liquidity event, not a signal of strategic concern. Gross margin compression (17.8% vs. 21.1% a year ago) reflects AI’s lower-margin, high-volume nature — but ISG operating margin actually expanded, validating Dell’s operational discipline. As Citigroup noted, ‘This isn’t margin erosion — it’s AI mix acceleration.’

What’s next for Dell’s AI infrastructure leadership?

This isn’t margin erosion — it’s AI mix acceleration.— Citigroup analyst

Dell Technologies Inc. has raised FY27 revenue guidance to $165–$169 billion, with AI server revenue now projected at $60 billion — up 144% year-over-year. The $1.44 billion U.S. Air Force contract announced June 15 confirms sovereign AI demand is accelerating. With the June 22 AI Factory launch, Dell is no longer just supplying servers — it’s delivering sovereign-ready AI infrastructure stacks. The company’s Texas domicile vote at its June 23 annual meeting could further streamline regulatory and tax positioning for federal AI contracts. As Jim Cramer observed, Dell now trades at just 23x FY27 EPS — far below the NASDAQ-100’s 32x — making it one of the most compelling AI infrastructure values on Wall Street.